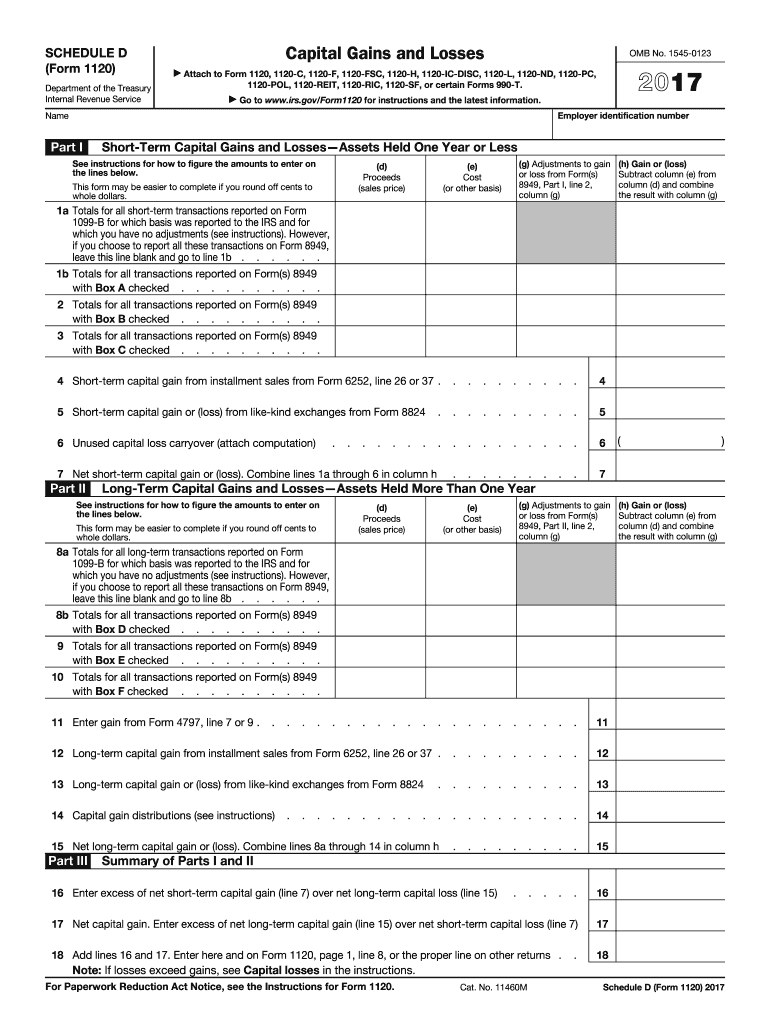

Definition and Purpose of Form Losses 2017

Form Losses 2017, officially known for its role in detailing capital losses, serves a critical function in the financial landscape. Primarily used by individuals and businesses to report capital losses incurred during the sale of assets, this form allows taxpayers to account for and calculate the impact of these financial transactions on their overall taxable income. Recognizing short-term versus long-term capital losses is central to its purpose, as each has distinct tax implications. Short-term losses stem from assets held for under a year, while long-term losses pertain to assets held for more than a year. Accurately distinguishing these losses is necessary to ensure compliance with tax regulations and to optimize potential tax savings.

How to Obtain Form Losses 2017

Acquiring Form Losses 2017 is a straightforward process. The form can be downloaded directly from the Internal Revenue Service (IRS) website, where a comprehensive collection of tax forms and instructions is available. This ensures that you have access to the most current version with accompanying guidelines critical for accurate completion. For individuals preferring offline options, local IRS offices provide physical copies upon request. Furthermore, tax software such as TurboTax or QuickBooks often includes this form as part of their tax filing packages, streamlining the process by integrating it into their digital workflow.

Steps to Complete Form Losses 2017

Filling out Form Losses 2017 involves a series of detailed steps. Begin by gathering all the necessary transaction records, ensuring you have accurate purchase and sale dates, as well as corresponding amounts. Calculate your capital losses by subtracting the sale price from the purchase price for each asset sold. Distinguish between short-term and long-term transactions and enter these figures into the appropriate sections. Verify all calculations meticulously to prevent errors. If using tax preparation software, the built-in functionality will prompt you for the required information and automatically perform the necessary calculations.

Who Uses Form Losses 2017

Form Losses 2017 is predominantly used by taxpayers, including individuals and various business entities, who have participated in the sale of capital assets within the tax year and have incurred a loss. This group often includes investors, stock traders, and real estate professionals. Businesses structured as corporations, LLCs, partnerships, and sole proprietorships may also require this form to accurately reflect their capital transactions and ensure tax compliance. Understanding who primarily engages with this form highlights its essential role in both personal and business financial management.

Important Terms Related to Form Losses 2017

Several critical terms are associated with Form Losses 2017, essential for understanding its completion and implications. These include:

- Capital Asset: Property such as stocks, bonds, or real estate that is acquired for investment purposes.

- Capital Loss: The loss incurred when a capital asset is sold for less than its purchase price.

- Short-Term Capital Loss: Loss from selling an asset held for less than one year.

- Long-Term Capital Loss: Loss from selling an asset held for more than one year.

- Net Capital Loss: The total capital loss after accounting for any capital gains in the same year.

Familiarity with these terms ensures accurate reporting and compliance with tax obligations.

IRS Guidelines for Form Losses 2017

The IRS provides clear guidelines for completing Form Losses 2017, ensuring that taxpayers can properly report their capital losses. These guidelines outline the necessary documentation, such as transaction receipts and financial statements, to support any claims made. Additionally, they specify the correct process for calculating net capital losses, including the detailed handling of carryover losses to future tax years. Adherence to these guidelines is crucial to prevent errors that could result in audits or penalties.

Filing Deadlines and Important Dates

Timeliness is a critical factor when dealing with Form Losses 2017. The form must be submitted in conjunction with an individual or business’s annual tax return, typically due by April 15 each year. However, if this date falls on a weekend or legal holiday, the deadline is extended to the next business day. For those needing additional time, filing for an extension must be done prior to the original deadline, granting an additional six months to finalize returns and avoid late filing penalties.

Required Documents for Completing Form Losses 2017

To accurately complete Form Losses 2017, specific documents are imperative. These include:

- Purchase Records: Proof of the purchase price and date for each asset.

- Sale Receipts: Documentation of the sale dates and amounts received.

- Financial Statements: Consolidated reports that align with the reported transactions.

- Brokerage Statements: Official records from financial institutions detailing asset transactions.

Ensuring these documents are organized and readily available simplifies the completion process and supports claims during audits.