Definition & Purpose of the 2002 IRS Form 1040

The 2002 IRS Form 1040 is a crucial document utilized by individuals in the United States to file their annual income tax returns. This form serves as a comprehensive tool for taxpayers to report their earnings, claim relevant deductions, and determine their tax responsibilities. It includes various sections designed to capture personal information, income details, and adjustments, ensuring accurate tax calculations.

For taxpayers, understanding the purpose of the Form 1040 is essential for fulfilling legal tax obligations. This form is essential in reflecting an individual's financial activities over the tax year, enabling both transparency and accuracy in tax reporting. Taxpayers utilize this form to achieve fair outcomes regarding their due taxes, liabilities, or potential refunds from the IRS.

Steps to Complete the 2002 IRS Form 1040

Completing the Form 1040 involves a systematic approach for accuracy. Here's a step-by-step guide:

-

Gather Required Documentation:

- Collect essential financial documents, including W-2s, 1099s, and records of other income sources.

- Ensure you have records of any deductible expenses, charitable contributions, and potential tax credits.

-

Fill Personal Information:

- Enter your name, Social Security Number (SSN), and address.

- Indicate your filing status, such as single, married filing jointly, or head of household.

-

Report Income:

- Add wages, salaries, and tips documented in W-2 forms.

- Include other income like dividends or self-employment earnings, ensuring alignment with corresponding 1099 forms.

-

Claim Deductions and Credits:

- Itemize deductions if applicable or claim the standard deduction.

- Eligible credits, such as the Earned Income Credit, should be claimed accurately.

-

Calculate Tax Liability:

- Determine your taxable income and refer to IRS tax tables to establish the correct amount of owed taxes.

- Subtract applicable credits to find the net tax liability or refund amount.

-

Review and Sign:

- Double-check all entries for accuracy.

- Sign and date the form before submission.

How to Obtain the 2002 IRS Form 1040

Accessing the 2002 IRS Form 1040 can be achieved through various methods:

-

IRS Website:

- Download a copy directly from the IRS archive section online.

-

Postal Request:

- Request a physical copy to be sent to your mailing address by contacting the IRS helpline.

-

Libraries and Post Offices:

- Obtain a copy from participating public libraries or post offices that stock backdated IRS forms.

Ensuring you have the correct version is vital for historical tax filing or amendment purposes.

IRS Guidelines on Using the Form

The IRS provides specific guidance for the correct use of the Form 1040:

-

Accurate Reporting:

- Ensure all income and deductions are reported accurately to avoid discrepancies with IRS records.

-

Filing Status Selection:

- The chosen filing status must reflect the taxpayer's situation as of December 31, 2002.

-

Deadline Adherence:

- Meet the filing deadline, typically April 15th, to avoid penalties unless an extension is granted.

Failing to adhere to these guidelines can result in penalties and interest on unpaid taxes.

Key Elements of the 2002 IRS Form 1040

The Form 1040 comprises several critical sections each serving a unique function:

-

Personal Information:

- Captures taxpayer identification details needed for account verification.

-

Filing Status:

- Determines tax brackets and eligibility for specific credits.

-

Income and Adjustments:

- Encompasses all sources of income, reflecting total earnings subjected to taxation.

-

Tax Computation:

- This section uses income data to establish tax responsibilities after deductions and credits.

Each element contributes to the overall tax calculation, ensuring clarity and precision in tax reporting.

Penalties for Non-Compliance

Non-compliance with IRS requirements can result in significant penalties:

-

Failure-to-File Penalty:

- Applies if the form isn't submitted by the deadline, accumulating at a rate of 5% per month up to 25%.

-

Late Payment Penalty:

- Imposed if taxes are unpaid by the deadline, accruing monthly until settled.

-

Accuracy-Related Penalties:

- These apply where understated taxes due to negligence or substantial inaccuracies are present.

Understanding these penalties emphasizes the importance of timely and accurate filing.

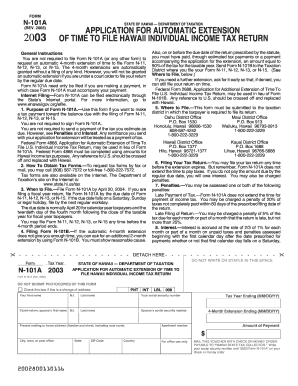

Filing Deadlines and Important Dates

For the 2002 tax year, specific deadlines are critical:

-

Regular Filing Deadline:

- April 15, 2003, is the standard deadline for submission.

-

Extended Deadline:

- October 15, 2003, provides additional time for those granted an extension.

Meeting these deadlines ensures compliance and avoids unnecessary penalties.

Digital vs. Paper Version of the Form

Taxpayers have the option to file using either digital or paper formats:

-

Digital Filing:

- Offers ease of submission through e-filing services, reducing error rates and processing times.

-

Paper Filing:

- Traditional method, requiring manual completion and postal submission.

Both methods are valid, but electronic filing is preferred for its efficiency and convenience.