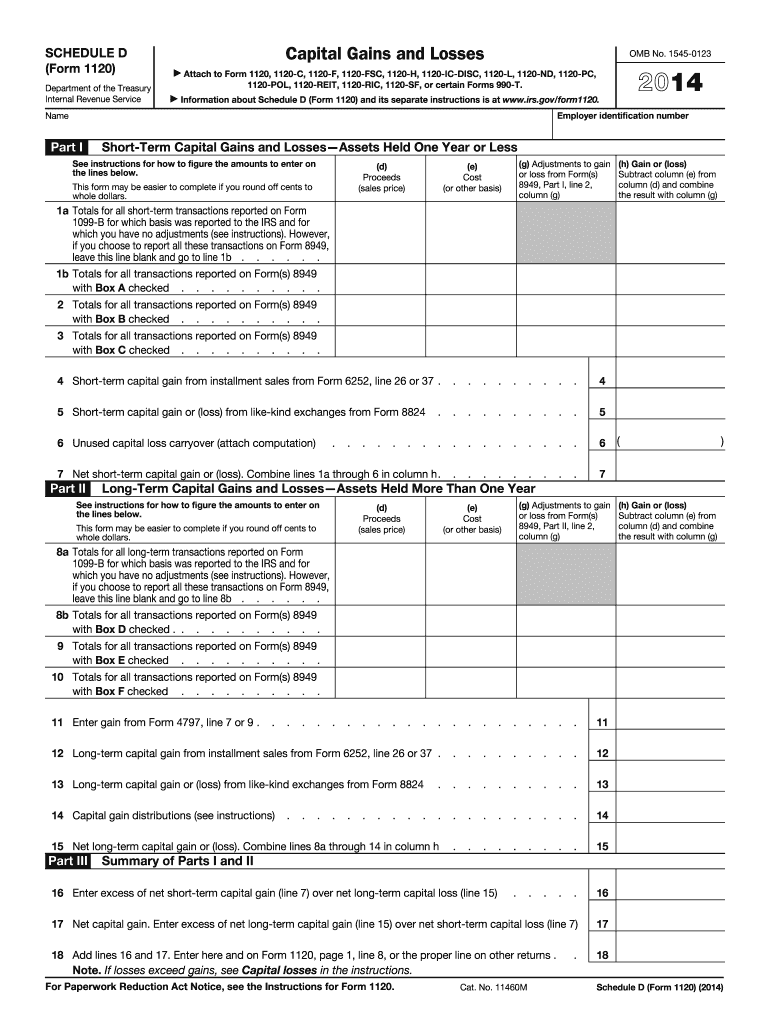

Definition and Purpose

The Schedule D (Form 1120) is used by corporations in the United States to report capital gains and losses realized from the sale of assets. It functions as a supporting document for various corporate tax returns and is essential for accurately calculating taxable income related to these transactions. The form includes sections for both short-term and long-term capital transactions, requiring detailed data on the proceeds and costs associated with asset sales.

Key Features

- Short-Term Transactions: Captures gains or losses from assets held for one year or less.

- Long-Term Transactions: Focuses on assets held for more than one year.

- Attachment Requirement: Must be attached to the corporation’s primary tax return when filed.

How to Use the 2014 Schedule D Form

Using the 2014 Schedule D involves a meticulous process of documenting capital gains and losses. The following steps provide a structured approach to complete this form:

- Gather Documentation: Collect records of asset sales, including purchase price, sale price, and relevant dates.

- Classify Transactions: Determine if each transaction is short-term or long-term based on the holding period.

- Calculate Gains or Losses: Compute the difference between the sale price and the original purchase price for each asset.

- Complete Form Sections: Enter the transaction details into the appropriate sections of the form.

Practical Tips

- Accurate Record-Keeping: Maintain comprehensive records throughout the year to simplify this process.

- Software Compatibility: Consider using tax preparation software compatible with Schedule D to improve accuracy and efficiency.

How to Obtain the 2014 Schedule D Form

To access the 2014 Schedule D Form, taxpayers have several options:

- IRS Website: The form can be downloaded directly from the official Internal Revenue Service website.

- Tax Software: Many tax preparation programs include the Schedule D form as part of their filing package.

- Tax Professionals: Accountants and tax professionals typically have copies of required forms and can assist in obtaining them.

Additional Sources

- Local IRS Offices: Physical copies may be available at local IRS offices or by request via mail.

- Libraries: Some public libraries provide copies of tax forms, especially during tax season.

Steps to Complete the 2014 Schedule D Form

Completing the 2014 Schedule D Form involves a series of detailed steps:

- Fill Personal Information: Enter the corporation’s name and employer identification number at the top of the form.

- Record Short-Term Gains/Losses: Utilize Part I to enter and compute short-term transactions.

- Document Long-Term Gains/Losses: In Part II, report proceeds and costs for long-term assets.

- Totals and Net Gains/Losses: Calculate the totals for short-term and long-term and determine overall net gain or loss.

- Transfer Totals: Transfer the final totals to the corporation’s primary tax return.

Common Mistakes to Avoid

- Incorrect Classification: Incorrectly categorizing assets as short-term or long-term.

- Misplaced Figures: Entering values in incorrect sections of the form.

Who Typically Uses the 2014 Schedule D Form

The 2014 Schedule D Form primarily serves certain business entities:

- Corporations: Both C-corporations and S-corporations utilize this form to report asset sales.

- Investment Firms: Companies dealing heavily in securities often have multiple transactions to report.

- LLCs Treated as Corporations: Limited liability companies that are taxed as corporations also require this form.

Edge Cases

- Disregarded Entities: Single-member LLCs seen as separate entities for tax purposes may need specific advice on usage.

Key Elements of the 2014 Schedule D Form

Understanding the crucial elements of the form is vital:

- Part I: Short-term capital gains and losses.

- Part II: Long-term capital gains and losses.

- Reporting Sections: Designated lines for details such as proceeds and basis of transactions.

Detailed Sections

- Proceeds: Gross revenue from asset sales.

- Basis: Original cost of assets, critical for calculating capital gains or losses.

IRS Guidelines and Regulations

The Internal Revenue Service provides specific guidelines for completing the Schedule D:

- Accuracy: Ensures accurate reporting of gains and losses to calculate correct tax obligations.

- Compliance: Adherence to IRS instructions minimizes the risk of audits and penalties.

Compliance Measures

- Proper Documentation: Verify all reported figures with supporting documentation.

- Adjustment Entries: Incorporate any necessary adjustments for correct reporting.

Filing Deadlines and Important Dates

Timeliness is crucial for compliance with IRS regulations:

- Tax Filing Deadline: Schedule D must be filed with the corporation’s tax return by the standard filing deadline, typically April 15.

- Extensions: Extensions are available, but Schedule D must still meet updated deadlines.

Considerations for Delays

- Late Filing Penalties: Failure to file on time may result in fines unless extensions are secured.

- Audit Risk: Late or inaccurate submissions can trigger audits.