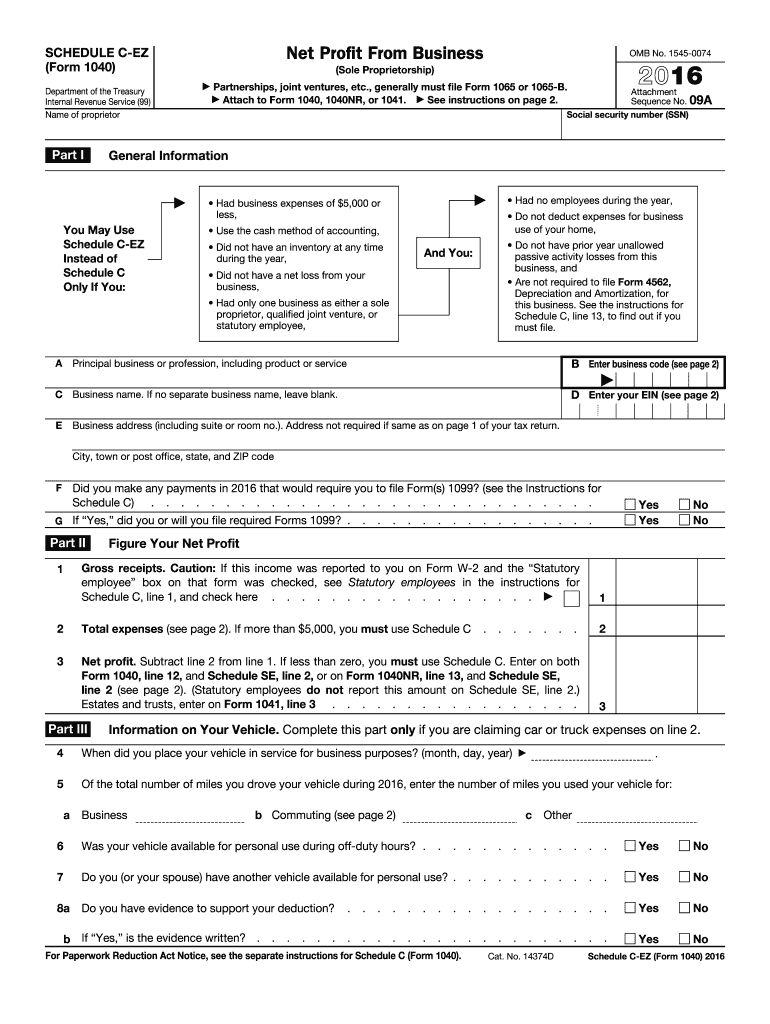

Definition & Purpose of the 1040 Schedule C-EZ Form

The 1040 Schedule C-EZ, a streamlined tax form, is designed for small sole proprietorships or qualified joint ventures to report net profit. It simplifies the process of detailing income and expenses compared to the full Schedule C, making it ideal for businesses with straightforward financials. Businesses without employees and with $5,000 or less in business expenses are typically eligible to use this form. It provides a simple way to calculate business profit, focusing on major areas such as gross receipts and total expenses.

Eligibility Criteria for Using Schedule C-EZ

Not all businesses are eligible to use the Schedule C-EZ form. Key eligibility criteria include:

- No employees within the business.

- Total business expenses must be $5,000 or less for the tax year.

- No need to claim a home office deduction or account for depreciation.

- The business must not have a net loss.

- A cash accounting method is used by the business.

Meeting these criteria allows small business owners to leverage this form, saving time and simplifying their tax filing process.

Steps to Complete the 1040 Schedule C-EZ Form

Completing the Schedule C-EZ involves several steps:

- Gross Income Reporting: Record total revenues from business activities.

- Expense Calculation: Sum up allowable business expenses.

- Vehicle Information: If applicable, fill out mileage and vehicle-related expense details.

- Net Profit Calculation: Subtract total expenses from gross receipts to determine net profit.

- Transfer to Form 1040: Enter the net profit on the appropriate line of the Form 1040 (U.S. Individual Income Tax Return).

Ensuring accuracy in these steps is crucial to reflect your business's true financial position and minimize discrepancies during IRS reviews.

Key Elements of the Schedule C-EZ Form

The Schedule C-EZ consists of several critical sections:

- Part I: General Information: Basic business details including the principal business or profession and business name.

- Part II: Figure Your Net Profit: This section requires input for gross receipts, total expenses, and resulting net profit.

- Part III: Information on Your Vehicle: Necessary if claiming vehicle expenses.

Each section of the form is designed to capture concise, relevant business information, ensuring clarity and simplicity.

Important Terms Related to Schedule C-EZ

Familiarity with important terms helps in navigating the Schedule C-EZ:

- Sole Proprietorship: A business structure where one individual owns the business and is personally liable.

- Gross Receipts: Total revenue from business transactions before any deductions.

- Net Profit: The remaining income after subtracting all allowable business expenses from gross receipts.

- Qualified Joint Venture: A sole proprietorship run by a married couple filing jointly.

Understanding these terms ensures better accuracy in completing and filing the form.

IRS Guidelines on Schedule C-EZ Usage

According to IRS guidelines, Schedule C-EZ can be used by those meeting specific criteria and preferring a simplified reporting method:

- Businesses should ensure the use of cash accounting.

- Carefully follow IRS instructions for accurately reporting business and vehicle expenses.

- Use the form only if conditions align with IRS rules to avoid complications or penalties.

IRS guidelines underline the importance of adherence to filing rules, protecting businesses against audits or penalties.

Filing Deadlines & Important Dates

Being aware of filing deadlines is crucial for compliance:

- Annual Filing: Aligns with the personal tax return deadline, usually April 15.

- Extensions: Filing Form 4868 provides an automatic six-month extension, moving the deadline to October 15.

Timely submission ensures businesses avoid late fees and interest on unpaid taxes.

Penalties for Non-Compliance

Failure to comply with IRS regulations regarding Schedule C-EZ can result in penalties:

- Late Filing Penalty: Up to 5% of the unpaid taxes for each month or part of a month that a return is late, capped at 25%.

- Inaccuracy Penalty: A penalty of 20% on underpaid taxes due to negligence or disregard of IRS rules.

Understanding the implications of these penalties emphasizes the importance of accurate and timely filings.