Definition & Meaning

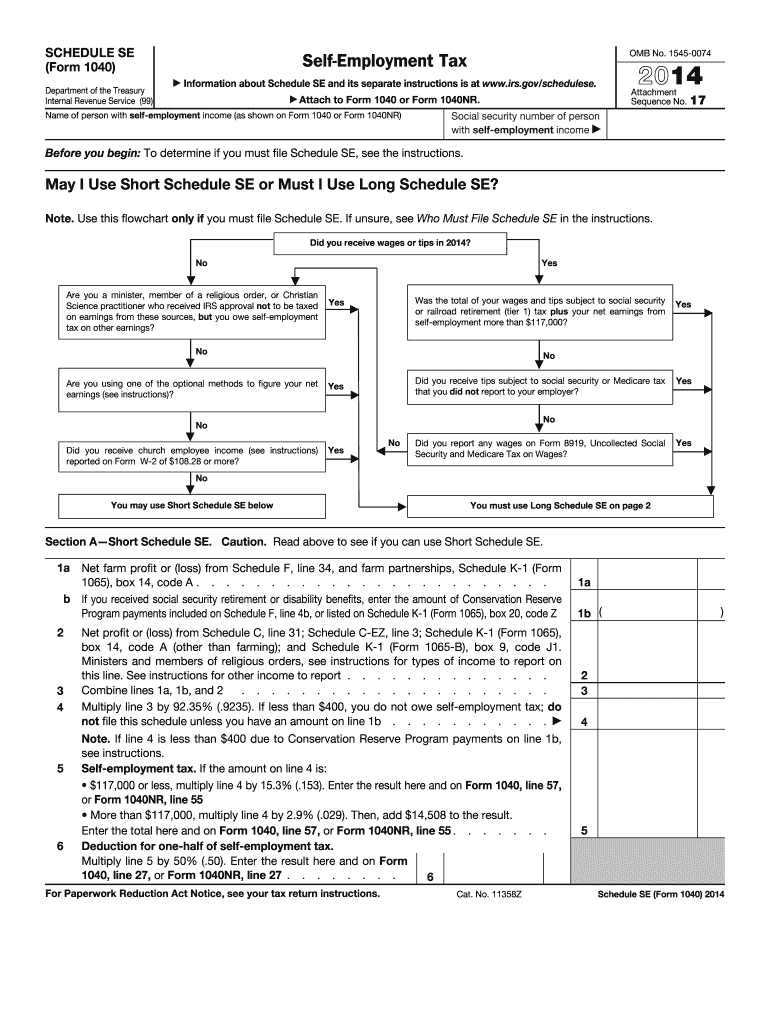

The Schedule SE (Form 1040) for 2014 is a vital tax document used by self-employed individuals to calculate their self-employment tax. This form helps taxpayers determine how much tax they owe based on their net earnings from self-employment. The document applies to anyone operating as a sole proprietor, independent contractor, or member of a partnership, focusing on self-employed individuals' contributions towards Social Security and Medicare taxes.

How to Use the 2014 Schedule SE Form

To use the Schedule SE (Form 1040) effectively, individuals should follow these critical steps:

- Collect Income Records: Gather all income records from self-employment activities, including contracts and invoices.

- Determine Net Earnings: Calculate your net earnings from self-employment by subtracting business expenses from gross income.

- Complete the Short or Long Form: The form provides a short and long version, depending on your net earnings. The long form is necessary if your income is above a specific threshold or you need to apply specific circumstances like farm income.

- Calculate Tax: Compute the self-employment tax by applying the appropriate tax rates to your net earnings.

Steps to Complete the 2014 Schedule SE Form

Filling out the Schedule SE involves a series of detailed steps:

- Start with Personal Information: Enter your name, address, and Social Security Number at the top of the form.

- Assess Total Income: Document your total income from self-employment.

- Evaluate Deductions: Identify and indicate any deductions you can claim that reduce your taxable income.

- Choose Form Version: Decide between the short and long form based on your income level and additional requirements.

- Complete Calculations: Use the instructions to perform calculations for self-employment tax.

- Transfer Tax Amount: Transfer the calculated tax amounts to your primary Form 1040.

Important Terms Related to 2014 Schedule SE Form

Understanding these essential terms will aid in navigating and completing this form:

- Self-Employment Tax: This consists of Social Security and Medicare taxes primarily for individuals who work for themselves.

- Net Earnings: The income from self-employment minus business expenses.

- Social Security: A federal program that provides retirement and disability benefits.

- Medicare: A health insurance program for those aged 65 and older or with specific disabilities.

Legal Use of the 2014 Schedule SE Form

The legal use of the 2014 Schedule SE requires compliance with IRS regulations to ensure correct reporting of self-employment income for tax purposes. This form is binding once filed, and inaccuracies can lead to audits or penalties. It is crucial to retain records in case of verification by tax authorities and to ensure that all computations and entries align with the guidelines provided by the IRS.

IRS Guidelines

The IRS provides comprehensive instructions alongside the Schedule SE (Form 1040), guiding taxpayers on eligibility, calculations, and error avoidance:

- Eligibility: Defines who must file based on income and self-employment status.

- Instructions: Detail each step for accurate completion.

- Examples: Include hypothetical scenarios to clarify common situations.

- Warnings: Highlight potential pitfalls and errors during form completion.

Filing Deadlines / Important Dates

Filing the Schedule SE (Form 1040) by the deadline is mandatory to avoid penalties:

- Annual Due Date: Typically, April 15th of the following year unless it falls on a holiday or weekend, which then extends to the next business day.

- Estimated Payments: For those with significant self-employment tax, quarterly estimated taxes may be required.

Penalties for Non-Compliance

Non-compliance with filing requirements for the Schedule SE can lead to several consequences:

- Monetary Fines: Include fines for late payment and underreporting of income.

- Interest Charges: Applied to amounts owed beyond the due date.

- Increased Scrutiny: May attract additional attention or audits from the IRS in subsequent years.