Definition and Purpose of Schedule C-EZ

Schedule C-EZ (Form 1040) was designed as a simplified version of Schedule C for sole proprietors to report net profits from a business. This form enables those with uncomplicated tax situations to file without the extensive details required by the regular Schedule C. Its primary use is to streamline the filing process for small business owners who meet specific conditions, such as having limited business expenses and not carrying any inventory. By using Schedule C-EZ, eligible taxpayers can save time and reduce the paperwork involved in tax preparation.

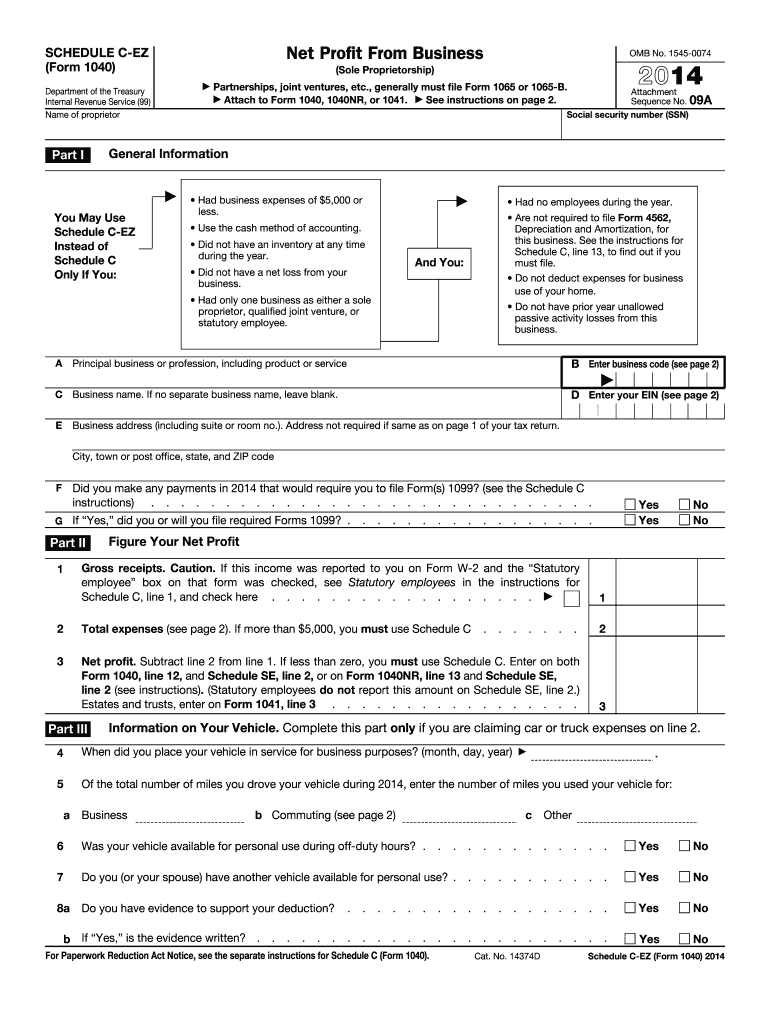

Eligibility Criteria for Using Schedule C-EZ

Eligibility to use Schedule C-EZ requires meeting several specific conditions. First, your business expenses should not exceed $5,000. Additionally, you should not have any employees, nor should you own or lease any property associated with the business. The form is not applicable if you are operating your business as a corporation or partnership. Importantly, you must use the cash method of accounting, and your total business inventory should be zero. Understanding these criteria is crucial for determining if Schedule C-EZ is suitable for your filing needs.

Common Eligibility Scenarios

- Sole proprietors without employees.

- Businesses operating without inventory.

- Taxpayers using cash accounting methods.

- Business entities without significant expenses.

Key Elements of Schedule C-EZ

Schedule C-EZ focuses on key elements essential for reporting net profit efficiently. Among these are gross receipts or sales, total business expenses, and vehicle information for those who use vehicles for business purposes. The form also considers business mileage and other travel costs when applicable. This concise structure ensures that all necessary fiscal information regarding small business operations is documented without complicating the filing process.

Required Information

- Total gross receipts.

- Business expenses totaling under $5,000.

- Vehicle mileage if applicable.

Vehicle Usage Reporting

If you used a vehicle for your business, you must report mileage on Schedule C-EZ. Ensure accurate records of total miles driven for business purposes throughout the year as this impacts the deductions you can claim.

Steps to Complete Schedule C-EZ

Filing Schedule C-EZ is a straightforward process, especially if you fulfill the eligibility criteria. The steps are methodically organized to streamline the process.

- Gather Necessary Information: Collect details regarding gross receipts, total expenses, and any applicable vehicle information.

- Fill Out Personal Information: Complete the top section with your name, Social Security number, and business name.

- Report Income and Expenses: Accurately note your income and allowable expenses. Ensure they align with the eligibility requirements.

- Sign and Date: Confirm and authenticate your form by providing your signature and dating it appropriately.

Tips for Accurate Filing

- Double-check the eligibility before filling out the form.

- Keep receipts and documentation to substantiate figures.

- Review for consistency with your tax return to avoid discrepancies.

Who Typically Uses Schedule C-EZ

Schedule C-EZ is primarily used by small business owners who maintain straightforward operations. Sole proprietors with minimal expenses, freelancing individuals, and certain independent contractors find this form advantageous for its simplicity and ease of use.

Example Scenarios

- Freelance graphic designers operating without employees.

- Independent consultants with limited travel and business costs.

- Home-based sellers with less than $5,000 in yearly expenses.

Important Terms Related to Schedule C-EZ

Familiarity with terminology specific to Schedule C-EZ ensures accurate completion and reporting. Critical terms include gross receipts, net earnings, business mileage, and cash method accounting. An understanding of these terms helps in determining eligibility and accurate tax reporting.

Key Terms Explained

- Gross Receipts: Total income from sales before expenses.

- Net Earnings: Income after subtracting all business expenses.

- Cash Method of Accounting: Recording income and expenses as they are actually received or paid.

- Business Expenses: Costs necessary to keep your business operational.

IRS Guidelines for Schedule C-EZ

The IRS provides comprehensive guidelines for completing Schedule C-EZ to ensure accuracy and compliance. These guidelines underscore the requirements for eligibility and specific instructions for each section of the form. Adhering to IRS instructions is fundamental to avoid errors or potential audits.

Critical IRS Requirements

- Maintain accurate and detailed records.

- File within designated deadlines.

- Understand the distinction between personal and business expenses.

Filing Deadlines and Important Dates

Adhering to the filing deadline for Schedule C-EZ is crucial to avoid any penalties. Typically, this form is due with your Form 1040 by April 15, unless an extension is filed. Ensure that all related documents are complete and submitted to the IRS within the stipulated timeframe.

Extension and Late Filing

Should you require additional time, filing an extension provides the flexibility to extend your deadline to October 15. Remember, the extension allows for more time to file the paperwork, not to pay any taxes due.

Penalties for Non-Compliance

Failure to comply with the requirements for filing Schedule C-EZ can lead to penalties. These may include late filing fees or penalties for underreporting income. The IRS enforces strict guidelines, so accuracy and timeliness are paramount.

Avoiding Penalties

- Ensure comprehensive understanding of form requirements.

- Keep documentation organized for verification.

- File promptly within IRS deadlines.

By understanding the essentials of the 2014 Schedule C-EZ and following these detailed guidelines, taxpayers can navigate the tax filing process effectively, ensuring compliance and optimizing their tax situation.