Definition and Meaning

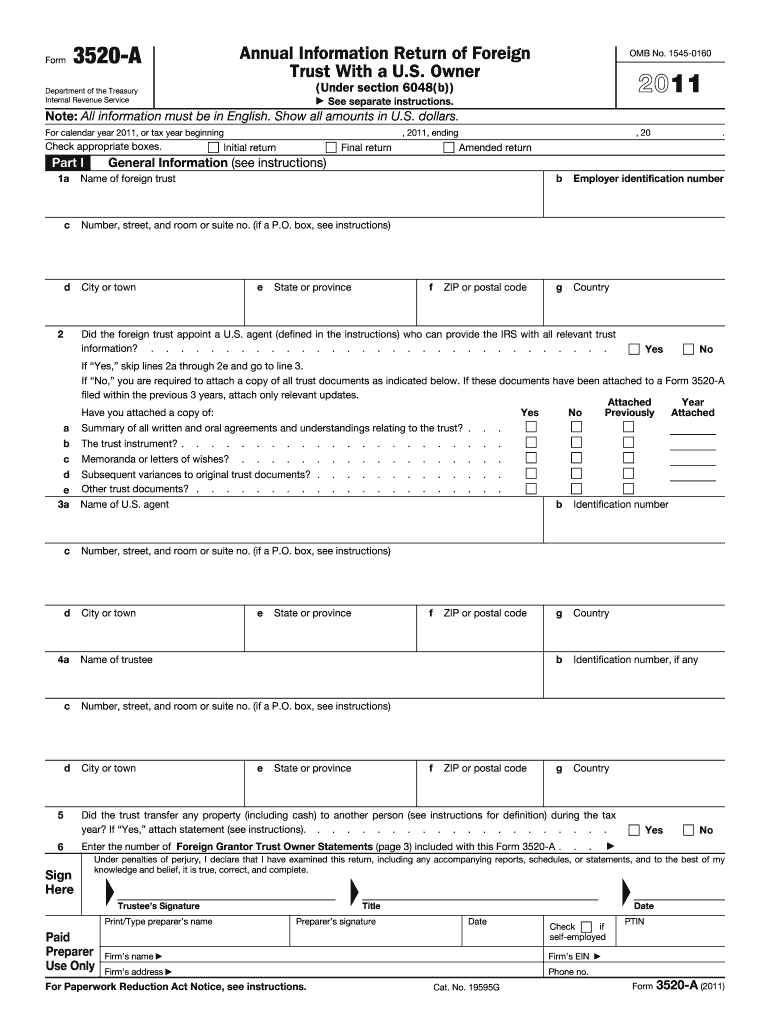

Form 3520, specifically for the tax year 2011, is an information return used to report certain transactions with foreign trusts, ownership of foreign trusts by U.S. persons, and receipts of certain large gifts or bequests from foreign persons. It is distinct from tax returns and is not used for calculating taxes owed. Instead, it ensures compliance with U.S. reporting requirements for those involved with foreign trusts and entities.

- Foreign Trust Transactions: Any U.S. person who transferred property to a foreign trust or received a distribution from one in 2011 is required to file Form 3520.

- Foreign Gifts: Reporting is also necessary for large gifts from foreign persons, typically exceeding $100,000 from non-resident aliens and foreign estates.

- Ownership: Disclosing ownership of foreign trusts is essential, even if no transactions occurred during the year.

How to Use the 2011 Form 3520

The 2011 Form 3520 serves as a critical compliance document to ensure transparency in international financial arrangements involving U.S. taxpayers.

- Reporting Mechanism: Utilize the form to report extensive details about the foreign trust, including the trust’s financial activities, income, and beneficiaries.

- Gift Reporting: Report significant gifts or bequests not included in gross income but relevant for monitoring potential tax evasion.

- Documentation: Ensure all pertinent records are organized to support each transaction or gift being reported.

Steps to Complete the 2011 Form 3520

Completing the 2011 Form 3520 requires attention to detail and an understanding of international financial dealings.

- Gather Necessary Information: Collect data regarding the foreign trust, including financial statements, trust deeds, and transaction records.

- Complete Identification Details: Fill out the form’s initial sections with your personal information and the tax year.

- Detail Trust Transactions: Provide a comprehensive account of any involvement with a foreign trust, including transfers, distributions, and related parties.

- Report Gifts and Bequests: List foreign gifts exceeding the established threshold and gifts from foreign corporations or partnerships.

- Review and Submit: Double-check all entries for accuracy, then submit the form to the IRS by the required deadline.

Important Terms Related to the 2011 Form 3520

Understanding key terms is crucial when dealing with Form 3520.

- Foreign Trust: A legal arrangement established outside the U.S. where the trustee holds property for beneficiaries.

- Grantor: An individual who establishes a trust and transfers assets into it.

- Distributions: Payments or transfers of assets from a trust to beneficiaries.

- Bequests: Transfers of property from an estate, typically received through a will.

Legal Use of the 2011 Form 3520

Ensuring legal compliance when filing the 2011 Form 3520 is essential.

- U.S. Tax Law Compliance: The form aligns with the Internal Revenue Code, particularly sections relating to foreign trusts.

- Avoidance of Penalties: Proper filing prevents substantial penalties for non-compliance or inaccuracies.

- Disclosure Assurance: Ensures that all international transactions and assets are transparent to the IRS.

IRS Guidelines

The IRS provides specific guidelines for the 2011 Form 3520 to ensure the form is filled out correctly.

- Filing Instructions: Detailed instructions are provided by the IRS, highlighting the information required for each section.

- Penalties: Non-compliance may result in significant financial penalties, potentially 35% of the gross reportable amount for unreported trusts.

- Resources: IRS resources are available to help clarify doubts and assist with the completion of this complex form.

Filing Deadlines and Important Dates

Timeliness is crucial when filing the 2011 Form 3520.

- Deadline: Form 3520 is generally due on April 15 of the year following the relevant tax year, aligning with income tax return deadlines.

- Extensions: If filing an income tax return extension, ensure it covers Form 3520 submission.

- Late Filing Consequences: Late submissions risk financial penalties that can exacerbate compliance issues.

Penalties for Non-Compliance

There are severe consequences for failing to file the 2011 Form 3520 accurately and timely.

- Financial Penalties: Penalties for non-filing can start at $10,000, with potential increases depending on the unreported amount involved.

- Increased IRS Scrutiny: Non-compliance may trigger audits or additional IRS scrutiny into other aspects of personal or business finances.

- Legal Implications: In extreme cases, systemic non-compliance can result in legal action beyond financial penalties.