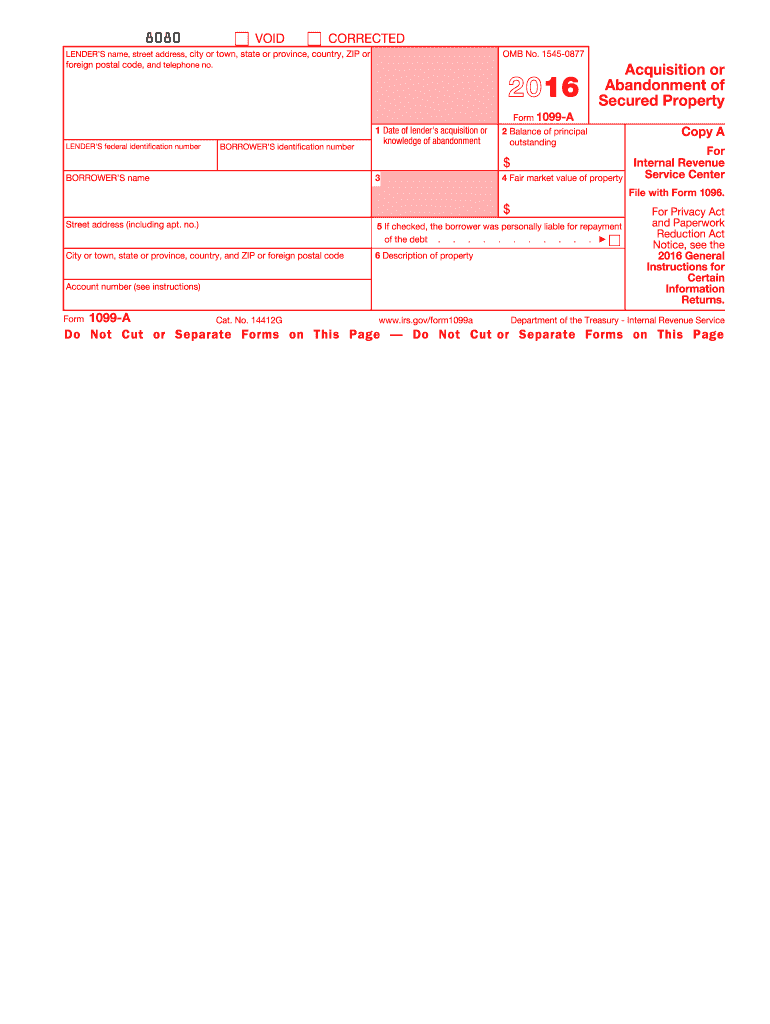

Definition and Purpose of Form 1099-A

Form 1099-A, titled "Acquisition or Abandonment of Secured Property," is used by lenders to report borrowers who have had their property acquired by the lender or have abandoned the property securing a loan. This form is crucial in detailing the transaction details related to the foreclosure or abandonment of property. It helps both lenders and borrowers understand the tax implications resulting from these events. The form is a necessity in cases where a loan is secured by property that the borrower no longer possesses.

How to Use the 1099-A Form

Filling out a 1099-A form involves entering specific information about the lender, borrower, and the property in question. Lenders must complete the form when acquiring property through foreclosure or when a borrower abandons secured property. In Box 1, lenders provide the date of the acquisition or the date the borrower abandoned the property. Box 2 requires the balance of the principal outstanding. Box 3 specifies the property's fair market value on the acquisition date or upon abandonment. Box 5 establishes whether the borrower was personally liable for repaying the debt. This information is essential for borrower records and IRS filings.

Steps to Complete the 1099-A Form

- Gather information about the borrower, including name and taxpayer identification number.

- Obtain the necessary details of the secured property, such as its description and location.

- Record the balance of the principal outstanding in Box 2.

- Determine the fair market value of the property as of the acquisition or abandonment date and enter it in Box 4.

- Indicate whether the borrower was personally liable for the debt in Box 5.

- Ensure the form is accurate and complete. Any inaccuracies can result in legal issues or incorrect tax filings.

Who Uses the 1099-A Form

Both lenders and borrowers have interests in the 1099-A form. Lenders use it to report the foreclosure or abandonment of property. Borrowers refer to this form to determine their financial responsibilities and tax obligations following the loss of property. Real estate professionals and financial advisors might also involve themselves in the process to assist clients with tax planning and compliance tied to these events. Additionally, the IRS utilizes this data to monitor the transactions and verify tax liabilities.

Important Terms Related to Form 1099-A

- Foreclosure: The legal process by which a lender takes control of a property used to secure a loan when the borrower fails to make required loan payments.

- Abandonment: When a borrower voluntarily leaves a property without the intention of returning or reclaiming it.

- Fair Market Value (FMV): An estimate of the property's market value, representing what a willing buyer would pay a willing seller.

- Principal Outstanding: The remaining balance on a loan, excluding any unpaid interest or future obligations.

Legal Use of the 1099-A Form

The use of Form 1099-A is defined by IRS regulations. Lenders are legally required to use it to report property acquisitions or abandonments to both the borrower and the IRS. For borrowers, understanding this form is essential to accurately report income and any potential capital gains resulting from a foreclosure or an abandoned property. Legal compliance ensures transparency and accountability in financial transactions involving secured properties.

Key Elements of the 1099-A Form

The form consists of several key elements necessary for compliance:

- Borrower’s Tax Identification Number (TIN): Essential for associating the transaction with the correct taxpayer.

- Lender’s Information: Includes the lender’s name, address, and TIN.

- Description of Property: Details of the foreclosed or abandoned property to clearly identify the assets involved.

These elements are crucial in ensuring all parties have the necessary information to fulfill their tax obligations and document the transaction appropriately.

IRS Guidelines and Compliance

The IRS provides comprehensive guidelines to ensure that Form 1099-A is used appropriately. The form must be filed by lenders by February 28 if submitted by mail, or March 31 if filed electronically following the tax year in which the property was acquired or abandoned. Failure to comply with these deadlines or submit accurate information can result in penalties. Lenders must issue this form to borrowers by January 31. This ensures borrowers have vital information in time for tax planning and filings.