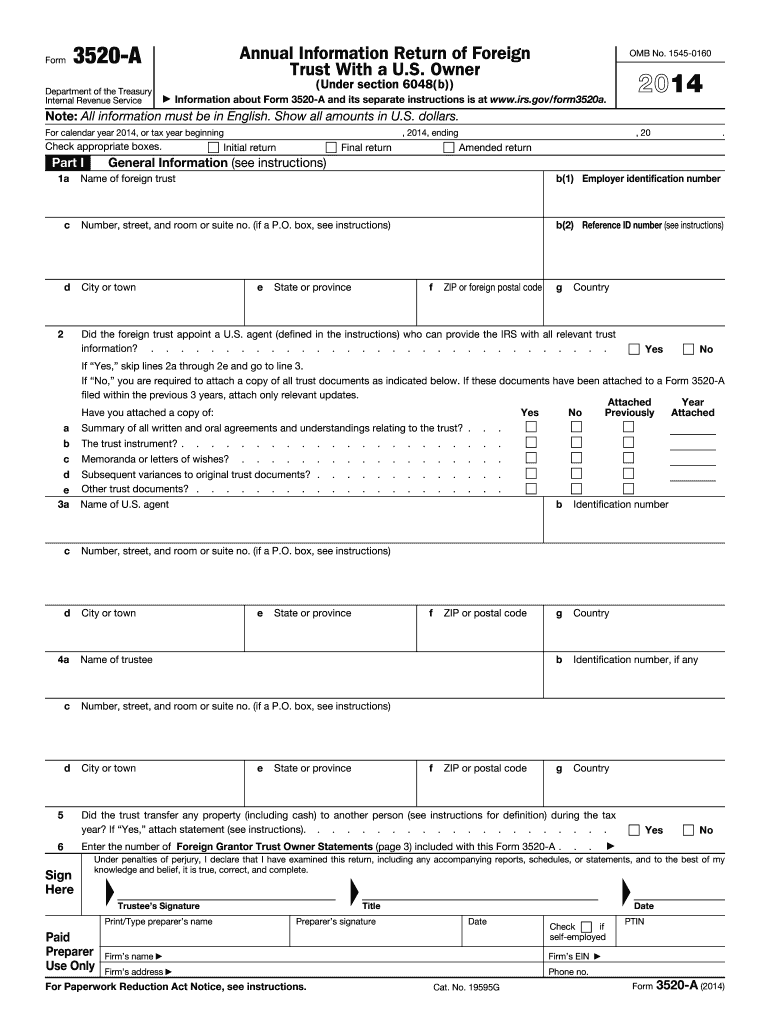

Definition & Meaning of Form 3520-A

Form 3520-A, known as the Annual Information Return of Foreign Trust with a U.S. Owner, is a critical reporting requirement for U.S. persons who own a foreign trust. This form is designed to ensure compliance with U.S. tax regulations regarding foreign assets. It provides detailed information about the operations of the trust, including income, expenses, and changes in ownership. The IRS uses this data to monitor and regulate foreign trusts to prevent tax avoidance and ensure proper tax reporting by U.S. citizens.

Key Elements of Form 3520-A

The form comprises several sections, each serving a distinct purpose in reporting trust activities:

- General Trust Information: Includes basic details about the trust such as name, address, and EIN (Employer Identification Number).

- Income and Expenses Statement: Provides a comprehensive overview of the trust's financial performance, detailing various income sources and types of expenses.

- Balance Sheet: Offers a snapshot of the trust's financial status, listing assets and liabilities at the end of the tax year.

- U.S. Owner Statement: Specifically delineates the share of income, expenses, and credits attributable to U.S. owners.

How to Use Form 3520-A

Completing Form 3520-A accurately is essential for compliance:

- Gather Necessary Information: Begin by collecting all pertinent trust documents, financial statements, and details of beneficiaries and trustees.

- Fill Out General Information: Enter the trust's basic details as well as information about the responsible party.

- Complete Financial Sections: Carefully document all income, expenses, and balance sheet items. Ensure accuracy to avoid discrepancies.

- Owner Statement Details: Allocate income and credits accurately to U.S. owners. Double-check for completeness.

Who Typically Uses Form 3520-A

Form 3520-A is primarily used by:

- U.S. Citizens Owning Foreign Trusts: Individuals with ownership interests in foreign trusts are mandated to file this form.

- Trustees of Foreign Trusts: Trustees are responsible for maintaining and providing necessary documentation to U.S. owners.

- Tax Professionals: Accountants and financial advisors utilize this form to assist clients in meeting U.S. tax obligations.

Steps to Complete Form 3520-A

Accurate completion involves several key steps:

- Prepare Relevant Documents: Ensure all trust-related financial documents are available.

- Understand IRS Guidelines: Familiarize yourself with specific reporting requirements and instructions.

- Input Financial Data: Carefully enter income, deductions, balance sheet items, and U.S. owner information.

- Review and File: Thoroughly review the completed form for accuracy before submitting it to the IRS. Ensure you file by the stated deadline to avoid penalties.

IRS Guidelines for Filing

The IRS specifies several guidelines for the correct completion and filing of Form 3520-A:

- Due Date: Typically, the form is due on the 15th day of the third month after the end of the trust's tax year. Extensions may be granted upon request.

- Penalties for Inaccuracy: Incorrect or late filing can lead to significant penalties. Each failure to comply can result in a fine of five thousand dollars or more.

Required Documents for Form 3520-A

To complete Form 3520-A, you will need:

- Trust Deeds and Agreements: Foundational documents establishing the trust and outlining its terms.

- Financial Statements: Income statement, balance sheet, and previous tax returns.

- Beneficiary and Trustee Information: Includes details of all beneficiaries, trustees, and their respective roles.

- Supporting Documentation: Any relevant attachments that substantiate reported figures.

Penalties for Non-Compliance

Failure to submit Form 3520-A properly can lead to substantial IRS penalties:

- Non-Filing Penalties: Starting at ten thousand dollars for each form not filed or filed late.

- Inadequate Information Penalties: Additional fines may apply if the form lacks sufficient information.

Digital vs. Paper Version

Taxpayers have the option to file Form 3520-A digitally or via paper. The digital option is often preferred for faster submission and confirmation, while the paper version may be necessary for those lacking digital access or requiring a physical document trail.

Software Compatibility

For those filing digitally, ensure compatibility with software platforms. Programs like TurboTax or specific IRS e-file services can expedite submissions and validate input for errors or omissions.

Filing Deadlines and Important Dates

- Annual Submission: March 15 is the standard deadline if operating on a calendar year.

- Extensions: File Form 7004 to request an automatic six-month extension.

Who Issues Form 3520-A

The form is issued by the Internal Revenue Service to track and report foreign trust activities related to U.S. taxpayers.

Conclusion

Understanding and effectively managing the Annual Information Return of Foreign Trust with a U.S. Owner is vital for compliance with U.S. tax laws. Properly completing and submitting Form 3520-A ensures transparency in foreign financial engagements and prevents costly penalties.