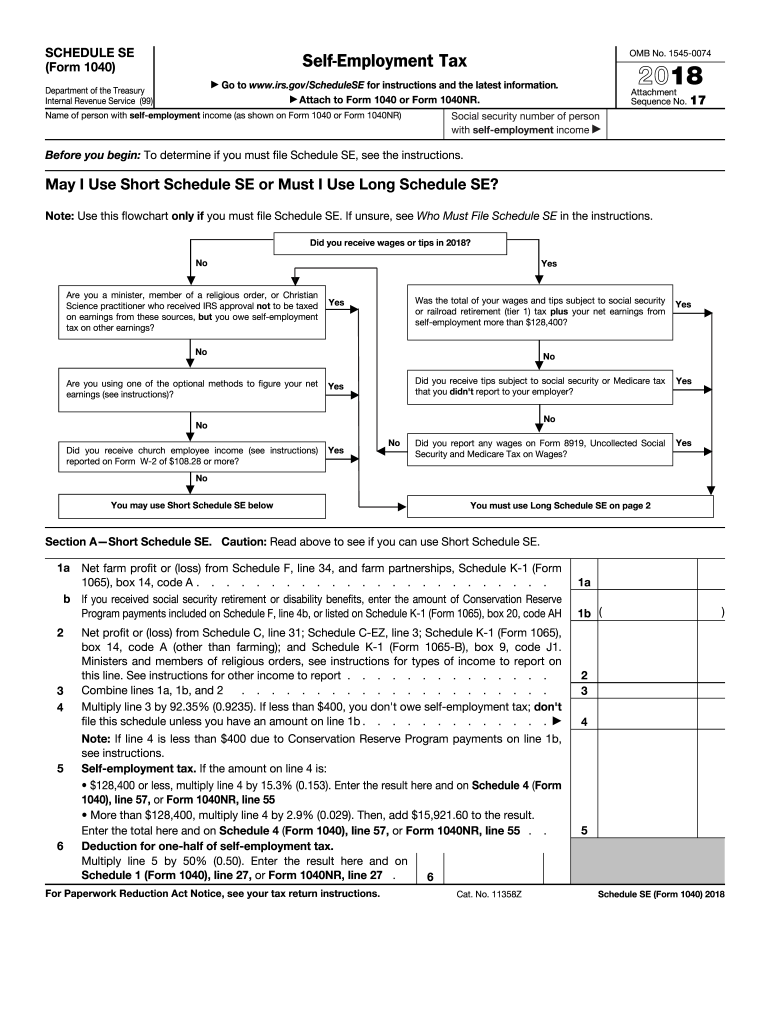

Definition & Meaning

Schedule SE (Form 1040) for 2016 is a critical IRS tax form used by self-employed individuals in the United States to calculate their self-employment tax obligation. This form ensures that individuals pay contributions toward Social Security and Medicare, mirroring the contributions made by employed individuals' payroll taxes. It's particularly relevant for freelancers, independent contractors, and small business owners who earn income not subject to standard payroll withholding.

Calculation Components

- Net Earnings from Self-Employment: This is the key figure on the Schedule SE. It includes gross income minus business expenses, giving self-employed individuals a basis for tax calculation.

- Self-Employment Tax Rate: A rate equivalent to the combined portions of Social Security and Medicare taxes must be calculated. For 2016, this is 15.3%.

How to Use the Schedule SE 2016

To effectively use Schedule SE 2016, individuals need to follow a structured process to ensure accurate tax computation and compliance.

Step-by-Step Instructions

- Gather Financial Records: Begin by collecting all relevant financial records for the tax year, including income statements and records of business expenses.

- Calculate Net Earnings: Determine your net earnings from self-employment by subtracting business expenses from gross income.

- Fill Out Part I (Short Schedule SE): Most self-employed taxpayers will use the Short Schedule SE unless they have specific circumstances such as church income or clergy housing allowances.

- Fill Out Part II (Long Schedule SE): Required if you have specific deductions or income types that make the simplified form inadequate.

Additional Considerations

- Health Insurance Deduction: Self-employed individuals can deduct health insurance premiums, which can impact the net earnings calculations.

- Social Security Wage Base: For 2016, only the first $118,500 of combined wages, tips, and net earnings is subject to the Social Security portion (12.4%) of the self-employment tax.

Steps to Complete the Schedule SE 2016

Completing Schedule SE requires precise attention to detail to prevent errors and ensure correct tax amounts.

Detailed Process

- Identify Correct Part (Short vs. Long): Review qualifications to determine if the Long Schedule SE is necessary.

- Computations: Carefully compute the self-employment tax using the figures derived from your income sources.

- Deductions: Implement applicable tax deductions. Use worksheets provided in the IRS instructions for nuanced deductions or complex situations.

- Transfer Amounts: Transfer computed amounts to the correct lines on your Form 1040 to complete the self-employment tax section.

Key Elements of the Schedule SE 2016

Understanding the components of Schedule SE is essential for proper completion and submission.

Major Sections

- Net Profit (or Loss): The foundation for all other calculations.

- Social Security and Medicare Tax: Calculated separately but summed to determine total liability.

- Deduction for One-Half of Self-Employment Tax: Offers a deduction for half of the liability as an adjustment to income.

IRS Guidelines

Adhering to IRS guidelines is pivotal to ensure compliance and avoid penalties.

Compliance Requirements

- Timely Filing: Ensure Schedule SE accompanies your Form 1040 to meet federal deadlines.

- Accurate Reporting: Misreporting income or deductions can lead to audits, penalties, and interest.

Important Terms Related to Schedule SE 2016

Understanding the terminology specific to Schedule SE can prevent errors and enhance comprehension.

Glossary

- Self-Employment Tax: Combined Social Security and Medicare tax for self-employed individuals.

- Net Earnings: Profits subject to self-employment tax after allowable business expenses.

- Deduction for One-Half of SE Tax: A deduction available to ease the burden of self-employment tax.

Required Documents

Gathering all necessary documentation beforehand simplifies the filing process and ensures accuracy.

Essential Records

- Income Statements: Documentation showing your income and revenue.

- Expense Receipts: Receipts relevant to deductible business costs.

- Prior Year Tax Returns: Useful for referencing previous calculations and ensuring consistency.

Who Typically Uses the Schedule SE 2016

Knowing who should use Schedule SE helps in identifying filing requirements.

Eligible Taxpayers

- Self-Employed Individuals: Those earning income from business activities not taxed at source.

- Independent Contractors: Professionals working freelance or on contract without traditional employment taxes withheld.

- Small Business Owners: Proprietors or partners in small businesses responsible for their Social Security and Medicare contributions.

This detailed breakdown not only elaborates on the core aspects of the Schedule SE for 2016 but also guides individuals in accurately completing and filing their tax forms, ensuring compliance with IRS regulations.