Definition and Meaning

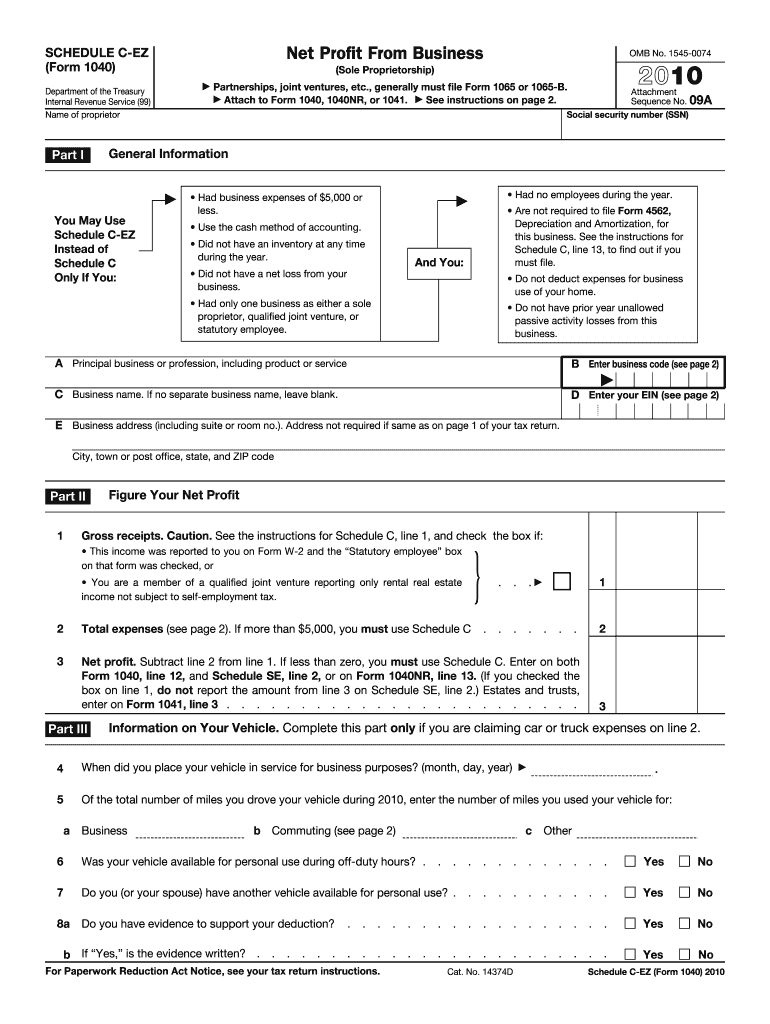

The 2010 Schedule C-EZ form is a simplified version of the Schedule C, used by sole proprietors to report their net profit from business activities. This form is applicable for taxpayers who meet certain criteria, such as having business expenses not exceeding $5,000, no employees, and not claiming depreciation or a home office deduction. By streamlining the reporting process, the Schedule C-EZ allows eligible business owners to fulfill their tax obligations with reduced paperwork.

Eligibility Criteria

To use the 2010 Schedule C-EZ form, a taxpayer must satisfy specific requirements. Key eligibility criteria include:

- Business expenses must be $5,000 or less.

- The business should have no employees or inventory.

- The taxpayer cannot claim deductions for a home office, depreciation, or amortization.

- The business must be a sole proprietorship.

- The taxpayer must not have previously claimed the retirement contribution credit based on self-employment income. These conditions ensure that the form is intended for very simple business scenarios, focusing on those with straightforward financial activities.

How to Obtain the 2010 Schedule C-EZ Form

Taxpayers can obtain the 2010 Schedule C-EZ form from various sources. It is available on the Internal Revenue Service (IRS) website for download in PDF format. Alternatively, physical copies can be requested from the IRS through the mail. Additionally, tax preparation software often provides access to this form within their digital tools, and tax professionals can supply the form as part of their services.

Steps to Complete the 2010 Schedule C-EZ Form

Completing the 2010 Schedule C-EZ involves several steps to ensure accuracy:

- Begin by entering the gross receipts or sales of the business activities on line one.

- Deduct the total expenses that do not exceed the $5,000 limit.

- Report net profit on line three by subtracting expenses from gross receipts.

- Include any vehicle information on line four if applicable, such as business mileage deduction.

- Use additional lines to indicate any other relevant financial information related to business activities. Accuracy in each entry ensures compliance with IRS requirements and reduces the risk of errors or audits.

Key Elements of the 2010 Schedule C-EZ Form

The form consists of specific elements critical to reporting and calculating business income, such as:

- Gross Receipts: Total revenue from business performed.

- Total Expenses: All costly business engagements, capped at $5,000.

- Net Profit Calculation: Gross receipts minus total expenses.

- Vehicle Expenses: Details on usage and deductions related to business travel. This straightforward structure aids in capturing the necessary financial data efficiently, helping taxpayers comply with their tax reporting duties.

IRS Guidelines

The IRS provides detailed guidelines on completing the Schedule C-EZ form, which are crucial for compliance:

- Follow instructions on each line carefully to ensure accurate reporting.

- Declare all business income, including any received in goods or services.

- Maintain records to substantiate all reported figures; this includes keeping receipts and financial statements for at least three years. The guidelines help prevent errors and ensure sole proprietors meet all federal compliance requirements.

Important Terms Related to 2010 Schedule C-EZ Form

- Sole Proprietorship: A business owned and operated by one individual, with no legal distinction between the owner and the entity.

- Gross Receipts: Total income earned before any deductions.

- Net Profit: Income that remains after deducting all allowable expenses.

- Depreciation: The reduction in value of business assets over time, not applicable in this form. Understanding these terms is vital for accurately completing and filing the form.

Filing Deadlines and Important Dates

For taxpayers using the 2010 Schedule C-EZ, adhering to deadlines is crucial:

- The form must accompany the taxpayer’s annual income tax return, typically due on April 15. If this date falls on a weekend or holiday, the deadline may be extended.

- It is possible to apply for an automatic extension using Form 4868. Meeting deadlines ensures that taxpayers avoid penalties and remain in good standing with the IRS.