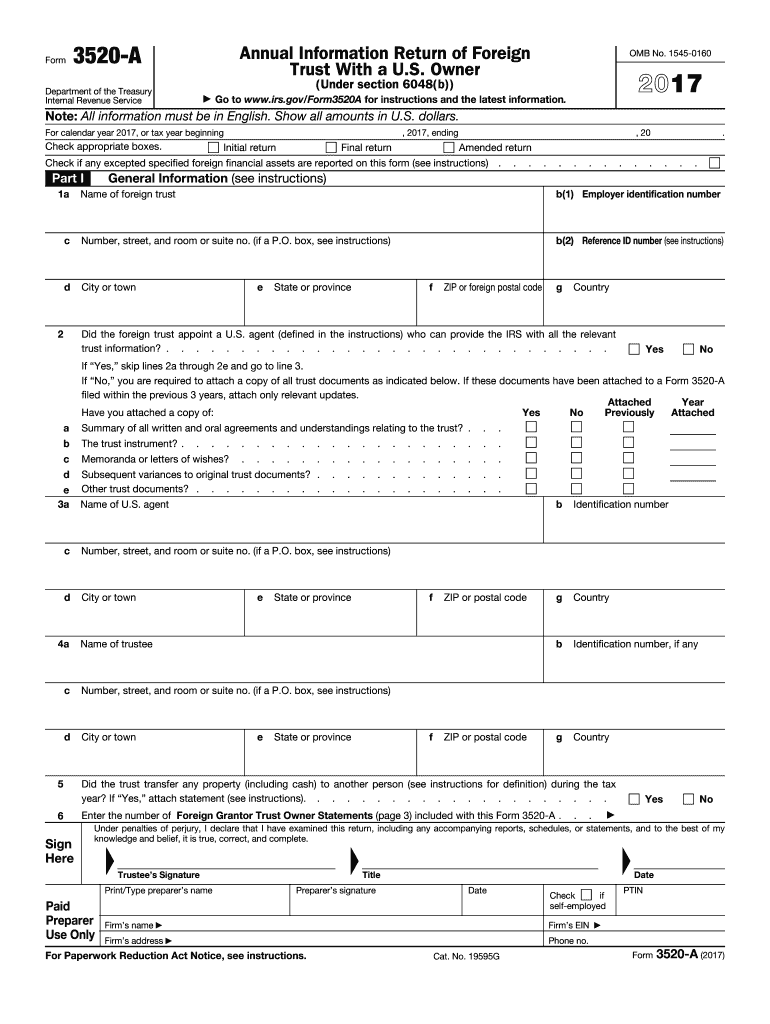

Definition & Meaning

Form 3520 is an informational return used by U.S. persons to report certain transactions with foreign trusts, ownership of foreign trusts, and receipt of certain large gifts or bequests from foreign entities. The 2017 version of this form specifically pertains to the tax year 2017. The IRS requires this form to ensure compliance with U.S. tax laws regarding foreign assets and income. It is not used to calculate taxes owed, but rather to provide information that supports overall tax compliance.

Who Typically Uses the IRS 3 Form

This form is generally used by U.S. individuals, including citizens and residents, who have had interactions involving foreign trusts or who have received large gifts from foreign persons. Specifically, those who must file include:

- U.S. owners of portions of foreign trusts.

- Beneficiaries of distributions from foreign trusts.

- Receivers of gifts or inheritances from foreign entities exceeding certain thresholds.

Understanding who needs to file is crucial for ensuring compliance and avoiding penalties.

How to Obtain the IRS 3 Form

The IRS 3 form can be obtained directly from the IRS website. Here’s a step-by-step process for acquiring the form:

- Visit the IRS official website.

- Use the search function on the homepage and enter "Form 3".

- Download the form in PDF format onto your computer.

It is always recommended to use the official IRS website to ensure the form is the correct version.

Steps to Complete the IRS 3 Form

Completing the IRS 3 form involves several steps, which include detailing trust transactions and gifts. Here’s how to approach it:

-

Identify Reportable Transactions:

- Determine whether you had any transactions with foreign trusts.

- Identify any significant gifts from foreign sources.

-

Gather Required Information:

- Collect information about the foreign trust or the foreign party from which you received gifts.

- Ensure you have the correct valuation of gifts.

-

Complete the Sections of the Form:

- Fill out the general information and any applicable parts related to foreign trust transactions or gifts.

- Double-check for accuracy.

Key Elements of the IRS 3 Form

The form is divided into several important parts:

- Part I: Information on the filer, including identifying data and background on foreign trust connections.

- Part II: Specifics about foreign trusts and transactions.

- Part III: Details on large gifts or bequests from foreign entities.

Each section must be completed with precision to ensure accuracy and avoid submission errors.

IRS Guidelines and Compliance

According to IRS guidelines for 2017, accurate filing of Form 3520 is essential for compliance with U.S. tax regulations. These guidelines elaborate on:

- Documentation: Providing substantiation for foreign transactions and gifts.

- Deadlines: The form is due at the same time as the filer’s income tax return, including extensions.

- Penalties: Late filing or failing to provide accurate information can result in substantial penalties, often calculated as a percentage of the foreign transaction or assets involved.

Filing Deadlines / Important Dates

The IRS mandates that Form 3520 be filed by the same date as your federal income tax return, which is typically April 15th, including any extensions. For 2017, this meant ensuring electronic or paper submissions were postmarked by the due date. Extensions for tax returns also apply to this form, allowing additional time but requiring explicit filing for extensions.

Penalties for Non-Compliance

Non-compliance with the Form 3520 requirements can lead to severe penalties:

- Penalties: Starting at $10,000 or a percentage based on the value of the trust, transaction, or gift involved.

- Increased Scrutiny: Failure to file may result in further IRS investigations or audits.

- Interest: Accumulation of interest on unpaid penalties can add to the financial burden.

Accurate compliance is crucial to avoid these penalties and the resultant impact on personal or business finances.