Definition & Meaning

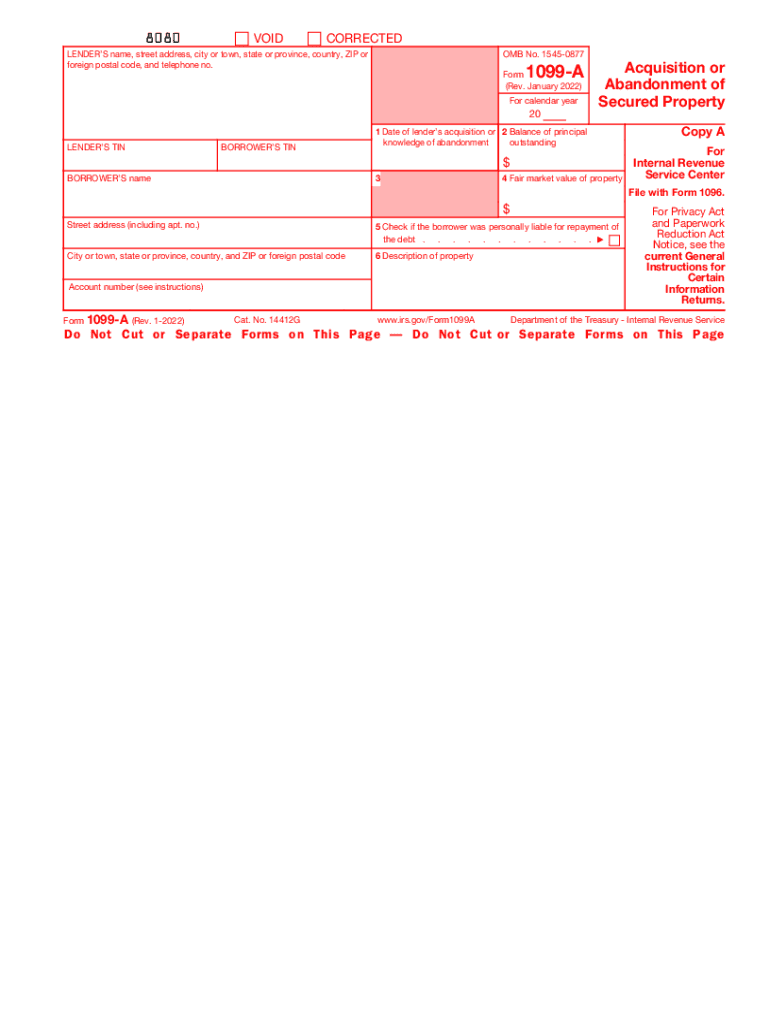

Form 1099-A, known officially as "Form 1099-A (Rev. January 2022). Acquisition or Abandonment of Secured Property," is a document used by lenders to report the acquisition or abandonment of secured property. This form plays a crucial role when borrowers fail to meet their debt obligations, resulting in lenders acquiring the property or the borrower abandoning it. The information on Form 1099-A aids in declaring potential taxable events related to the discontinued use or foreclosure of property, which might lead to cancellation of debt income for the borrower.

Key Elements of the Form 1099-A

- Description of Property: Details about the property secured for the debt, such as real estate or personal property.

- Balance of Principal Outstanding: The remaining debt amount the borrower owes when the property is acquired or abandoned.

- Fair Market Value of Property: The estimated market value of the property at the time of acquisition or abandonment.

- Date of Acquisition or Abandonment: Specific date when the lender took back the property or it was abandoned by the borrower.

- Parties Involved: Information about both the borrower and lender, including names, addresses, and taxpayer identification numbers.

How to Use the Form 1099-A

Lenders must fill out and issue Form 1099-A to both the IRS and the borrower when a property is either acquired or abandoned. The borrower uses this form to evaluate potential tax implications, as the transaction might lead to a recognition of income or loss. For instance, if the property's market value exceeds the outstanding debt, the borrower could face income as a result of the debt cancellation. Conversely, if the outstanding balance surpasses the property's value at abandonment, a loss might be recognized.

Steps to Complete the Form 1099-A

- Identify Property and Borrower: Collect accurate information on the property and the borrower involved.

- Enter Financial Details: Include the principal balance owed and the fair market value of the property.

- Record Date: Clearly list the date of acquisition or abandonment.

- Submit to IRS and Borrower: Send the completed form both to the IRS and provide a copy to the borrower.

Important Terms Related to Form 1099-A

- Secured Property: Assets used as collateral for a loan.

- Acquisition: Process where the lender takes possession of the secured property.

- Abandonment: Borrower's voluntary relinquishment of the property secured to the lender.

- Fair Market Value: An estimate of the price a property would fetch in the open market.

Legal Use of the Form 1099-A

The form ensures compliance with tax laws by documenting transactions involving secured properties' acquisition or abandonment. Its legal significance lies in the fact that it helps the IRS monitor potential taxable events due to property foreclosures or abandonments, aligning with federal laws governing the taxation of canceled debts.

IRS Guidelines

The IRS mandates that Form 1099-A must be submitted by the lender when a secured property is acquired or abandoned. The guidelines underscore the necessity for providing accurate and timely information to prevent legal discrepancies and ensure compliance with tax obligations. Lenders must adhere to deadlines and maintain consistency in reporting the transaction details.

Filing Deadlines / Important Dates

Form 1099-A has specific submission deadlines. Lenders are generally required to furnish the form to the borrower and the IRS by January 31st of the year following the calendar year in which the property was acquired or abandoned. Adhering to these deadlines is vital, as late submissions can lead to penalties or interest charges.

Penalties for Non-Compliance

Failing to issue or file Form 1099-A can result in penalties. Lenders who neglect to file the form on time with the IRS or provide it to the borrower might incur fines that escalate based on the duration of the delay and the incompleteness of the submission. Understanding and avoiding these penalties is crucial for maintaining regulatory compliance.

Examples of Using the Form 1099-A

- Foreclosure Scenario: A borrower defaults on a mortgage, and the lender forecloses the property. The lender issues Form 1099-A detailing the transaction to the borrower and the IRS.

- Voluntary Abandonment: A borrower willingly leaves a property after ceasing loan payments. The lender reports this abandonment through Form 1099-A.

Who Typically Uses the Form 1099-A

Form 1099-A is typically used by lending institutions such as banks, credit unions, government agencies, and real estate lenders when they repossess or when there is abandonment of secured property. Borrowers, on the other hand, use this form to understand potential tax impacts and report the information correctly on their tax returns.