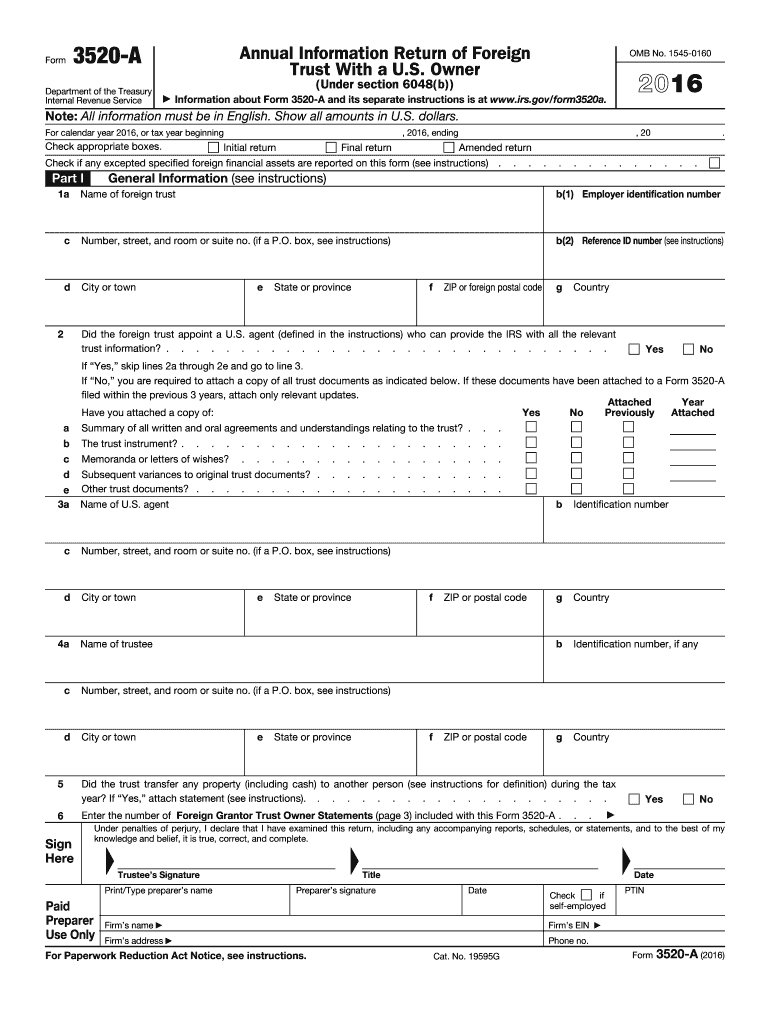

Definition & Meaning

Form 3520, officially known as the "Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts," is an informational document used by U.S. taxpayers. Specifically, the 2016 form 3520 is required for individuals who have engaged in transactions with foreign trusts, have foreign trust ownership, or received gifts from foreign entities totaling more than the IRS threshold for that year. This form ensures compliance with U.S. tax laws governing foreign assets and transactions, aiming to prevent tax evasion by maintaining transparency about offshore financial dealings.

How to Use the 2016 Form 3520

Taxpayers use the 2016 form 3520 to report specific transactions with foreign trusts, ownership of such trusts, and the receipt of substantial foreign gifts. To use this form effectively, you should:

- Identify any foreign trusts you have conducted transactions with during 2016.

- Accurately detail any gifts or bequests from foreign persons or entities, ensuring they meet or exceed the reporting threshold.

- Fill in all required sections of the form, detailing personal information, trust details, and gift information.

Proper use of this form ensures that you remain compliant with IRS regulations while accurately reflecting your financial engagements with foreign entities.

Steps to Complete the 2016 Form 3520

-

Gather Required Information: Collect detailed information about each foreign trust, including the names and addresses of trustees, the value of distributions received, and any foreign gifts.

-

Complete Part I: Enter general information about the filer, including personal identification details and the relationship to the foreign trust.

-

Complete Part II: Provide information about each foreign trust transaction, including transfers, distributions, and the fair market value of assets involved.

-

Complete Part III: Report on the ownership of foreign trusts, specifying details about the trust's financial activities.

-

Complete Part IV: Input data regarding any substantial foreign gifts or inheritances received.

-

Review and Submit: Double-check for accuracy and completeness before filing with your annual tax return. Failure to complete correctly could lead to penalties.

IRS Guidelines

IRS guidelines for form 3520 mandate that U.S. persons report specific transactions involving foreign trusts or substantial gifts from foreign individuals or entities. The guidelines emphasize:

- Full disclosure of all transactions meeting the threshold.

- Precise and accurate reporting to prevent penalties.

- Timely submission to avoid late filing fees.

These guidelines support the IRS's broader objective of ensuring taxpayers provide a clear view of their foreign financial activities.

Filing Deadlines / Important Dates

Typically, the 2016 form 3520 should have been filed with your annual tax return, due on April 15, 2017. For extensions, the IRS provided additional time until October 15, 2017. Missing these deadlines could result in significant penalties, emphasizing the importance of timely submission. Extensions would generally align with those granted for your income tax return.

Penalties for Non-Compliance

Failure to file the 2016 form 3520, or for significant inaccuracies, the IRS imposes penalties, which could include:

- A minimum of $10,000 or a percentage of the gross reportable amount for trusts.

- Additional penalties accruing monthly if issues are not rectified.

Understanding these penalties underscores the necessity of accurate and timely form submission to avoid financial repercussions.

Required Documents

To correctly complete the 2016 form 3520, gather the following documents:

- Statements and records from foreign trusts, detailing transactions and distributions.

- Any documentation of gifts or inheritances from foreign sources.

- Financial records that verify valuations and trust details, ensuring the information provided aligns with IRS expectations.

Having these documents on hand ensures accuracy and compliance with reporting requirements.

Form Submission Methods (Online / Mail / In-Person)

For 2016, form 3520 could be submitted via mail as part of your federal income tax return. While the IRS does not permit electronic filing independently, it could be sent through qualified electronic return originators if included with your digital tax filing. Ensure you choose a method that aligns with your filing preferences and guarantees timely arrival.

Important Terms Related to 2016 Form 3520

Be familiar with several key terms when dealing with this form:

- Foreign Trust: Any trust considered foreign for tax purposes, generally a trust not subject to U.S. jurisdiction.

- Grantor: The entity transferring assets into the trust.

- Beneficiary: An individual entitled to benefits from the trust.

- Gift Threshold: The minimum amount in foreign gifts requiring reporting to the IRS.

Understanding these terms helps clarify the form's requirements and ensures your accurate reporting of foreign financial activities.