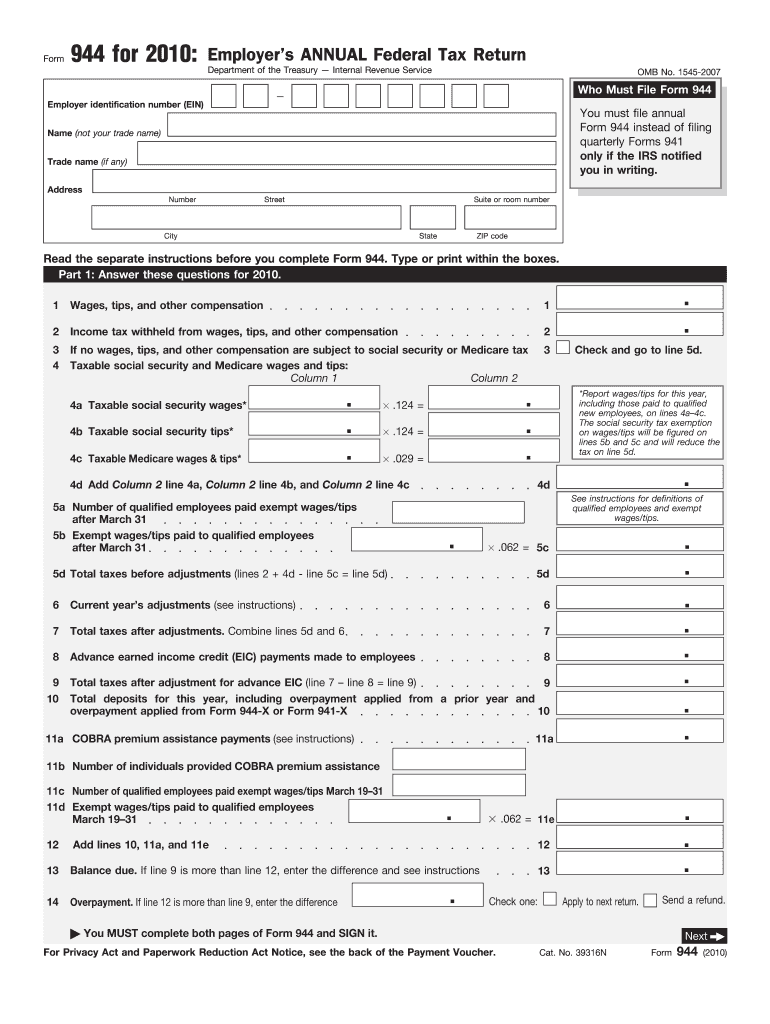

Definition and Purpose of the 2010 Form 944

The 2010 Form 944, officially titled the Employer’s Annual Federal Tax Return, is a form used by certain small employers to report wages, tips, other compensation, and taxes withheld to the Internal Revenue Service (IRS). This form is specifically designed for employers whose liability for social security, Medicare, and withheld federal income taxes is $1,000 or less per year. Instead of filing quarterly, qualified employers can file this form annually, reducing the frequency of reporting. Understanding its purpose helps employers know whether they qualify and how it can streamline their tax reporting.

How to Use the 2010 Form 944

The 2010 Form 944 is utilized for reporting annual employment taxes. Employers should calculate total wages paid and tips reported, determine the total social security and Medicare taxes due, and report any advanced earned income credit payments made to employees. The form also requires the reporting of federal income tax withheld and any adjustments for sick pay, group-term life insurance, or other types of adjustments. Employers must ensure they meet the criteria for filing this form, which is often communicated directly by the IRS.

Steps to Complete the 2010 Form 944

- Gather Required Information: Include total employee wages, tips, and other compensation.

- Calculate Taxes: Compute social security and Medicare taxes, ensuring accuracy in the deductions.

- Adjustments and Credits: Enter adjustments for any corrections, such as over-collected taxes, and report any tax credits.

- Review: Double-check all figures and ensure all calculations reflect the company's payroll accurately.

- Sign and Date: The form must be signed and dated by an authorized person within the business.

- Submit: Choose a preferred method of submitting the completed form – via mail or online.

Filing Deadlines and Important Dates for the 2010 Form 944

The 2010 Form 944 was due by January 31, 2011. Employers needing to pay taxes alongside the form submission could do so up until February 10, 2011, if all taxes due were deposited timely, throughout the year. It's crucial to adhere to these deadlines to avoid any penalties or interest on late payments.

Who Typically Uses the 2010 Form 944

Small businesses that have been notified by the IRS directly are the primary users of the 2010 Form 944. These businesses typically have a lower total tax liability and can benefit from the reduced frequency of annual filings compared to the quarterly requirement of other forms. This includes certain individual entrepreneurs, small-scale retailers, and service providers.

Key Elements of the 2010 Form 944

- Wage and Tax Reporting: Centralized in a single section, detailing all compensation types.

- Tax Calculation: Specific rows outline the method for computing social security and Medicare taxes.

- Adjustments and Credits Section: Allows modifications for accuracy in the reported amounts.

- Signature Line: Ensures the form is legally executed by an authorized representative of the business.

IRS Guidelines for the 2010 Form 944

The IRS provides detailed instructions for completing the form, necessitating careful review to ensure compliance. This includes guidelines on calculating taxes, making adjustments, and identifying who must or should not file the form. These guidelines help in minimizing errors and avoiding potential penalties.

Penalties for Non-Compliance

Failing to file the 2010 Form 944 on time or inaccurately reporting tax information can lead to significant penalties. These may include fines for late filing and interest charges on unpaid taxes. Correctly filing and on-time submissions can prevent such costly consequences, emphasizing the importance of adherence to IRS requirements.