Definition and Purpose of the 2014 Form 944

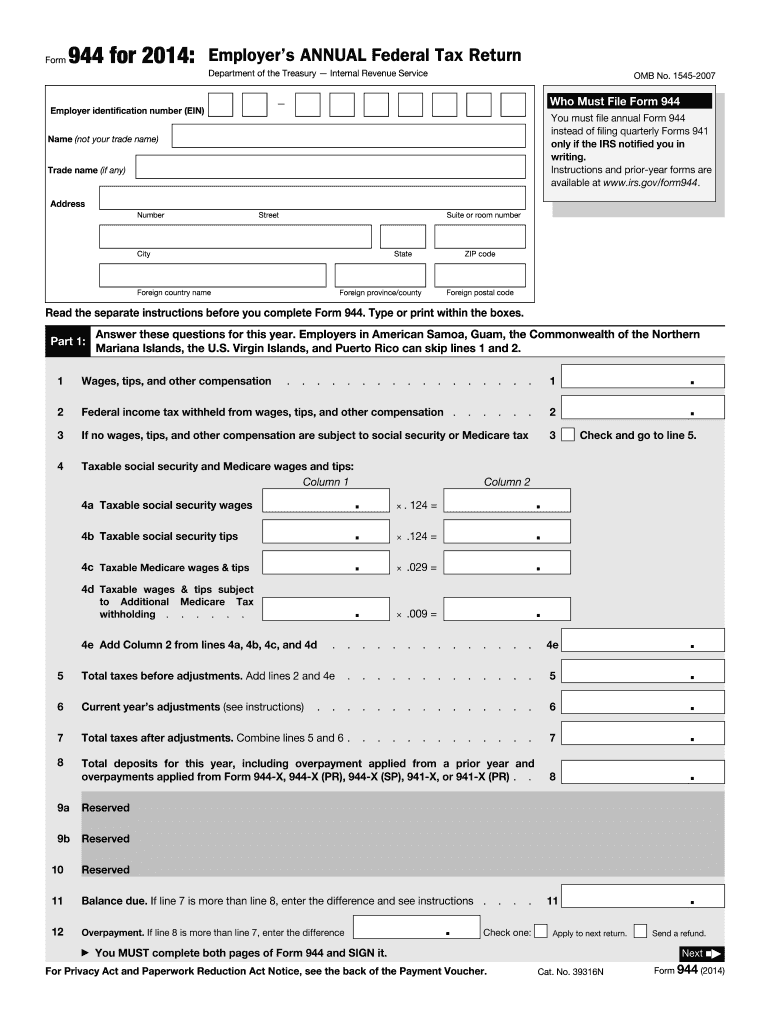

The 2014 Form 944, officially known as the Employer's Annual Federal Tax Return, is a form required by the Internal Revenue Service (IRS) in the United States. It is designed for small employers to report annual payroll taxes. The primary purpose of this form is to report wages, tips, other compensation, and the federal income tax that has been withheld. This form is specifically intended for those employers whose annual payroll tax liability is $1,000 or less.

Steps to Complete the 2014 Form 944

-

Gather Necessary Information: Before you start filling out the form, make sure to have all required documents, including employee payroll information, Federal Employer Identification Number (FEIN), and details of federal income tax withheld.

-

Enter Business Identification Details: Include the legal name of your business, trade name, and FEIN in the top sections of the form to ensure correct identification.

-

Report Payroll and Tax Withholding: Record the total wages paid, federal income tax withheld, and taxable social security and Medicare wages in their respective sections.

-

Calculate Tax Liabilities: Use the specified instructions to calculate the payroll tax liability for social security, Medicare, and additional Medicare tax, ensuring all figures are accurate.

-

Include Any Deposits or Credits: Report any payments made throughout the year or applied credits. This includes overpayments from previous tax years.

-

Review and Sign the Form: Double-check all information for accuracy. The employer or an authorized representative should sign and date the form for submission.

Eligibility Criteria for Using 2014 Form 944

Not all employers are eligible to use Form 944. It is primarily targeted at small employers whose total annual liability for social security, Medicare, and withheld federal income taxes is $1,000 or less. Employers must receive a notification from the IRS that permits them to file Form 944 instead of Form 941.

Filing Deadlines and Penalties

Employers need to submit the 2014 Form 944 by January 31, 2015. This deadline can be moved to February 10 if you deposited all taxes when due. Late filing can result in penalties and interest charges. The penalty is generally a certain percentage of the unpaid taxes.

Form Submission Methods

There are multiple ways to submit the 2014 Form 944:

- Electronic Filing: Utilize the IRS' e-file system which is a secure, fast, and error-proof method.

- Mail: Send the completed form to the address specified in the IRS instructions.

- Authorized Service Providers: Some payroll service providers can file the form on your behalf.

Benefits of Filing Form 944 for Small Employers

For eligible small employers, Form 944 helps simplify tax filing by reducing the frequency of submitting payroll tax forms. Instead of quarterly filings required by Form 941, Form 944 requires only an annual submission. This reduces administrative workload and helps employers manage time and resources more efficiently.

Common Errors When Completing the 2014 Form 944

To avoid processing delays:

- Ensure all financial entries correspond to payroll records and W-2 forms.

- Verify your FEIN, as errors could result in misdirected correspondence.

- Double-check all calculations, especially payroll tax liabilities.

- Make sure the deposited amounts and credits are accurately reported.

IRS Guidelines for Form 944

The IRS provides comprehensive instructions for completing and submitting Form 944. Key points to remember include who can file, how to handle corrections, and the methods for submitting payments. These guidelines are critical for legal compliance and for avoiding penalties.

Key Elements of the 2014 Form 944

- Employer Information: Essential contact and identification details.

- Employee Compensation: Total wages and withholding details.

- Tax Liabilities: Social security, Medicare, and federal tax specifics.

- Deposits and Credits: Any previous payments or transferred credits applied to the current tax liability.

- Authorized Signature: Legal confirmation of the accuracy and completeness of the form.

Comparison of Digital vs. Paper Versions

Employers can choose between completing Form 944 digitally or on paper. Digital filing through the IRS e-file system offers immediate confirmation and faster processing. Conversely, paper submissions may incur delays, though they remain an option for those without electronic access.

Penalties for Non-Compliance

Failing to file Form 944 on time or incorrectly reporting information can lead to financial penalties. Non-compliance can also attract interest charges until the full tax liability is settled. Employers should make every effort to meet deadlines to avoid these repercussions.

State Specific Considerations

While Form 944 is a federal requirement, employers should also be aware of state-specific payroll tax obligations. These can vary and might require additional filings or adjustments based on local regulations. Consulting with a tax professional familiar with both federal and state laws can provide guidance tailored to specific business needs.

Real-World Scenarios Involving Form 944

Small businesses like a local boutique with a limited payroll might find the annual filing of Form 944 to be advantageous due to simplified processes. However, a growing company should remain alert to when their tax liability exceeds thresholds, requiring a transition to filing Form 941 quarterly.