Definition and Meaning of 1099-A 2014 Form

Form 1099-A, Acquisition or Abandonment of Secured Property, is primarily used by lenders to report the acquisition or abandonment of secured property to the Internal Revenue Service (IRS). This form is applicable when property has been either foreclosed upon or repossessed. The 2014 version of the form captures lender details, the fair market value of the property, and the outstanding mortgage balance at the time of acquisition or abandonment. As the information contained within is crucial for the borrower's tax records, understanding this form's specifics is essential for both parties involved.

How to Use the 1099-A 2014 Form

Form 1099-A is utilized primarily by lenders who have acquired or foreclosed on a secured property. The borrower should incorporate this information when calculating their tax obligations, particularly relating to any gain or loss as a result of debt cancellation associated with the property. For example, if the fair market value of the property is less than the owed balance, the difference may constitute taxable income. It's critical to integrate the figures from 1099-A into the taxpayer's Schedule D or Form 982, whichever is applicable.

Steps to Complete the 1099-A 2014 Form

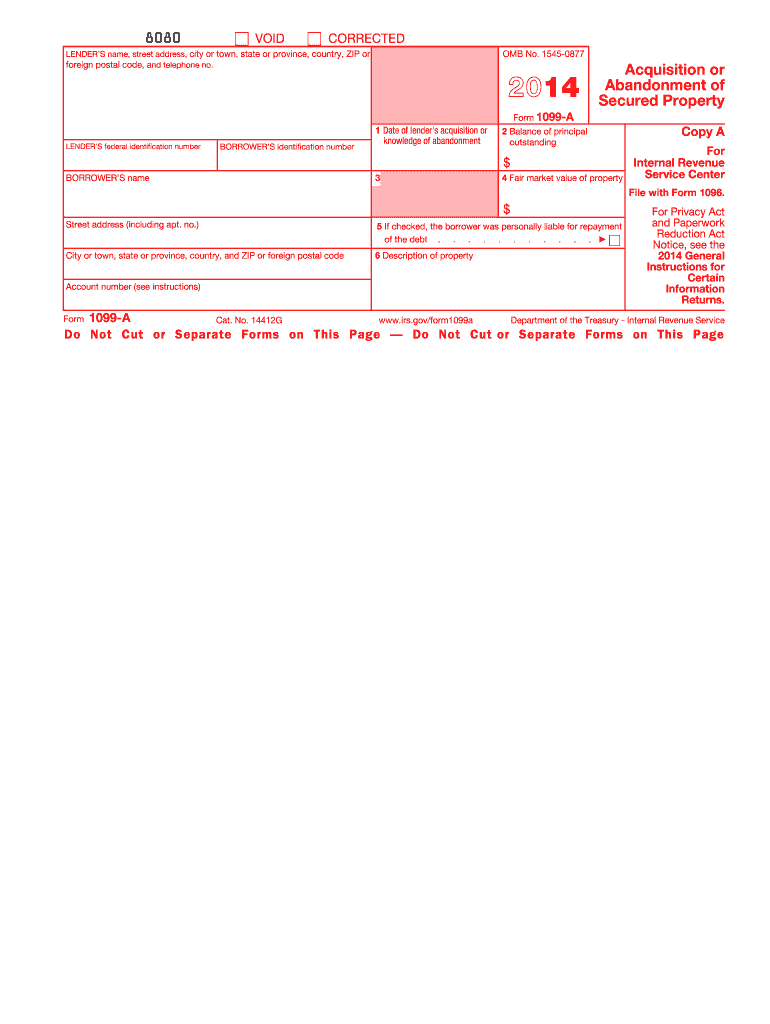

- Lender Identification: Fill out the lender's information accurately, including their name, address, and taxpayer identification number.

- Borrower Information: Ensure the borrower’s correct name, address, and taxpayer identification number are entered.

- Property Details: Include details of the property acquired or abandoned, such as the address or an adequate description.

