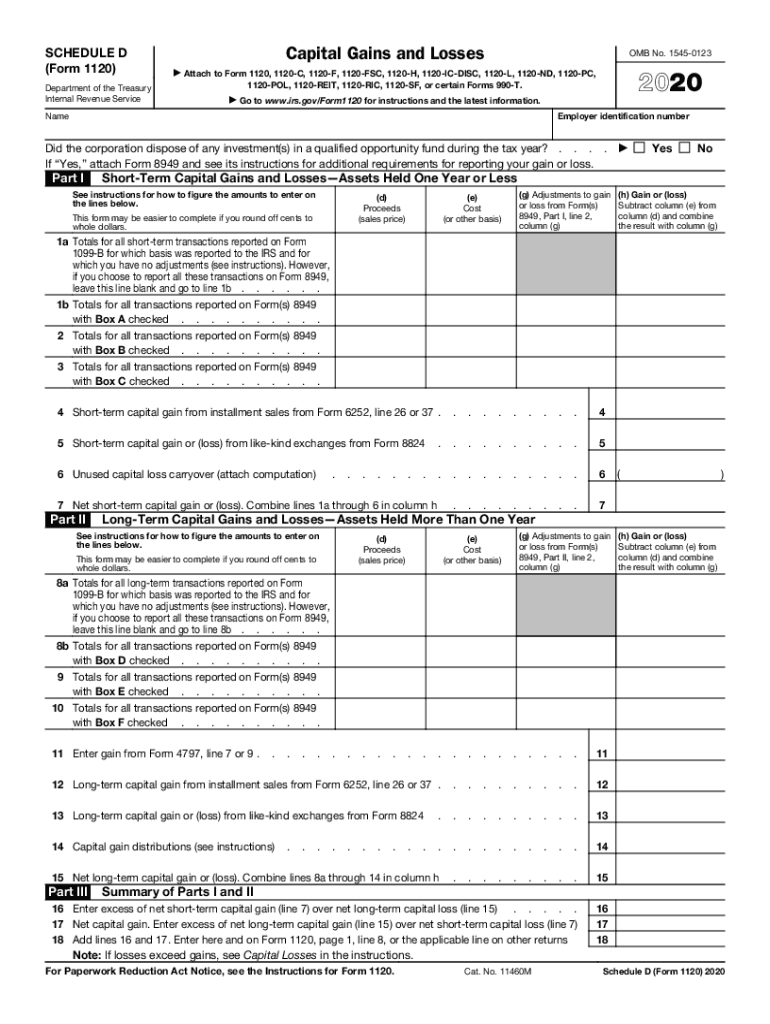

Understanding Schedule D for 2020

Schedule D (Form 1120) is a pivotal tax form utilized by corporations to report capital gains and losses for the 2020 tax year. This document is essential for detailing short-term and long-term capital transactions, with a focus on proceeds, costs, and necessary adjustments. Corporations must attach this schedule to their Form 1120 submissions and other related forms while following specific instructions for reporting gains or losses from qualified opportunity funds.

How to Use the 2020 Schedule D

Corporations need to provide a comprehensive report of their capital gains and losses using this schedule. It involves recording both short-term and long-term transactions. Each section requires details such as the date acquired, date sold, proceeds received, cost or other basis, and resulting gain or loss. Corporations must ensure accuracy in filling out this form as it directly impacts their tax obligations.

Steps to Complete the 2020 Schedule D

- Gather Required Documents: Ensure you have access to all financial records related to capital transactions, including purchase and sale documentation.

- Complete Short-Term Capital Gains and Losses: Fill in Part I of the form, detailing transactions held for one year or less.

- Report Long-Term Capital Gains and Losses: Use Part II to report transactions held for more than one year.

- Calculate Totals: Add together the figures to determine net short-term and long-term capital gains or losses.

- Finalize Documentation: Transfer totals to Form 1120 as required, ensuring congruity between forms.

Key Elements of the 2020 Schedule D

- Identification Details: The top section of the form requires standard identification information related to the corporation.

- Detailing Transactions: Separate sections for short and long-term capital gains or losses.

- Comprehensive Reporting: Requires meticulous detailing of dates, proceeds, costs, and category identifiers.

Important Terms Related to the 2020 Schedule D

- Short-Term Capital Gain/Loss: Gains or losses from asset sales held for one year or less.

- Long-Term Capital Gain/Loss: Gains or losses from asset sales held for more than one year.

- Basis: Initial cost of an asset, crucial for calculating gain or loss.

- Qualified Opportunity Fund: An investment vehicle that provides tax incentives for investing in specific regions.

Filing Deadlines and Important Dates

For the 2020 tax year, corporations typically needed to submit their tax returns by April 15, 2021. However, extensions are available under certain conditions. It's crucial for corporations to keep abreast of any changes in IRS deadlines, which can vary and often depend on broader economic or social circumstances.

Required Documents for Filing

- Transaction Records: Includes documentation of dates, sale proceeds, and initial costs.

- Supporting Financial Statements: Relevant financial statements that correlate with transactions on the Schedule D.

- Form 1099: May be needed to substantiate income reported.

IRS Guidelines and Compliance

The IRS provides detailed instructions on how to properly fill out Schedule D, which are accessible on their official website. Compliance with IRS guidelines ensures accurate reporting of capital gains and losses, reducing the risk of discrepancies and potential penalties.

Business Entities Utilizing 2020 Schedule D

Corporations, particularly those with active trading or asset management structures, primarily use Schedule D. It is fundamental for entities involved in frequent buying and selling of assets, ensuring precise calculation and reporting of gains.

Penalties for Non-Compliance

Failure to accurately report capital gains and losses or to file in a timely manner can result in penalties from the IRS. These fines can be substantial and may also include interest on overdue taxes. It's imperative for corporations to adhere strictly to reporting guidelines and deadlines to avoid such outcomes.

By providing a thorough understanding and detailed guidelines, corporations can confidently navigate the complexities of the 2020 Schedule D, ensuring complete and accurate submission of their financial activities for the respective tax year.