Definition & Meaning

The capital loss carryover worksheet is a tax-related financial document used by individuals and corporations in the U.S. to determine how much of their capital losses from previous years can be applied to current tax filings. This worksheet is crucial for taxpayers who have incurred capital losses exceeding the annual deductible limit, currently set by the IRS at $3,000 ($1,500 if married filing separately). By employing this worksheet, taxpayers can methodically document and offset their capital gains with the precise amount of prior losses, ensuring accurate and optimal tax liability management.

How to Use the Capital Loss Carryover Worksheet

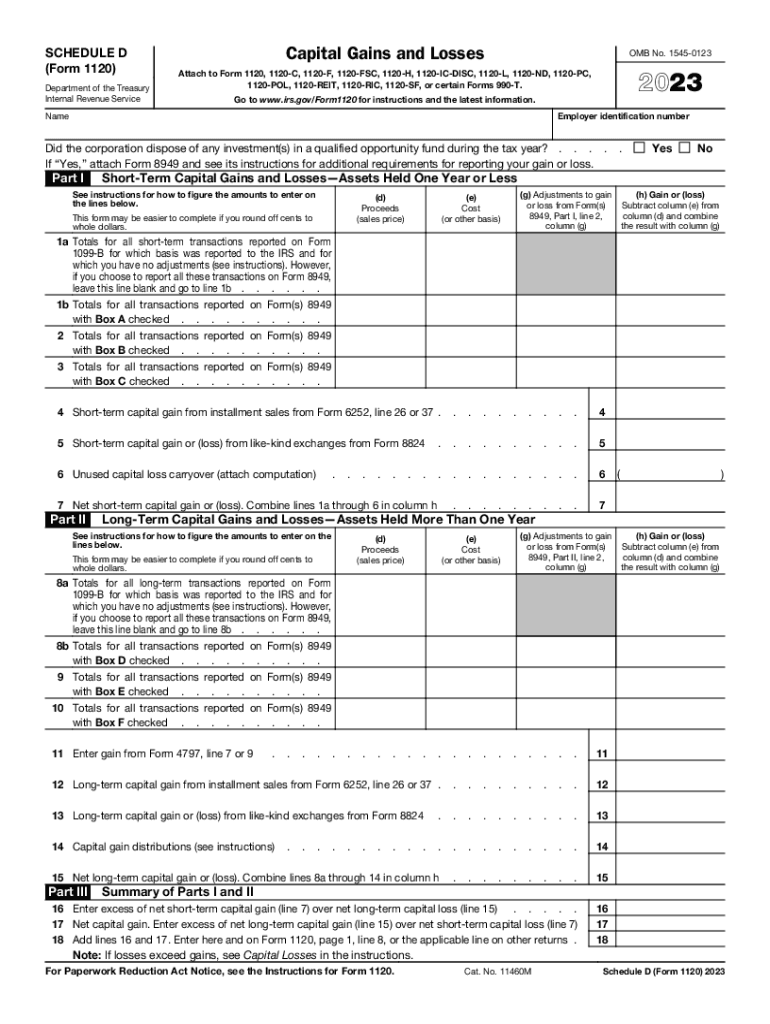

Taxpayers can navigate the capital loss carryover worksheet with a structured approach. The process begins by accurately gathering the past year’s Schedule D form, as this will be necessary for reference. The worksheet requires the documentation of the total capital loss incurred, the amount previously deducted against ordinary income, and any remaining losses eligible for carryover. Once these figures are identified, they should be recorded in the respective sections of the worksheet. The final step involves calculating the allowable carryover for both short-term and long-term capital losses, typically offsetting gains in taxable income with these figures across future tax years until fully utilized.

Steps to Complete the Capital Loss Carryover Worksheet

- Gather Documentation: Collect all previous tax returns, especially forms like Schedule D, to retrieve historical loss data.

- Calculate Total Capital Loss: Accumulate the total losses from prior years' transactions involving real estate, stocks, or other capital assets.

- Determine Annual Deductions: Identify how much loss, from up to $3,000 annually, has been offset against ordinary income.

- Residual Loss Calculation: Subtract the used loss amount from the total accrued losses to find the remaining carryover.

- Allocate Loss Categories: Divide remaining losses into short-term and long-term categories for future tax offsets.

- Documentation: Accurately document these calculations on the worksheet and reference in subsequent tax filings.

Key Elements of the Capital Loss Carryover Worksheet

The worksheet contains several critical sections, including short-term and long-term loss entries. Taxpayers must accurately record adjusted gross income (AGI) implications, ensuring appropriate deductions are taken only from gains and ordinary income limits outlined by IRS regulations. Specific lines and entries might also require additional documentation, such as purchase and sale records or Form 1099-B reporting details. Precise computation during each tax year ensures maximized future carryover potential, essential for strategically managing the impact of past financial losses.

Important Terms Related to Capital Loss Carryover Worksheet

- Capital Gains and Losses: Profits and losses arising from the disposal of assets, consolidated under different tax forms for IRS reporting.

- Short-Term vs. Long-Term: Distinctions based on the duration an asset is held, impacting both the tax rates and carryover qualifications.

- Ordinary Income Limit: Preset IRS limits on capital loss deductions impacting taxable income.

- Carryover: Unused capital loss amounts transferred across tax periods to decrease future liabilities.

IRS Guidelines

The IRS provides specific regulations for the implementation and utilization of the capital loss carryover worksheet. These include specifications for reporting timelines, necessary accompanying forms like Schedule D, and compliance with anti-abuse rules that prevent improper deductions. Taxpayers are obligated to adhere to these guidelines meticulously to avoid discrepancies or penalties during IRS audits. Familiarity with yearly IRS updates or modifications to the regulations is advised to ensure ongoing compliance and correct usage.

Software Compatibility (TurboTax, QuickBooks, etc.)

Many tax preparation platforms, such as TurboTax and QuickBooks, naturally integrate the use of the capital loss carryover worksheet into their systems, helping automate the calculation process. Users can input their financial data, and these software solutions can generate accurate worksheets and forms ready for IRS submissions. Compatibility with these platforms allows taxpayers to focus on accurate data entry, as they systematically handle compliance, calculation, and submission protocols, providing a user-friendly approach to managing complex tax scenarios.

Filing Deadlines / Important Dates

Timely filing of tax documents, including those involving carryovers, aligns with the IRS’s standard tax deadline, typically on April 15. It is pivotal to adhere to these timelines to avoid penalties. Calendar reminders for quarterly estimated payments or extensions should be set, ensuring comprehensive preparatory work is finalized ahead of deadlines. Discrepancies or questions should ideally be remedied well before these dates, allowing adequate time for corrections or additional clarifications with IRS correspondence if necessary.