Definition and Meaning

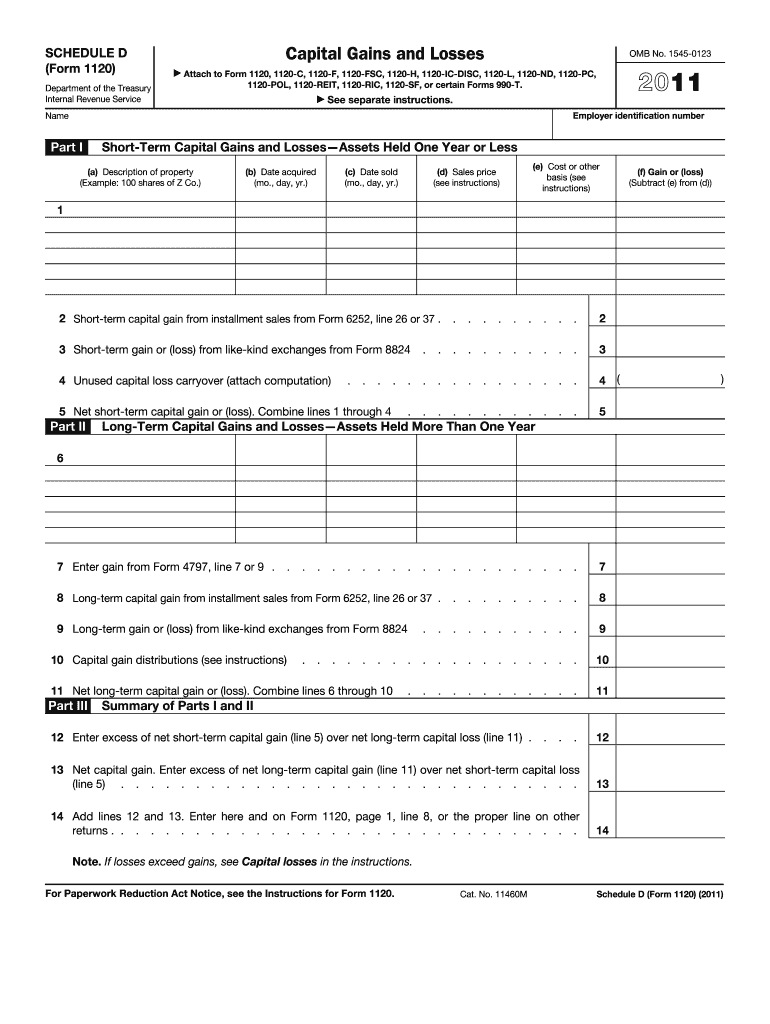

The 2011 Schedule D Form is specifically used by taxpayers to report capital gains and losses that occur from the sale of assets. It is a crucial part of the tax filing process for individuals and entities that have engaged in transactions involving capital assets. The form helps in calculating the net capital gain or loss, which ultimately impacts the total taxable income reported. Taxpayers use this form to break down gains and losses into short-term and long-term categories, depending on the duration for which the asset was held, following the IRS guidelines.

Key Elements of the 2011 Schedule D Form

The Schedule D Form includes several essential sections:

-

Part I: Short-Term Capital Gains and Losses - This section records transactions involving assets held for one year or less.

-

Part II: Long-Term Capital Gains and Losses - This records the transactions of assets held for more than one year, which typically receive a more favorable tax rate compared to short-term gains.

-

Part III: Summary - This part totals the figures from Parts I and II to provide a net capital gain or loss figure, which is then transferred to other forms, such as Form 1040 for individuals or Form 1120 for corporations.

How to Use the 2011 Schedule D Form

To effectively use the Schedule D Form, ensure you follow these steps:

-

Gather Necessary Information - Collect details on each capital asset transaction, including acquisition and sale dates, cost basis, and sales price.

-

Categorize Transactions - Determine if each transaction falls into the short-term or long-term category based on the holding period.

-

Fill Out the Form - Use the collated data to complete Parts I and II of the form accurately.

-

Calculate the Net Gain or Loss - In Part III, summarize the computations from the previous parts to arrive at a net gain or loss figure.

-

Attach to Your Main Tax Return - Depending on your tax status, this could be Form 1040 for individual filers or Form 1120 for corporations.

How to Obtain the 2011 Schedule D Form

The form can be acquired through several avenues:

-

Directly from the IRS Website - Downloadable PDFs are available for printing and manual completion.

-

Request by Mail - The IRS provides a service to send physical copies upon request.

-

Tax Preparation Software - Most modern tax filing applications such as TurboTax or H&R Block include the option to fill out Schedule D electronically.

Important Terms Related to the 2011 Schedule D Form

Understanding specific terminology is crucial for accurately completing the form:

-

Cost Basis - The original value of an asset, adjusted for any splits, dividends, or return of capital distributions that may have occurred.

-

Capital Asset - Any significant piece of property such as stocks, bonds, or real estate that is bought for investment purposes.

-

Net Capital Gain - The positive difference after summing all individual gains and losses.

-

Holding Period - The length of time an asset is held before being sold, which determines its categorization as short-term or long-term.

Filing Deadlines and Important Dates

Compliance with filing deadlines is essential to avoid penalties:

-

April 15th - The standard deadline for filing individual tax returns, which includes Schedule D for reporting any capital gains or losses.

-

Extensions - If unable to file by this date, taxpayers may file Form 4868 for an automatic six-month extension, although any owed taxes must still be paid by the original deadline to avoid interest and penalties.

Penalties for Non-Compliance

Failing to accurately complete and file the 2011 Schedule D Form can result in various penalties:

-

Underreporting Penalty - If the IRS finds unreported capital gains, penalties may apply for underpayment of taxes.

-

Late Filing Penalty - Charged at 5% of the unpaid tax for each month the return is late, up to a maximum of 25%.

-

Accuracy-Related Penalty - If errors are due to negligence or substantial understatement of income, the penalty is 20% of the underpaid amount.

IRS Guidelines

The IRS provides extensive guidance for completing the Schedule D Form:

-

Instructions for Schedule D - Available directly on the IRS website, providing detailed breakdowns and examples to assist in properly filling out each section.

-

Publication 544 - Offers further insight into the treatment of capital assets, providing context for correctly categorizing and calculating gains and losses.