Definition & Meaning

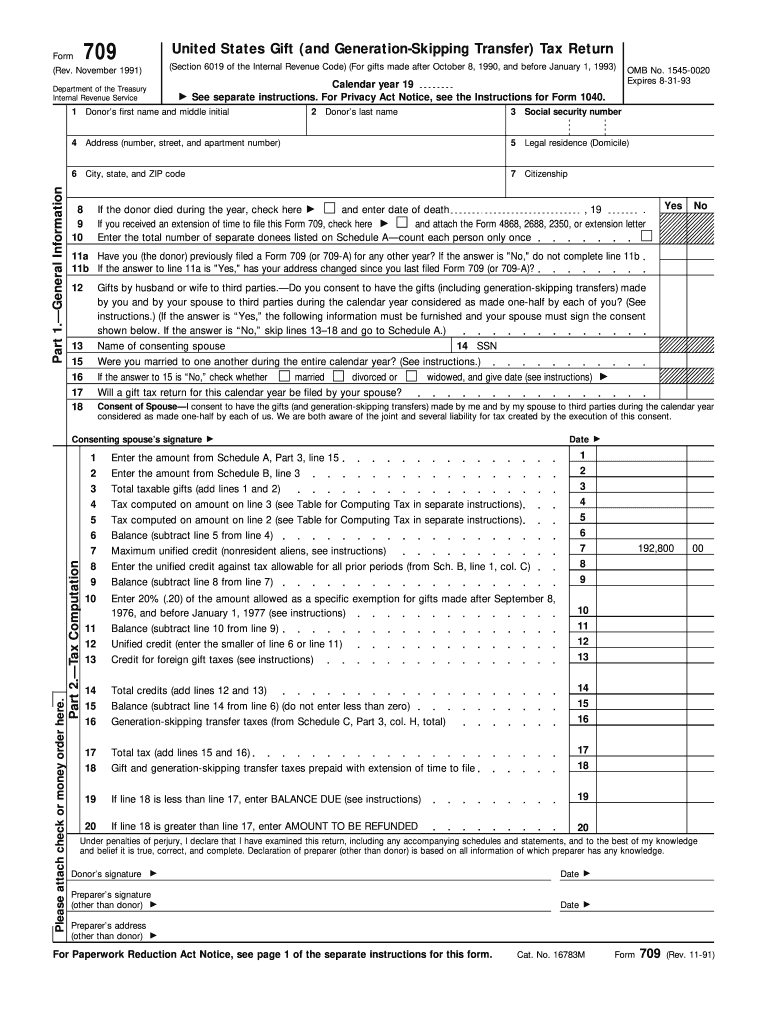

The Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is employed to report gifts exchanged between individuals and determine applicable gift taxes. It encompasses general information about the donor, specifics of gifts given, tax calculation, and reconciliation of generation-skipping transfer taxes. Importantly, the version referred to as "1991 Form" caters primarily to gifts made between October 8, 1990, and January 1, 1993.

Steps to Complete the 1991 Form

-

Provide Personal Information:

- Start by entering the donor’s personal details, including full name, address, and taxpayer identification number.

-

List of Gifts:

- Detail each gift, its fair market value, and the recipient’s details. This section requires precision to avoid misinterpretation.

-

Computing Gift Tax:

- Follow the instructions to calculate any due gift tax based on the cumulative value of the gifts listed.

-

Generation-Skipping Transfer Tax:

- If applicable, compute the tax specifically related to generation-skipping transfers, a critical component for reporting.

-

Signature and Date:

- Ensure the form is signed and dated, confirming the information's accuracy under penalty of perjury.

-

Attachments:

- Attach any necessary documentation supporting valuations or special circumstances that might affect the tax computation.

Why Use the 1991 Form

-

Regulatory Compliance:

- It ensures compliance with IRS regulations regarding gift and generation-skipping transfer taxes.

-

Accurate Tax Reporting:

- Filing this form helps accurately report gifts to prevent future tax liability discrepancies.

-

Avoid Penalties:

- Proper submission of this form helps avoid penalties associated with late or incorrect filing.

Who Typically Uses the 1991 Form

-

Individuals Making Significant Gifts:

- Typically, individuals who make substantial gifts that exceed the annual exclusion limit need to file this form.

-

Estate Planners:

- Those involved in estate planning often use this form to manage the tax implications of substantial bequests or transfers.

Required Documents

-

Appraisals:

- Documentation of fair market valuations, especially for non-cash gifts.

-

Identifying Information:

- Tax identification numbers for both the donor and recipients ensure accurate records.

-

Past Returns:

- Previous Form 709 submissions may be necessary to verify historical gift values and prior taxes paid.

Filing Deadlines / Important Dates

-

Annual Deadline:

- The form is generally due on April 15th of the year following the calendar year when the gifts were made.

-

Extensions:

- An extension for filing Form 709 can be obtained if needed, corresponding to the extension for filing an income tax return.

Legal Use of the 1991 Form

-

Record Keeping:

- Legally serves as documentation for both the IRS and personal records of significant financial gifts.

-

Tax Disputes:

- Provides a legal basis and documentation in case of disputes or audits regarding gift taxes.

Penalties for Non-Compliance

-

Late Filing Penalties:

- Failing to file by the deadline without an extension results in financial penalties and potential interest on the tax owed.

-

Accuracy-related Penalties:

- Incorrect reporting or underpayment of taxes due from inaccurate form completion could also incur additional charges.

Form Submission Methods (Online / Mail / In-Person)

-

Mail:

- Traditional mailing is common, with a physical copy sent to the specified IRS address.

-

Courier:

- For time-sensitive submissions, using a courier service ensures the IRS receives the form by the deadline.

This structure provides an organized and comprehensive overview of "1991 Form," ensuring clarity and comprehensive understanding for users engaging with the document.