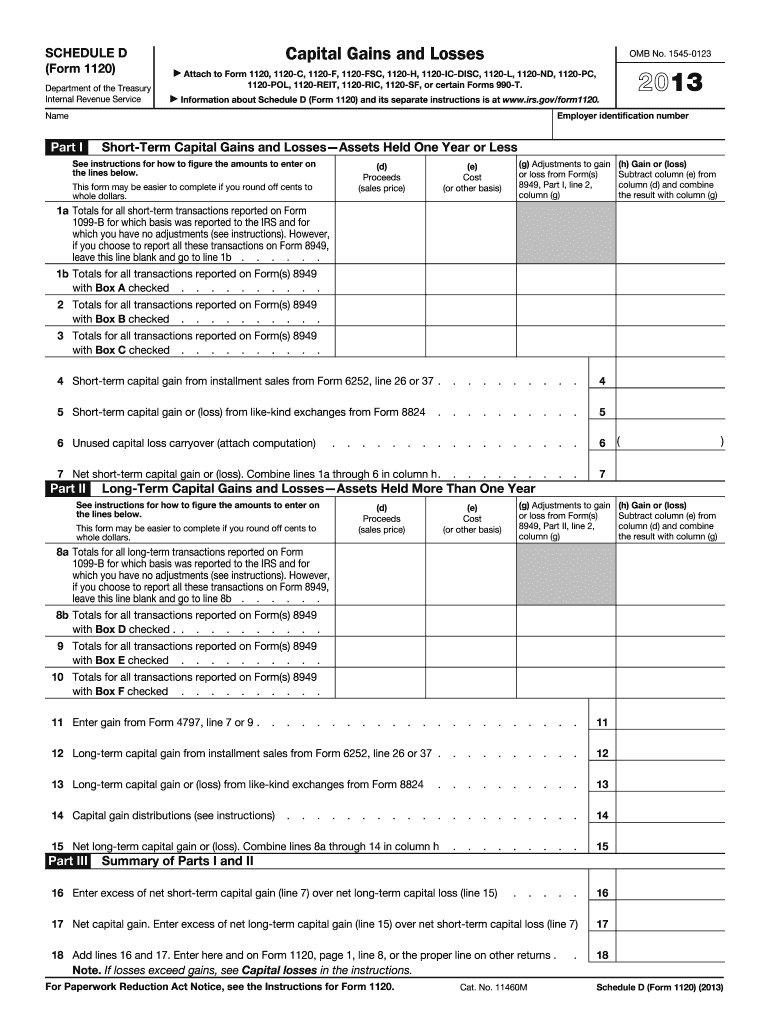

Definition and Purpose of the 2013 IRS Schedule D Form

The 2013 IRS Schedule D Form is used by individuals, partnerships, and corporations to report capital gains and losses that stem from the sale of investments or assets. This form is crucial for detailing short-term and long-term gains and losses, which are subjected to different tax rates. The primary purpose is to determine the overall net gain or loss, which ultimately impacts the taxpayer's income tax liability.

Important Sections of the Schedule D Form

- Short-term capital gains and losses: Transactions involving assets held for a year or less.

- Long-term capital gains and losses: Transactions involving assets held for more than a year.

- Capital loss carryover: Allows taxpayers to carry over a net capital loss exceeding a yearly threshold to future years.

How to Obtain the 2013 IRS Schedule D Form

The form can be obtained from the IRS website by searching for "Schedule D (Form 1040) 2013" or directly from tax preparation software commonly used, like TurboTax or H&R Block. Some local tax offices also provide physical copies. It's advisable to ensure the form corresponds specifically to the tax year 2013 to avoid discrepancies.

Steps to Access the Form Online

- Navigate to the IRS official website.

- Enter the form name "Schedule D (Form 1040) 2013" in the search bar.

- Download the PDF version for personal use.

Steps to Complete the 2013 IRS Schedule D Form

Completing the Schedule D Form requires careful attention to detail and accuracy, ensuring all capital transactions are reported:

- Identify all reportable transactions from your annual financial records.

- Calculate your short-term and long-term gains or losses, ensuring each is reported in its respective section.

- Apply any applicable capital loss carryover from previous years.

- Transfer totals to the appropriate lines of Form 1040.

Detailed Instructions

- Record details accurately: Include purchase date, sale date, cost basis, and sales proceeds.

- Balance entries: The form balances carryover losses and gains to compute the final net gain or loss.

Key Elements of the 2013 IRS Schedule D Form

The Schedule D Form contains multiple elements contributing to a comprehensive financial report:

- Part I: Governs short-term transactions.

- Part II: Concerns long-term transactions.

- Part III: Summarizes the aforementioned transactions and calculates the net capital gain or loss.

Additional Components

- Supplementary schedules: Such as 8949, sometimes needed for detailed sales and transfer records.

- Instructions booklet: Provides line-by-line guidance for completing the form appropriately.

Important Terms Related to the 2013 IRS Schedule D Form

Understanding specific terminology is vital for a complete and correct form:

- Capital Gains and Losses: Profits or losses from the sale of assets.

- Cost Basis: The original value of an asset, used to determine gains.

- Net Gain: Overall profit after subtracting losses and applicable deductions.

- Holding Period: Duration for which an asset was held, determining if the gain/loss is short-term or long-term.

IRS Guidelines for the Schedule D Form

IRS guidelines stipulate how different assets and losses should be reported:

- Deduction limits: Deductions are capped annually, with excess losses potentially rolled over.

- Documentation: Retain proof of purchase and sale for each transaction.

Common Situations

- Selling Stock: Requires reporting on Schedule D.

- Real Estate Sales: Special rules for main homes versus investment properties apply.

Penalties for Non-Compliance

Failure to accurately complete or submit the Schedule D Form can lead to penalties, including:

- Underreporting: Results in fines equivalent to a percentage of the unpaid tax.

- Late Filing: Carries interest and additional penalties over time.

Avoidance Tips

- Double-check figures and documentation.

- Submit by the tax deadline to avoid unnecessary interest or penalties.

Filing Deadlines and Important Dates for the 2013 IRS Schedule D Form

Timely submission is critical when dealing with tax obligations:

- Filing Deadline: Typically April 15 of the subsequent year.

- Extension Options: With Form 4868, which grants an additional six months to file without incurring penalties.

Planning for Future Years

- Track variations in tax law to stay informed and compliant.

- Set reminders to ensure deadlines are consistently met.

This comprehensive guide should assist any taxpayer in successfully navigating the complexities of the 2013 IRS Schedule D Form, providing clarity on its purpose, completion steps, and associated rules.