Definition & Meaning

The "Reminder to U.S. Owners of a Foreign Trust" serves as a critical notification to U.S. individuals who hold ownership interests in foreign trusts. This document is a crucial compliance tool, reminding owners of their tax obligations under U.S. law. A U.S. owner of a foreign trust is typically required to report certain details about the trust, including its income and distributions, to the Internal Revenue Service (IRS). This form helps ensure transparency and adherence to U.S. tax regulations. It's essential for owners to understand that failing to comply could result in significant penalties.

How to Use the Reminder to U S Owners of a Foreign Trust

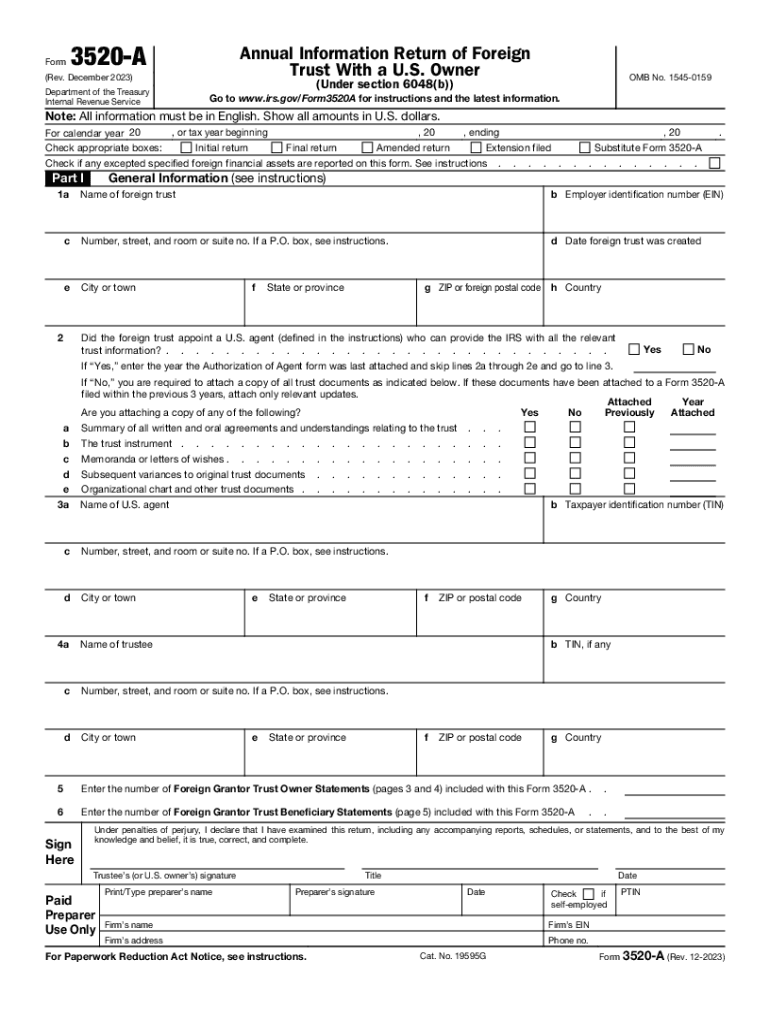

Utilizing the reminder efficiently involves a series of steps designed to align the owner with IRS requirements. U.S. owners must gather pertinent information about the foreign trust, such as the income generated, distributions made, and any changes in ownership throughout the year. This reminder serves as an aid to prepare for filing the necessary forms, such as the Form 3520 and Form 3520-A, which are integral in reporting and paying any applicable taxes on foreign trust income.

- Information Gathering: Assemble all financial details regarding the foreign trust.

- Form Utilization: Use the information to accurately complete Form 3520 or 3520-A.

- Filing and Documentation: Submit the required documentation by the specified IRS deadlines to avoid penalties.

Steps to Complete the Reminder to U S Owners of a Foreign Trust

Completing the form involves a structured process that ensures all necessary information is captured accurately:

- Identify the Trust Details: Include details such as the trust's name, creation date, and the role of the U.S. owner.

- Collect Financial Data: Document trust income, expenses, and distributions in U.S. dollars.

- Compile Trustee Information: Record trustee names and contact information.

- Report Distributions: Indicate any distributions made to U.S. beneficiaries, specifying amounts and recipients.

- Review and Verify: Ensure all information is accurate before submission.

- Submit the Form: File with the IRS through the designated method, whether electronically or by mail.

Filing Deadlines / Important Dates

Filing deadlines are crucial for maintaining compliance and avoiding penalties. The annual deadline for submitting Form 3520-A is March 15th, though it may vary slightly if it falls on a weekend or holiday. Form 3520 must usually be filed by the same date as the owner's income tax return, including any extensions. It's advisable to verify current IRS deadlines each year as they may change and ensure extensions are filed if additional time is needed.

Required Documents

To complete the reminder effectively, specific documents must be collected:

- Financial Statements: Income statements, balance sheets, and records of distributions from the foreign trust.

- Trust Deeds and Agreements: Documentation detailing the trust's legal foundation.

- Trustee Reports: Reports from trustees that summarize annual activities and changes.

- Beneficiary Lists: Details about U.S. beneficiaries and distributions received.

These documents provide a comprehensive overview of the trust's operations, ensuring accuracy in the information reported to the IRS.

IRS Guidelines

The IRS provides clear guidelines regarding the responsibilities of U.S. owners of foreign trusts. Owners must use Form 3520 to report certain transactions, while Form 3520-A functions as the trust's annual information return. These forms are used to disclose all activities involving the trust, including the receipt of distributions and any U.S. beneficiaries. Owners must ensure they follow IRS instructions precisely to avoid the substantial penalties associated with non-compliance.

Penalties for Non-Compliance

Non-compliance with filing requirements can result in severe financial penalties. Failing to file Form 3520 or 3520-A can lead to penalties ranging from $10,000 to a percentage of the trust’s undisclosed income. Additionally, incorrect or incomplete information can trigger further evaluations or audits by the IRS, increasing the risk of additional fines. These penalties underline the importance of adhering to all IRS requirements for foreign trust reporting.

Disclosure Requirements

Disclosure requirements are strict and necessitate complete transparency regarding foreign trusts. U.S. owners must report all financial activities, including income, principal distributions, and any changes in trust ownership. This degree of disclosure is vital for tax compliance, ensuring that the U.S. tax authorities have clear insight into the financial transactions and structures that potentially affect U.S. taxation of foreign trust income.