- Outstanding Balance: Note the outstanding principal balance of the loan at the time of acquisition or foreclosure.

- Fair Market Value: Enter the fair market value (FMV) of the property on the date of acquisition or abandonment.

- Personal Liability: Indicate whether the borrower was personally liable for the debt, which impacts tax treatment.

These steps ensure comprehensive and accurate completion of the form, satisfying IRS requirements.

Key Elements of the 1099-A 2014 Form

The 1099-A form consists of several key components that require precise information:

- Box 1: Date of lender acquisition or property abandonment.

- Box 2: Balance of principal outstanding.

- Box 3: Reserved for future use and typically left blank.

- Box 4: Note if the borrower is responsible for repaying the full loan.

- Box 5: Fair market value of the property.

- Box 6: Indicates whether the borrower was personally liable for the debt.

Understanding each box's requirements ensures correct data submission.

Who Typically Uses the 1099-A 2014 Form

Primarily, lenders and mortgage holders use Form 1099-A upon repossession or abandonment of secured property. Borrowers, on the other hand, need to review the information reported to understand potential tax implications. The form is instrumental for borrowers when addressing potential income from the difference between the fair market value of the property and the outstanding mortgage balance. Accountants and tax professionals also frequently utilize this information when preparing clients' tax returns to ensure IRS compliance.

Penalties for Non-Compliance with 1099-A Form Requirements

Lenders failing to correctly file and distribute Form 1099-A could face significant penalties from the IRS. Non-compliance includes not providing the form by the required deadlines or submitting inaccurate information. Borrowers should also ensure they report the details from Form 1099-A accurately on their tax returns to avoid potential fines and penalties due to underreported income. Keeping meticulous records and timely compliance is crucial to avert any complications.

IRS Guidelines for the 1099-A 2014 Form

The IRS requires that lenders document and file Form 1099-A when a property has been foreclosed, repossessed, or otherwise abandoned. This submission must occur both to the IRS and be provided to the borrower typically by January 31st of the following year. The information on this form plays a critical role in determining any potential gain or loss incurred by the borrower, affecting their annual tax filing. Adhering to these guidelines ensures smooth processing and minimizes the risk of audit or penalties.

Required Documents for Completing the 1099-A 2014 Form

To complete Form 1099-A, lenders and taxpayers should have:

- Loan Documentation: Details of the original loan, including the terms and conditions.

- Property Valuation: An appraisal or official valuation of the property's fair market value at the relevant date.

- Foreclosure Records: If applicable, documentation of the foreclosure process.

- Contact Information: Current details for both the borrower and lender.

Having these documents readily available aids in the accurate completion and submission of Form 1099-A.

Examples of Using the 1099-A 2014 Form

Consider a borrower who defaults on a mortgage, and the lender forecloses on the home. The lender uses Form 1099-A to report the acquisition to the IRS. If the outstanding loan balance was $200,000 and the fair market value of the property at foreclosure was $180,000, then the borrower might have $20,000 in taxable income, representing the debt canceled. Understanding such examples can help clarify tax obligations and subsequent filings related to real estate transactions and debt discharge.

Legal Use of the 1099-A 2014 Form

For both lenders and borrowers, Form 1099-A serves critical legal and tax functions. Correctly filling out and filing this form ensures adherence to IRS rules and assists in appropriate tax reporting for transactions involving abandoned or repossessed properties. Given the potential complexity of these situations, lenders should seek legal advice if there are questions regarding compliance or specific borrower filings. This ensures protection from legal disputes while aligning with regulatory standards.

Form Submission Methods: Online, Mail, or In-Person

Lenders must submit Form 1099-A to the IRS either electronically or by mail, depending on the number of forms prepared. Electronic filing is mandatory if filing 250 or more 1099 forms. Submissions cannot be made in-person at IRS offices. Borrowers receive paper copies as they require this data for their records and subsequent tax filings. The final forms must reach the borrowers by January 31st to streamline the tax preparation process.