Definition & Meaning

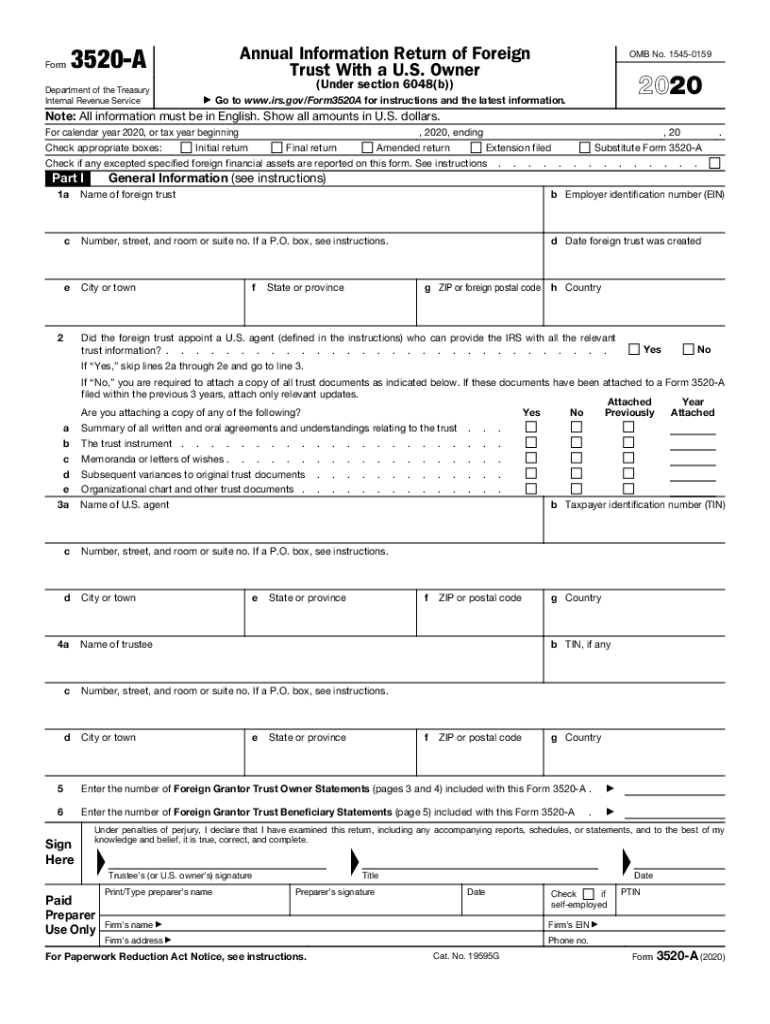

Form 3520-A is an Annual Information Return of a Foreign Trust with a U.S. Owner, as mandated by the IRS. It serves a critical function by documenting information about foreign trusts, including their creation, operations, and financial details pertaining to any U.S. owners. This includes the appointment of U.S. agents, income, expenses, and distributions to U.S. owners and beneficiaries. This form is vital in ensuring transparency and compliance with IRS regulations concerning offshore trusts.

How to Obtain Form 3520-A

To obtain Form 3520-A, you can download it directly from the IRS website in a PDF format. The form is accessible for free, providing instructions and details needed for accurate completion. If preferred, professional tax preparation services or tax software like TurboTax and QuickBooks often include Form 3520-A in their suite of tools, offering guidance through the process with automated features.

Steps to Complete the Form 3520-A

- Gather Information: Collect all relevant data regarding the foreign trust, including trust creation documents, financial statements, and details of U.S. beneficiaries.

- Enter General Information: Start with the trust's identifying information, such as the trust's name, the trustee’s details, and the Employer Identification Number (EIN).

- Report Financial Details: Include information on the trust’s financial activities, such as income, expenses, distributions to beneficiaries, and the trust’s balance sheet.

- Appoint a U.S. Agent: If applicable, provide details about the U.S. agent authorized to receive legal documents for the trust.

- Complete Compliance Statements: Ensure the trust complies with IRS regulations by completing necessary declarations.

- Review and Sign: Carefully review the form to ensure accuracy and complete all required signatures by the trustee or authorized person.

Filing Deadlines / Important Dates

Form 3520-A must be filed by the 15th day of the third month following the end of the trust’s tax year. For trusts operating on a calendar year basis, this deadline falls on March 15th. In case more time is needed, the trust can file IRS Form 7004 to request an automatic six-month extension.

Penalties for Non-Compliance

Failure to file Form 3520-A accurately and timely can result in substantial penalties. The IRS may impose a fine of the greater of $10,000 or 5% of the gross value of the trust's assets for each month the failure continues, capping at 25% of the trust's asset value. It is crucial to adhere strictly to submission deadlines and reporting requirements to avoid these punitive measures.

Required Documents

To complete Form 3520-A, you will need:

- Detailed financial accounts of the trust for the tax year.

- Copies of trust creation agreements.

- Records of all distributions made to U.S. owners or beneficiaries.

- Identification information of the trust and its U.S. agent.

Having these documents readily available ensures a smooth and precise filing process.

IRS Guidelines

The IRS provides a comprehensive set of guidelines on how to fill out Form 3520-A. These include instructions on what constitutes a foreign trust with a U.S. owner, the necessary financial details to report, and explanations of each part of the form. It is recommended to thoroughly review these guidelines to ensure compliance and accuracy.

Important Terms Related to Form 3520-A

- Foreign Trust: A trust characterized as foreign if primarily administered outside the U.S. and/or if U.S. courts do not have jurisdiction over its primary administration.

- U.S. Owner: A U.S. person who directly or indirectly owns any portion of a foreign trust.

- U.S. Agent: A U.S. resident designated to accept service of process for the trust for any IRS proceeding regarding the trust.

Understanding these terms is crucial for properly addressing the responsibilities associated with Form 3520-A.