Definition & Meaning

Form 1099-A, titled "Acquisition or Abandonment of Secured Property," is a tax document used primarily in the United States to report the acquisition or abandonment of properties that are secured. When a property is either foreclosed upon or its ownership changes under secured conditions, the 1099-A form serves to document these transactions for tax purposes. This form is vital for both the lender and the borrower as it records important details such as the date of the transaction, the fair market value of the property, and any outstanding debt.

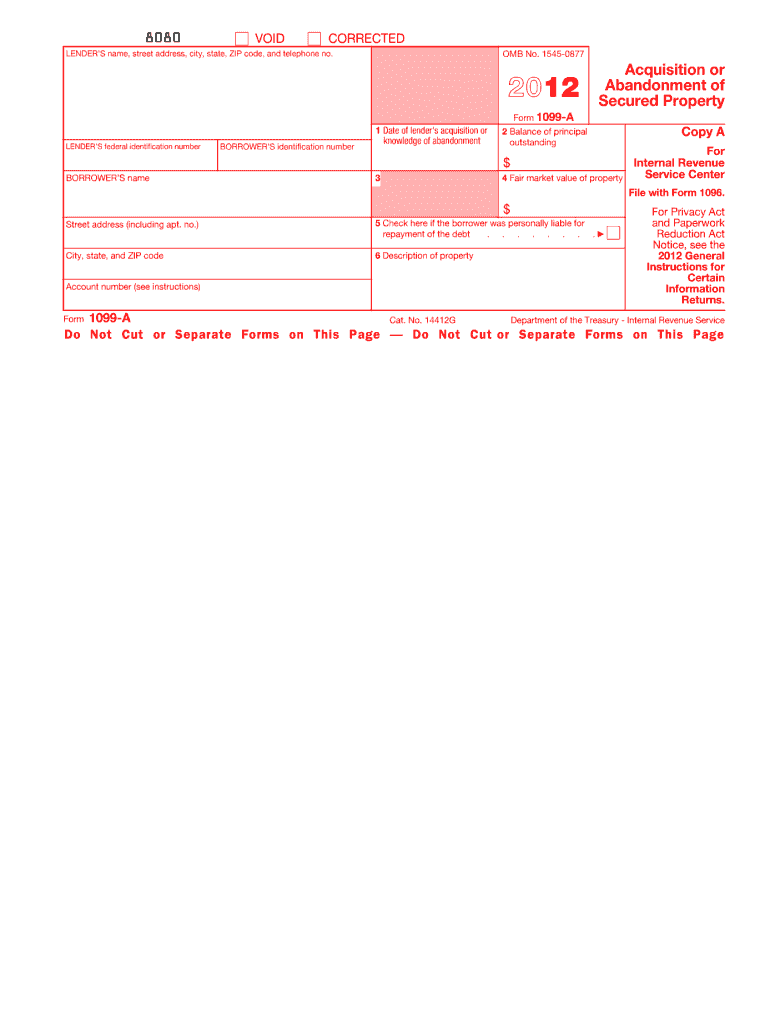

Key Elements of Form 1099-A

Understanding Form 1099-A requires familiarity with its key components, including:

- Date of acquisition or abandonment: Indicates when the transaction took place.

- Borrower’s identification: Includes the borrower’s name and Taxpayer Identification Number (TIN).

- Fair market value (FMV): Reflects the property's value at the time of acquisition or abandonment.

- Balance of principal outstanding: This shows the amount still owed on the property.

How to Obtain the 1099-A 2012 Form

Obtaining the 1099-A form is usually straightforward, as it is provided by the lender. Lenders must issue this form to borrowers involved in property-related transactions that fall under this category. Borrowers or lenders can also access official forms by visiting the IRS website, where they can download and print the necessary documents. It is important to note that the online version of the form should not be filed as it is not scannable, emphasizing the necessity of using the official form for mailing purposes.

Steps to Complete the 1099-A 2012 Form

Completing the 1099-A form accurately involves several steps to ensure all parties fulfill their reporting obligations:

- Gather relevant documents: Obtain details about the property, transaction date, fair market value, and outstanding debt.

- Fill in borrower and lender information: Include both entities’ names and tax identification numbers.

- Enter transaction specifics: Record the date of acquisition or abandonment alongside the property’s fair market value.

- Submit the form: Send the completed form to the appropriate IRS office, and provide copies to involved parties.

Practical Examples

- Foreclosure: In cases of foreclosure, lenders use Form 1099-A to report the transaction, detailing information such as the outstanding debt and the property’s fair market value at the time of transfer.

- Abandonment: Situations where the borrower abandons property also require the form to capture the same critical data.

Why Should You File a 1099-A 2012 Form?

Filing Form 1099-A holds significance for compliance with federal tax laws and fulfilling reporting obligations. It serves as a formal record for the IRS to track changes in ownership for secured properties, facilitating accurate taxation and prevention of fraud or errors in property handling. Lenders need these forms for internal record-keeping and ensuring borrower transparency.

Implications for Borrowers

Filing Form 1099-A provides borrowers relief by formalizing the foreclosure process, establishing clear documentation for their tax records, and potentially influencing their credit standing depending on how the transaction is recorded and settled.

Who Typically Uses the 1099-A 2012 Form?

Form 1099-A is primarily used by financial institutions, lenders, or banks that foreclose on properties that were secured under a loan agreement. It is also used by individuals who elect to abandon properties under financial constraints. The IRS requires this form from any situation where the ownership or secured status of a property changes under lending agreements.

Legal Use of the 1099-A 2012 Form

This form must comply with IRS regulations outlined under foreclosure or secured property abandonment events. The ESIGN Act ensures the legality of electronically maintained forms, while the IRS provides guidelines to avoid legal pitfalls associated with improperly filed documents. Inaccurate or non-compliance may result in substantial penalties.

IRS Guidelines

The IRS guidelines for Form 1099-A require exact adherence to specific protocols. Incomplete or incorrect filings can cause discrepancies in tax reporting, leading to audits or fines. Lenders need to follow precise timing rules regarding when to send this form, typically before the end-of-year reporting deadlines. Comprehensive instruction guides are available from the IRS to assist with any ambiguities during preparation.

Penalties for Non-Compliance

Failing to file a 1099-A form or doing so inaccurately can result in penalties imposed by the IRS. Such penalties may include monetary fines that increase with the duration of non-compliance, depending on the negligence's seriousness and duration. Timely and accurate filings, therefore, protect both lenders and borrowers from legal and financial repercussions.