Understanding the 2009 Form 944

The 2009 Form 944 is an IRS document that allows small employers to report their annual federal tax liabilities. Typically utilized by businesses with an employment tax liability of $1,000 or less, this form consolidates reporting responsibilities into one annual return instead of quarterly submissions, providing administrative convenience. It helps employers report wages, federal income taxes withheld, and Social Security and Medicare taxes.

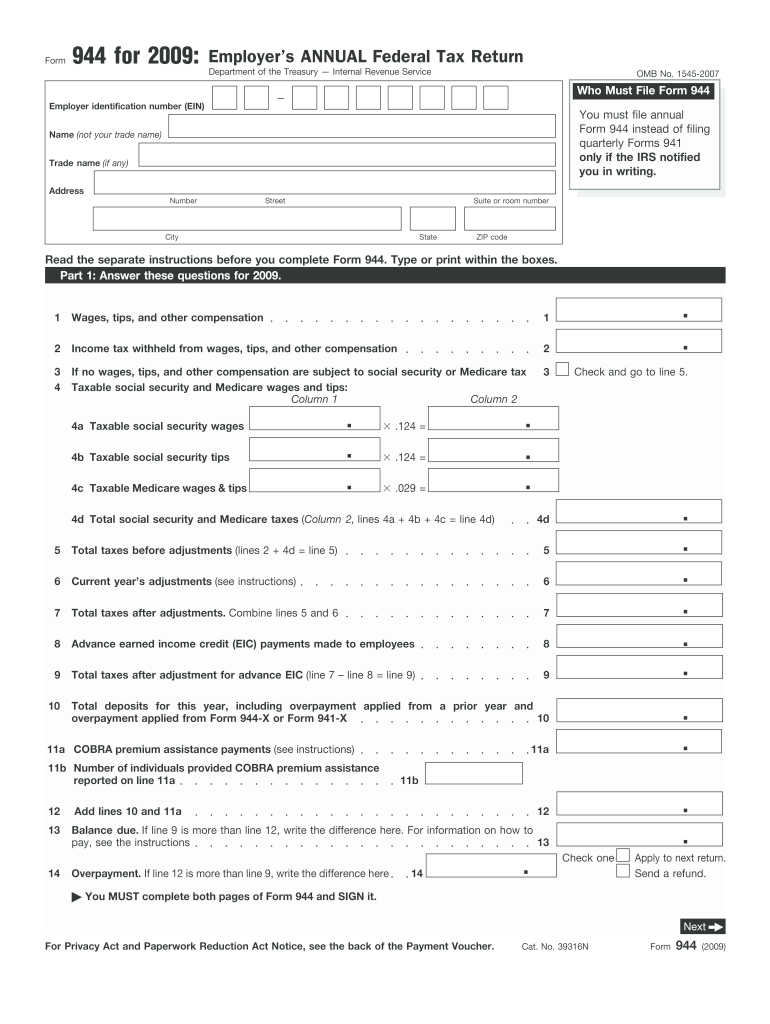

Key Elements of the 2009 Form 944

Include the following components when completing the 2009 Form 944:

- Employer Details: Business name, address, and Employer Identification Number (EIN).

- Tax Liability Sections: Lines to report wages paid, federal income taxes withheld, and Social Security and Medicare taxes.

- Adjustments and Credits: Spaces for reporting previous overpayments or penalties, with instructions for claiming credits.

- Signature and Certification: Confirmation that the information provided is accurate to the best of the employer’s knowledge.

Completing the 2009 Form 944

Follow these steps to complete the form accurately:

- Gather Necessary Documents: Collect payroll records, prior year tax filings, and documentation for any tax credits or adjustments.

- Fill in Employer Information: Ensure accuracy in the business name, address, and EIN.

- Enter Wages and Taxes: Report wages subject to federal income taxes and withheld amounts accurately using payroll data.

- Complete Adjustments Section: Address any adjustments due to overpayments or tax credits available.

- Sign and Date: Ensure the form is signed by a responsible party within the organization.

How to Obtain the 2009 Form 944

The 2009 Form 944 is available through several channels:

- IRS Website: Download a printable PDF directly from the official IRS site.

- Physical Copies: Request a mailed copy from the IRS, although this may take additional processing time.

- Tax Software Programs: Many platforms like TurboTax or QuickBooks provide integrated access to IRS forms.

Usage Scenarios for the 2009 Form 944

Smaller entities benefit from the 2009 Form 944’s streamlined approach. Businesses with minimal employment tax liabilities can reduce paperwork by filing annually. Here’s who commonly uses it:

- Small Employers: Businesses with a small workforce and limited payroll, such as family-owned shops.

- New Enterprises: Recent startups that have not yet grown large enough to exceed the $1,000 liability threshold.

IRS Guidelines and Compliance

Abiding by IRS instructions is critical:

- Adherence to Instructions: Follow the IRS guidelines precisely, especially regarding rounding figures and reporting tips.

- Record Keeping: Maintain records to support calculations on the form for at least four years.

Penalties for Non-Compliance

Non-compliance can lead to financial repercussions:

- Late Filing Penalties: Fines for failing to file by the specified deadline.

- Accuracy-Related Penalties: Consequences for incorrect or fraudulent reporting.

Filing Deadlines and Important Dates

Understanding key deadlines ensures compliance:

- Annual Submission: The form must be filed by January 31 of the following year. Adjust your internal timelines to ensure timely submission, including time for any corrections.

- Quarterly Deposit Schedule: Despite annual filing, employers must adhere to the quarterly deposit of federal taxes collected.

Versions and Alternatives to Form 944

While essential for some, there are alternatives:

- Form 941: Used by employers who surpass the $1,000 tax limit, requiring quarterly filings.

- Electronic Submissions: Consider digitally filing through IRS-supported tax software for faster processing and confirmation.

By following these guidelines and understanding the nuances of the 2009 Form 944, employers can streamline their annual tax responsibilities while ensuring compliance with IRS regulations.