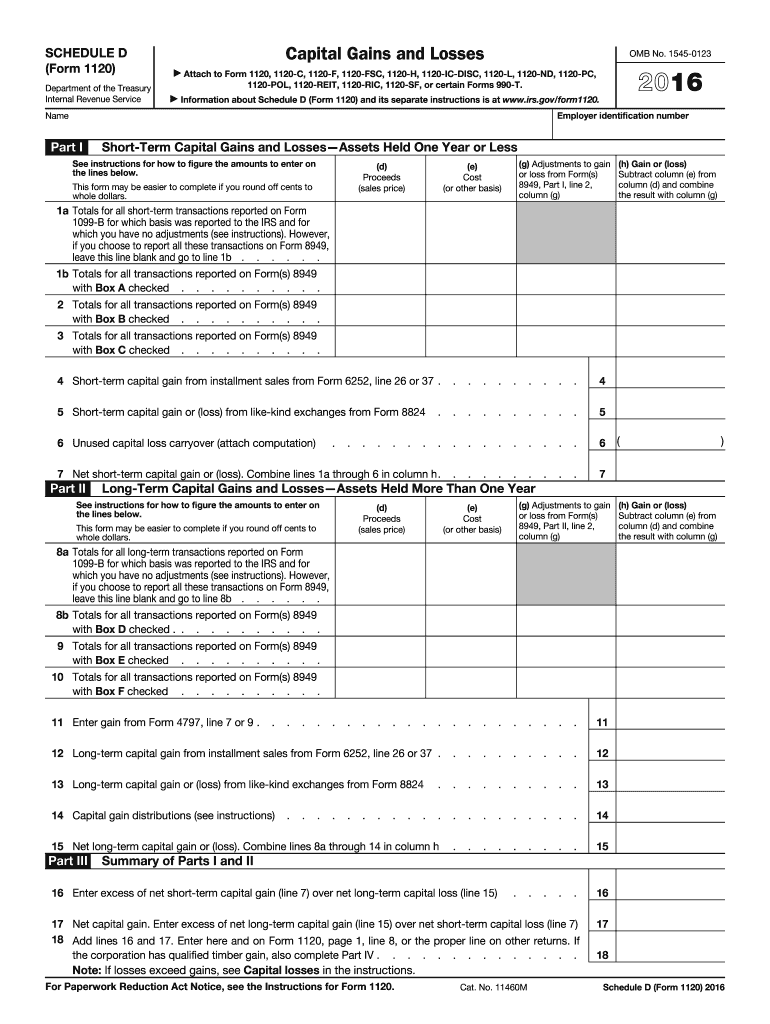

Definition and Purpose of Schedule D (Form 1120)

Schedule D (Form 1120) is primarily a tax form used by corporations to report their capital gains and losses from asset transactions. This form is critical for detailing both short-term and long-term capital transactions, ensuring corporations accurately declare gains or losses. The document aids in calculating the capital gain amount, which becomes a part of the taxable income for corporate tax filing.

Key Components

- Short-term capital gains and losses: Transactions involving assets held for one year or less.

- Long-term capital gains and losses: Deals with assets held for more than one year.

- Installment sales: Consideration of specific provisions for sales with payments distributed over multiple years.

- Like-kind exchanges: Reporting of exchanges where one asset is exchanged directly for another.

How to Use DocHub for the Form

DocHub offers immense utility for handling your 1120 Schedule D (Form 1120) for 2016. The platform's suite of tools enhances the ease of editing, signing, and sharing your form. By importing your form into DocHub, you can:

- Edit directly: Add necessary details, highlight critical information, or annotate sections for clarity.

- Sign electronically: Use legally binding digital signatures, simplifying the approval process.

- Collaborate and review: Set permissions for sharing with accountants or corporate partners.

Step-by-Step Process

- Upload the form: Import the Schedule D (Form 1120) from your device or linked cloud storage.

- Edit the form: Use the text and annotation tools to fill out the necessary sections accurately.

- Sign the form: Add electronic signatures where required.

- Share and export: Distribute completed forms securely via email or save them back to cloud storage like Google Drive.

Steps to Complete Schedule D (Form 1120)

Completing Schedule D accurately involves several key steps that ensure all necessary information is reported accurately.

Step-by-Step Instructions

- Gather Financial Data: Obtain all relevant financial records related to asset sales, including purchase and sale dates, cost basis, and sale price.

- Determine Holding Period: Establish if each transaction falls under short-term (assets held for a year or less) or long-term (assets held for more than a year).

- Calculate Gains or Losses: Subtract the cost basis from the sale price for each transaction to determine gain or loss.

- Complete Form Sections:

- List all transactions with required details.

- Calculate total gains and losses, categorizing them as short-term or long-term.

- Submit the Finalized Form: Attach Schedule D to the relevant corporate tax return when filing.

Required Documents for Filing

To efficiently complete the 1120 Schedule D for 2016, you need the following documents:

- Transaction records: Details of all asset sales, including purchase and sale documentation.

- Financial Statements: Adjusted income statements and balance sheets for accurate reporting.

- Previous Year’s Returns: Reference for historical gain or loss reporting and consistency.

Filing Deadlines and Important Dates

Deadlines are crucial for compliance when filing Schedule D (Form 1120). Corporations typically must adhere to the following schedules:

- Corporate income tax return deadline: Due by the 15th day of the 4th month after the corporation’s fiscal year ends. For calendar year filers, this is usually April 15.

- Extensions: Corporations may apply for a six-month extension, moving the deadline to October 15 for calendar year taxpayers.

IRS Guidelines for Schedule D

The IRS provides particular guidelines for completing Schedule D:

- Accurate Reporting: All capital asset sales or exchanges must be reported truthfully.

- Specific Instructions for Installment Sales and Timber Gain: Follow detailed IRS rules for scenarios like installment sales or qualified timber gains.

- Timely Filing: Strict adherence to filing deadlines and details to avoid potential penalties.

Penalties for Non-Compliance

Failure to adhere to the regulations involving 1120 Schedule D can result in penalties. Corporations face:

- Late filing penalties: Monetary fines imposed for failure to file on time.

- Accuracy-related penalties: Imposed for inaccuracies or reporting errors.

- Underpayment penalties: For insufficient advance tax payments based on incorrect gain reporting.

Who Typically Uses Schedule D (Form 1120)

Schedule D (Form 1120) is predominantly used by:

- Corporations needing to report capital transactions: Including C corporations and certain real estate firms.

- Legal and accounting professionals: Assisting corporate clients with accurate tax filings.

- Corporate finance departments: Seeking to comply with federal tax regulations and report accurate financial data.

Business Entity Types

- C Corporations: Main filers of Schedule D as part of their comprehensive corporate tax return process.

- S Corporations: Though they pass income to shareholders, some capital gains may require reporting on a corporate tax basis.

This sectioned approach to understanding and utilizing Schedule D (Form 1120) ensures maximum clarity and utility for corporations dealing with capital gains and losses during the 2016 tax year.