Definition and Purpose of the 2004 W-2 Form

The 2004 W-2 Form, officially known as the Wage and Tax Statement, is a document used by employers in the United States to report wages paid to employees and taxes withheld during the year 2004. The form is integral to the tax filing process in the U.S., serving as a record for the Internal Revenue Service (IRS) and employees alike. It discloses details about the employee’s earnings, Social Security contributions, and income tax withholdings, enabling individuals to accurately file their federal and state tax returns. The W-2 not only assists in informing the IRS of earnings but also plays a crucial role in determining taxpayers' eligibility for tax refunds.

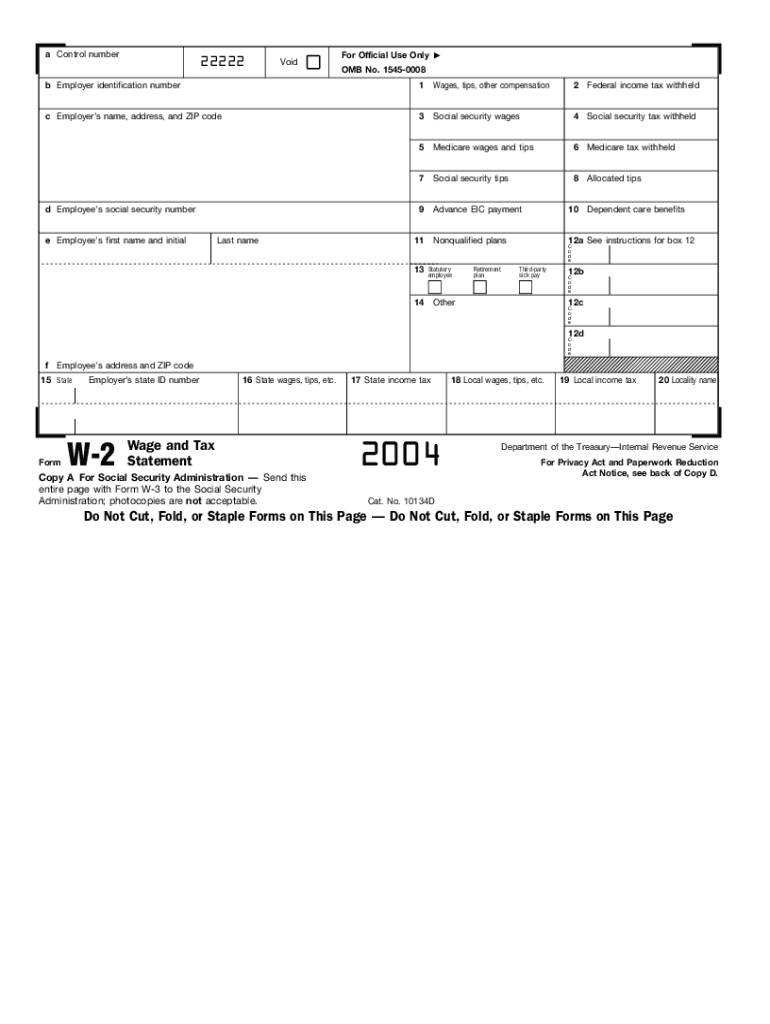

Key Components of the 2004 W-2 Form

The 2004 W-2 Form includes several sections that collect detailed information necessary for tax reporting.

- Employee Information: Contains personal details such as the employee’s name, address, and Social Security number.

- Employer Details: Lists the employer’s identification number, name, and address.

- Wages and Tax Withheld: Displays total wages, Social Security wages, Medicare wages, and federal and state tax withholdings.

- Other Compensations: Covers additional compensations like tips, bonuses, or certain fringe benefits.

- State and Local Details: If applicable, reports state income tax, wages, and state identification number.

Steps to Complete the 2004 W-2 Form

Completing the 2004 W-2 Form involves several steps to ensure accuracy and compliance.

- Gather Employer and Employee Information: Collect all necessary personal and employer identifiers.

- Accurate Calculation of Earnings: Ensure that full wages, including overtime and bonuses, are tallied.

- Withholding Reporting: Accurately calculate and report federal, state, and local taxes withheld.

- Filling Out and Distribution: Ensure all boxes are filled with the correct info. Distribute copies to employees and file with the IRS.

Who Typically Uses the 2004 W-2 Form

The W-2 Form is primarily used by employees and employers. Employers in any industry must complete this form for employees earning a salary or hourly wage during the year. Employees then use the form to file their personal tax returns. In addition to regular employees, this form is essential for anyone who has had income taxes withheld from wages, including part-time and seasonal workers.

Legal Use and Importance of the 2004 W-2 Form

The legal use of the 2004 W-2 Form is mandated by the IRS to ensure transparency in income reporting. Employers are legally required to furnish this form to their employees by the end of January following the tax year, ensuring that employees have the necessary documentation to file their taxes by the mid-April deadline.

Failure to provide or correctly file the W-2 can lead to penalties, underscoring the importance of accuracy in reporting all relevant wage and tax information.

How to Obtain the 2004 W-2 Form

Employees typically receive their W-2 Form from their employer. If misplaced, employees can request a duplicate from their company’s payroll or human resources department. For additional records, one can also request copies from the IRS, noting that processing may take some time.

Employers can acquire W-2 forms via the Social Security Administration's Business Services Online portal or by using payroll software that supports W-2 form generation.

IRS Guidelines and Compliance

Adherence to IRS guidelines is crucial for the successful and compliant submission of the 2004 W-2 Form. Critical components include:

- Deadline for Issuance: Employers must furnish W-2s to employees by January 31.

- E-File Requirement: Employers who file 250 or more W-2 forms must file electronically.

- Accuracy: Double-check data for accuracy to avoid discrepancies that might lead to IRS audits or penalties.

Common Errors and Penalties for Non-Compliance

- Errors: Common mistakes include incorrect Social Security numbers, misreported wages, or inaccurate tax withholdings.

- Penalties: Failing to file correct W-2s on time can result in penalties ranging from $50 to $530 per form, depending on the delay length and correction circumstances.

Understanding and adhering to these procedures ensures compliance with federal tax requirements, reducing the risk of audits or penalties for both employers and employees.