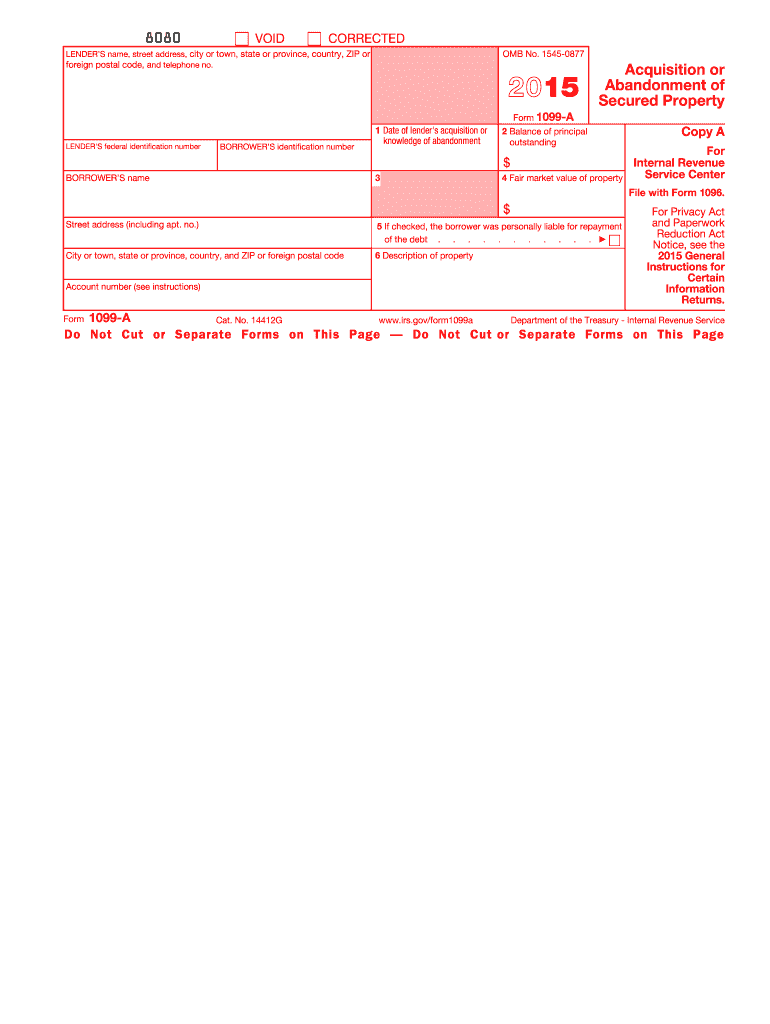

Definition and Purpose of the 1099-A 2015 Form

Form 1099-A, Acquisition or Abandonment of Secured Property, is employed by lenders to report the acquisition or abandonment of property that is secured for loans. It serves as part of the Internal Revenue Service's (IRS) information returns, contributing to the accurate reporting of asset transfers involving secured properties. This form provides details on the loan balance at the time of acquisition or abandonment, the fair market value of the property, and borrower information. It's essential for borrowers to receive this form to accurately report potential capital gains or losses on their tax returns.

How to Obtain the 1099-A 2015 Form

To access a Form 1099-A for 2015, individuals can explore multiple acquisition channels:

-

From Lenders: Lenders are responsible for issuing this form after acquiring or declaring a property abandoned. Borrowers should receive a copy from their lender, so verifying with them can be the first step.

-

IRS Resources: Individuals can request forms and instructions directly from the IRS by visiting their official website or ordering via phone.

-

Professional Assistance: Tax professionals and accounting services often have the necessary versions of tax forms that may not be as readily accessible elsewhere.

Steps to Complete the 1099-A 2015 Form

Accurate completion of Form 1099-A involves several specific stages:

-

Gather Information: Collect details concerning the property involved and the financial context, including debt balance and property fair market value.

-

Form Sections: Fill out the form by ensuring all required sections are completed:

- Lender’s details, including Federal Identification Number (TIN)

- Borrower's TIN and information

- Property description and status

-

Verification: Double-check values entered for accuracy, particularly focusing on debt balance and fair market value.

-

Submission: Distribute the filled form to the borrower and provide a copy to the IRS, adhering to the specific filing instructions outlined.

Who Typically Uses the 1099-A 2015 Form

This form is primarily utilized by financial institutions and borrowers who have been involved in an acquisition or abandonment of a secured property.

- Lenders: Including banks and mortgage holders, to comply with reporting regulations.

- Borrowers: Those experiencing foreclosure or conducting short sales to ensure accurate financial reporting and tax compliance.

Understanding this form’s purpose is critical to all parties involved in such transactions, assuring correct filing with the IRS.

Key Elements Found on the 1099-A 2015 Form

Central elements of the 1099-A form focus on the identification and financial specifics related to the property and involved parties:

- Date: Reflects when the lender acquired the property or when it was abandoned.

- Fair Market Value: A necessary figure, as determined at the time of acquisition or abandonment.

- Outstanding Debt: The balance of the principal outstanding at the time the form is issued.

- Property Description: A clear depiction of the property, ensuring proper identification.

IRS Guidelines for the 1099-A 2015 Form

Compliance with IRS guidelines is crucial to prevent potential penalties:

- Filing Procedures: Offers instructions on form submission, either electronically or via paper filing, to ensure timely and correct delivery.

- Use For Tax Reporting: The borrower uses the details on the 1099-A to report gains or losses upon the sale or acquisition of property on their tax return.

Filing Deadlines and Important Dates

Timeliness is critical when dealing with the 1099-A form:

- Lender Submission: Issuers must file the form with the IRS no later than the end of February if filing on paper or the end of March if filing electronically.

- Borrower Receipt: Should be delivered to borrowers by January 31st following the tax year in question to ensure adequate time for personal tax preparation.

Penalties for Non-Compliance Related to the 1099-A 2015 Form

Failure to adhere to compliance requirements can lead to significant repercussions:

- Monetary Penalties: Lenders may face fines for failing to file timely or correct information with the IRS.

- Tax Implications for Borrowers: Inaccurate reporting due to the absence of a 1099-A can result in additional taxable capital gains, penalties, or interest charges.

Understanding and addressing the procedures associated with the Form 1099-A, including obtaining, completing, and submitting it timely, ensures taxpayers remain in compliance with IRS regulations, minimizing risks associated with financial reporting errors.