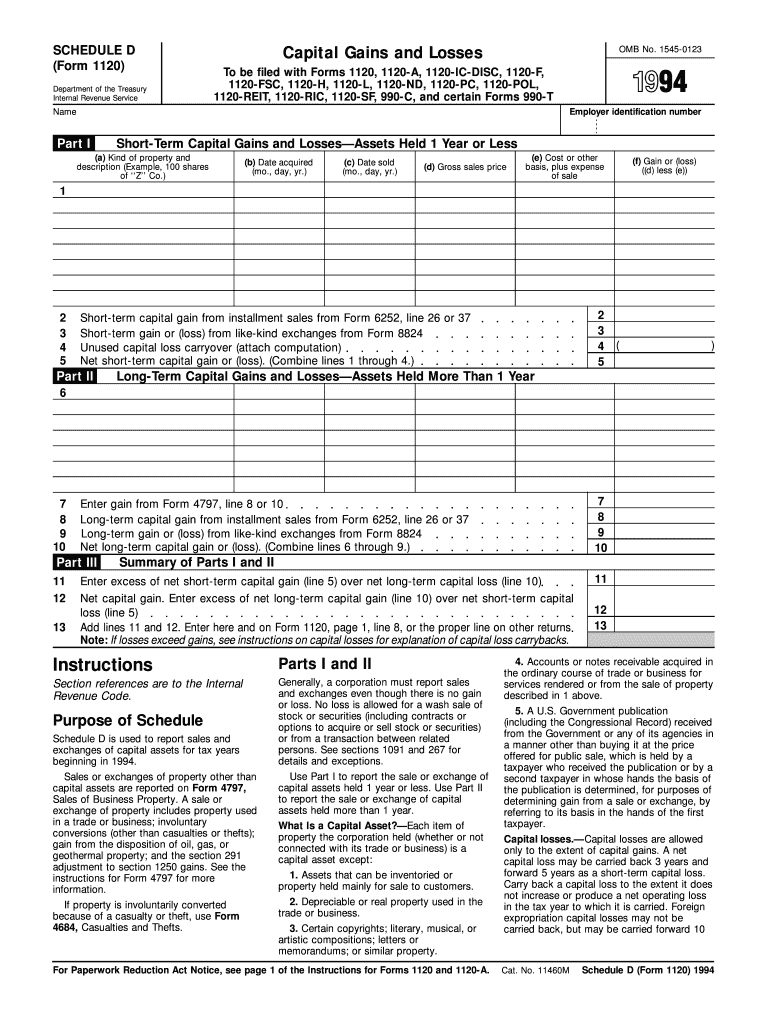

Definition and Purpose of the 1994 Form 1120

The 1994 Form 1120, also known as the U.S. Corporation Income Tax Return, is a document used by corporations in the United States to report their financial information to the IRS. This form plays a critical role in determining a corporation’s federal tax obligations. Generally, the form includes sections that solicit details about income, deductions, tax credits, and other relevant financial activities within a corporation. By completing this form, corporations ensure they comply with federal tax regulations while providing a transparent account of their fiscal year performance.

How to Obtain the 1994 Form 1120

Acquiring the 1994 Form 1120 for corporate tax reporting can be done through several avenues. You can visit the IRS website, where archived forms from prior years, including the 1994 version, are available for download. Alternatively, corporations can request a physical copy of the form by contacting the IRS directly. Other sources for obtaining this form include professional tax software that provides comprehensive access to historical tax documents needed for financial reporting.

Steps to Complete the 1994 Form 1120

Filling out the 1994 Form 1120 requires attention to detail and accuracy. Below are the outlined steps in completing this tax form:

-

Gather Necessary Documents: Ensure all financial statements, including income statements and balance sheets, are available as they are needed when completing various sections of the form.

-

Identify Income and Deductions: Properly categorize all revenue streams and allowable deductions. This may include operating income, dividends, and interest, along with business expenses and depreciation.

-

Complete All Schedules: If applicable, fill out corresponding schedules, such as Schedule C or Schedule J, which detail specific financial activities like dividends and Special Deductions for corporations.

-

Calculate Tax Liability: Using the provided formulas in the form, corporations should compute their total tax liability.

-

Finalize and Review: Before submission, review the form to ensure all entries are accurate and all sections are completed.

Important Terms Related to the 1994 Form 1120

Understanding specific terminology is vital when dealing with the 1994 Form 1120. Here are some key terms:

- Gross Income: The total revenue generated by a corporation before deductions or taxes.

- Net Operating Loss (NOL): A tax credit granted when a company's allowable tax deductions surpass its taxable income.

- Schedule M-1: A section that reconciles the difference between financial accounting net income and taxable income.

IRS Guidelines for the 1994 Form 1120

Adhering to IRS guidelines is mandatory for the proper completion and submission of the 1994 Form 1120. The IRS specifies instructions for all the form's segments, offering definitions and criteria for income categorization and deduction claims. It's crucial that corporations consider these guidelines to prevent misfiling, which could lead to penalties or audits.

Filing Deadlines for the 1994 Form 1120

Avoiding penalties involves meeting the designated deadlines for form submission. Typically, the 1994 Form 1120 must be filed by the 15th day of the third month after the end of the tax year—commonly March 15 for calendar-year filers. Extensions can be granted upon request, providing extra time for corporations that demonstrate needs due to specific circumstances, though penalties or interest on late tax payments may apply.

Required Documents for the 1994 Form 1120

Corporations are expected to have several documents on hand when completing the 1994 Form 1120. Important documents include:

- Income and Expense Summary: A detailed summary of the corporation’s gross income and expenditures.

- Capital Account Records: These help document changes in the ownership structure or financial stake.

- Prior Tax Returns: Useful for referencing and ensuring consistent reporting year over year.

Penalties for Non-compliance with the 1994 Form 1120

Failure to comply with submission requirements of the 1994 Form 1120 can result in significant penalties. Common penalties include late filing fees where the IRS charges a set percentage of the taxes unpaid by the due date. Additionally, there’s a failure-to-pay penalty escalating over time until the taxes are paid. Corporations can also face accuracy-related penalties if misleading statements are identified on the submitted forms, impacting the reported tax liability.

Business Entity Types Using the 1994 Form 1120

While the 1994 Form 1120 is primarily used by corporations, it's important to note that different entity types such as C corporations and certain LLCs operating as C corporations must file this form. Specifically, businesses choosing to be taxed as C Corporations report their earnings and outline respective tax responsibilities via this comprehensive tax document. It is not applicable for partnerships or sole proprietorships, which require different forms.

By understanding these aspects of the 1994 Form 1120, corporations can adeptly navigate tax reporting requirements, ensuring compliance and accurate submission to the IRS.