Definition & Meaning

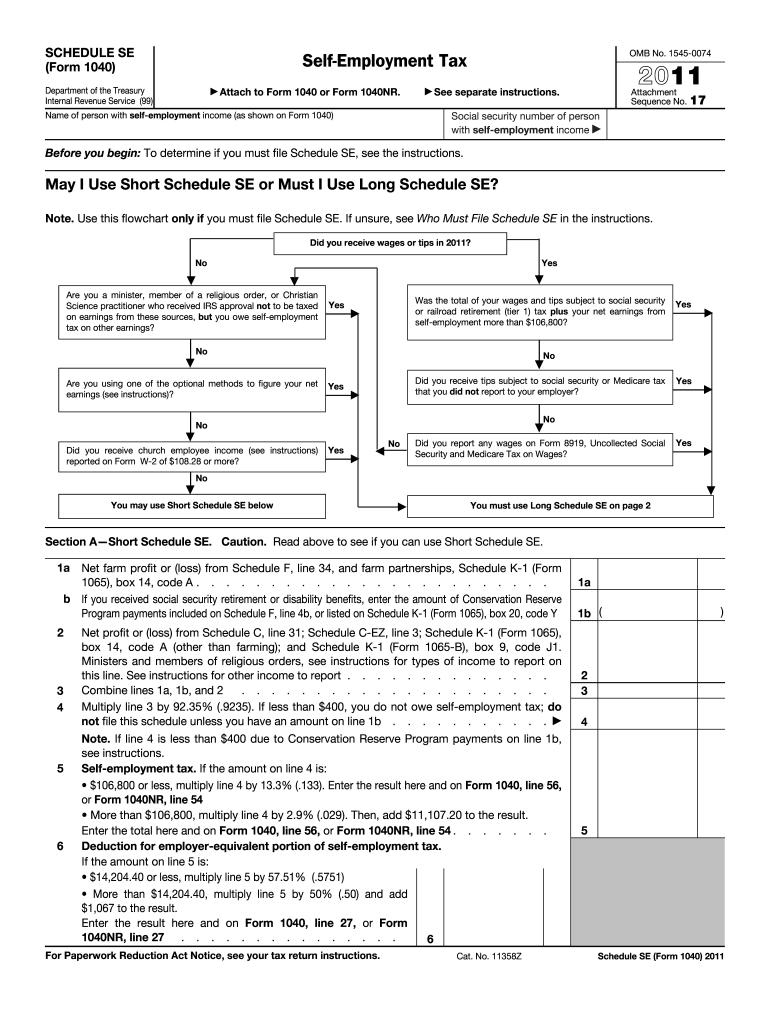

The Schedule SE (Form 1040) is a tax document utilized by individuals reporting self-employment income. It is specifically used to calculate self-employment tax, which encompasses Social Security and Medicare taxes for individuals who work for themselves. Unlike conventional employment taxes that an employer withholds, self-employed individuals must calculate and pay these taxes independently. This form outlines how to determine the net earnings from self-employment and calculate the appropriate taxes owed. The 2011 edition continues this function, aligning with tax laws applicable at the time.

How to Use the 2011 Schedule SE Form

Using the 2011 Schedule SE form requires a clear understanding of your self-employment income and any applicable deductions. Typically, this involves:

- Gathering Income Information: Include all earnings from self-employment, including income from business activities, contracted work, or freelance projects.

- Calculating Net Earnings: Deduct allowable expenses related to generating this income. These expenses can include office supplies, travel costs, and professional services fees.

- Completing Both Parts of the Form: Schedule SE is divided into two parts depending on income levels. Part I is for individuals with less than $106,800 in net earnings. Part II is for those above this threshold. However, you're required to fill out Part I in most cases.

Steps to Complete the 2011 Schedule SE Form

Completing the 2011 Schedule SE form involves several steps:

-

Part I: Net Earnings Calculation:

- Enter your net profit or loss from Schedule C, C-EZ or from partnership income.

- Calculate net earnings by multiplying the total by 92.35% (0.9235).

-

Part II: Self-Employment Tax Calculation:

- Apply the appropriate tax rate to your net earnings. For 2011, the rate is 13.3% of net earnings.

- Record any necessary deductions, including a credit for one-half of the self-employment tax.

-

Filing: Transfer the calculated amounts to the appropriate line on Form 1040 and ensure both Schedule SE and Form 1040 are submitted together.

Important Terms Related to 2011 Schedule SE Form

Understanding key terms is crucial:

- Net Earnings: The amount of income subject to self-employment taxes after deducting business expenses.

- Self-Employment Tax: The combined tax for Social Security and Medicare, applicable to self-employed individuals, replacing the payroll tax withheld by employers.

- Social Security Wage Base: The maximum income level subject to Social Security tax each year, which in 2011 was $106,800.

Filing Deadlines / Important Dates

For taxes calculated on the 2011 Schedule SE, the deadline for submission typically aligns with the individual income tax filing date in the U.S., which is April 15, unless it falls on a weekend or holiday. If an extension is filed, the deadline may be extended, but taxes owed should still be paid by the original deadline to avoid penalties.

IRS Guidelines

The Internal Revenue Service (IRS) provides guidelines to ensure correct filing:

- Eligibility: Instructions on who should file based on income and business structure.

- Documentation: Guidance on required supporting documents, such as receipts and income statements, to substantiate claims on the Schedule SE form.

- Penalties: The IRS outlines penalties for underpayment or failure to file, emphasizing timely and accurate filing.

Software Compatibility

Several software programs support the completion of the Schedule SE form:

- TurboTax and QuickBooks: Both offer integrated tools to guide users through self-employment tax calculations and form filing.

- Online Platforms: Many provide step-by-step assistance, allowing users to import data directly from accounting software or financial records.

Taxpayer Scenarios for the 2011 Schedule SE Form

The 2011 Schedule SE form is relevant for various self-employment scenarios:

- Freelancers and Independent Contractors: Individuals working on diverse projects without an employer may need to file this form.

- Small Business Owners: Sole proprietors and partners who report personal income and expenses from their businesses fall into this category.

- Gig Economy Participants: Those earning from short-term or task-based jobs, such as ridesharing or delivery services, need to report this income.

Penalties for Non-Compliance

Failure to correctly file the 2011 Schedule SE form may result in:

- Late Payment Penalties: If taxes are not paid by the original deadline, penalties and interest may accrue.

- Failure-to-File Penalties: These increase each month or part of a month that a tax return is late, up to a maximum percentage of the tax due.

Required Documents

To complete the 2011 Schedule SE form, gather:

- Income Records: 1099-NEC, W-2, and other documentation showing income earned.

- Expense Receipts and Documentation: For deductible business expenses.

- Previous Year's Tax Return: For reference on past deductions and calculations.

Form Submission Methods

Submitting the form can be done via:

- Electronic Filing: Preferred for faster processing and confirmation of receipt.

- Manual Mailing: Sending a hard copy of the form to the appropriate IRS location, as indicated in the form instructions.