Understanding Form 1099-A

Form 1099-A is used for reporting the acquisition or abandonment of secured property in the United States. It is primarily utilized by lenders to inform the IRS when they repossess or cancel the debt of a property. This form is essential for tracking financial gains or losses related to secured properties, which can have significant tax implications for both lenders and borrowers.

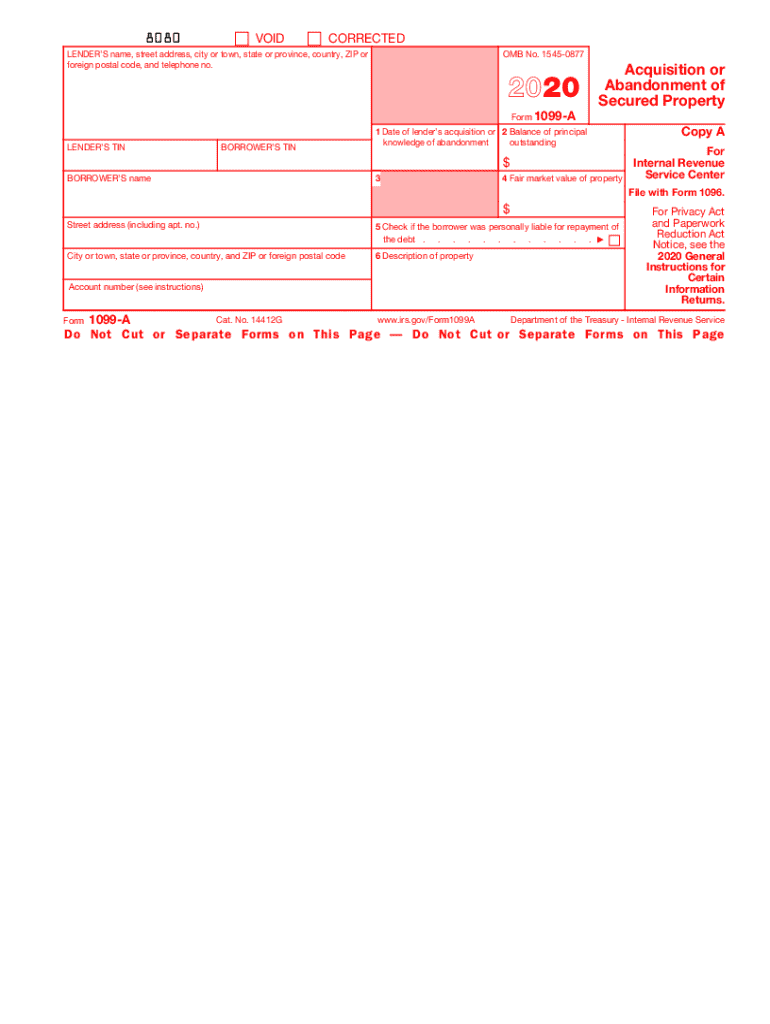

Key Elements of Form 1099-A

Form 1099-A contains several crucial details:

- Lender’s details: Name, address, and TIN (Tax Identification Number).

- Borrower’s information: Name, address, and TIN.

- Description of the property: A clear identification of the property involved.

- Date of acquisition or abandonment: The key date when the lender acquired the property or it was abandoned.

- Balance of principal outstanding: The amount the borrower still owes on the mortgage.

- Fair market value of the property: The property's value at the time of acquisition or abandonment.

Steps to Complete Form 1099-A

- Gather Information: Collect details about the borrower, lender, and relevant financial data.

- Complete Borrower and Lender Details: Enter the name, address, and tax identification numbers.

- Describe the Property: Provide a detailed description.

- Enter the Date: Specify when the property was acquired or abandoned.

- Calculate the Outstanding Debt: Fill in the principal balance still owed.

- Assess Fair Market Value: Provide the property’s fair market value at the time of the transaction.

- Review and Submit: Double-check information for accuracy before submission to the IRS.

How to Obtain Form 1099-A

Form 1099-A can be obtained directly from the IRS website. Financial institutions or lenders typically issue it when reporting to the IRS. It’s essential to ensure that the copy intended for submission to the IRS (Copy A) is correctly formatted and not printed from unofficial sources to avoid scanning issues.

Filing Deadlines and Important Dates

Lenders must adhere to strict deadlines when filing Form 1099-A:

- January 31: Deadline to furnish the borrower with their copy.

- February 28: If filing by paper, this is the deadline for submission to the IRS.

- March 31: For electronic filings, the due date is the end of March.

Legal Use and Compliance

It is crucial that Form 1099-A is used in accordance with IRS guidelines. The form is legally binding, and both lenders and borrowers must ensure accuracy to avoid tax complications. Lenders are responsible for issuing the form accurately and timely, while borrowers must report it to the IRS as part of their tax returns if required.

Penalties for Non-Compliance

Failure to file Form 1099-A appropriately can result in penalties for lenders. These penalties are usually monetary and can increase if the non-compliance is judged to be intentional. The amount of the penalties varies, depending on the extent and nature of the error.

Taxpayer Scenarios Involving Form 1099-A

Form 1099-A is particularly relevant in scenarios where a property owner defaults on a secured debt, like a mortgage, and the lender repossesses the property. Possible scenarios include:

- Foreclosure: The lender takes possession of a property due to the borrower's failure to meet repayment terms.

- Voluntary repossession: The borrower hands the property back to the lender to cancel the outstanding mortgage.

Software Compatibility

Many tax software solutions, such as TurboTax and QuickBooks, streamline the process of dealing with Form 1099-A. These software options often include step-by-step guidance to ensure compliance and accurate reporting. They can import data directly from financial records, which minimizes errors and saves time compared to manual entry.

IRS Guidelines on Form 1099-A

The IRS provides comprehensive guidelines on when and how to use Form 1099-A. It defines the roles and responsibilities of both the lender and the borrower in reporting these transactions. Understanding and following these guidelines help avoid complications with annual tax returns and ensures both parties comply with federal requirements.