Definition and Purpose of the 2012 Schedule SE Form

The 2012 Schedule SE (Form 1040) is a tax form used by self-employed individuals in the United States to calculate their self-employment tax, which includes Social Security and Medicare taxes. This form is essential for ensuring that self-employed taxpayers contribute appropriately to the Social Security and Medicare systems, as these taxes are not automatically withheld by employers for self-employed individuals.

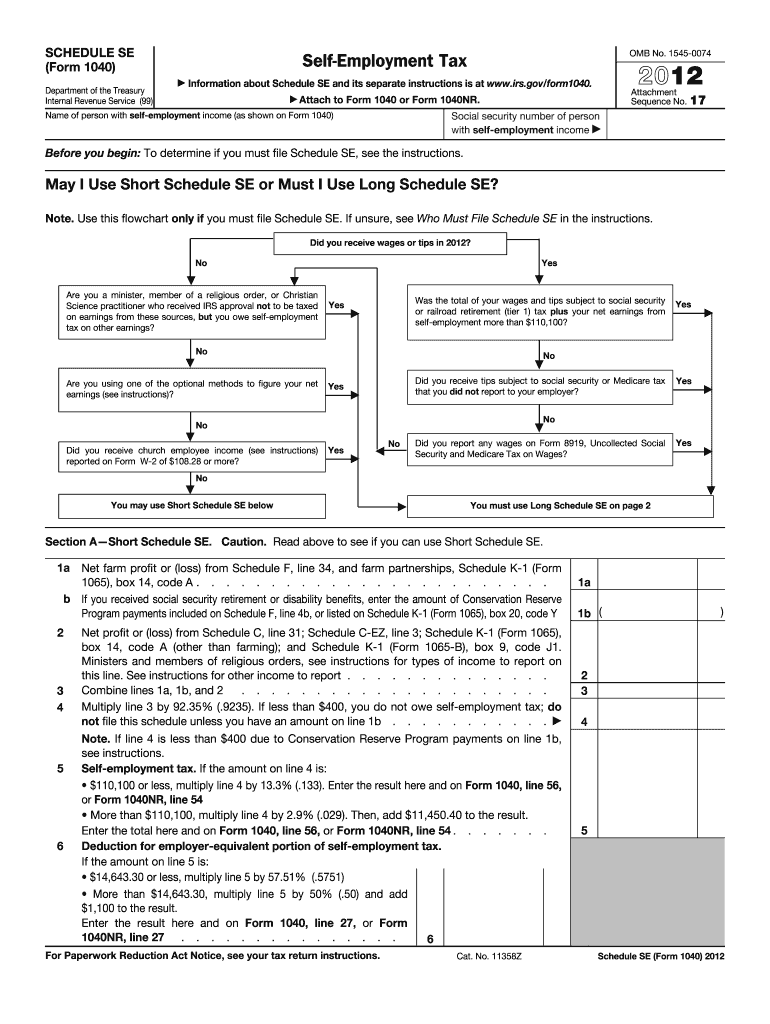

Eligibility Criteria for Using the Schedule SE Form

To use the 2012 Schedule SE, a taxpayer must be self-employed with a net income of $400 or more from self-employment, or they might be required if they receive church employee income of $108.28 or more. Farmers, sole proprietors, and independent contractors are common examples of individuals who would need to complete this form. The form helps determine whether one qualifies for the Short Schedule SE or Long Schedule SE, which is determined by specific conditions affecting the calculation of taxes owed.

Key Elements of the 2012 Schedule SE Form

- Net Farm Profit or Loss: Required for individuals involved in farming activities, this section reports taxable income or loss from farming.

- Net Profit from Self-Employment: Includes income from business activities minus allowable deductions.

- Optional Methods: Provides an alternative method for calculating net earnings from self-employment, typically beneficial in certain circumstances to qualify for Social Security benefits.

How to Obtain the 2012 Schedule SE Form

The 2012 Schedule SE form can be obtained from several sources, including the IRS website, where it can be downloaded and printed. Additionally, tax preparation software typically includes this form during the workflow of preparing a tax return for the year 2012.

Steps to Complete the 2012 Schedule SE Form

- Calculate Self-Employment Income: Determine the total business income and subtract any business expenses to ascertain net earnings.

- Check Qualification for Short or Long Schedule SE: Identify which parts of the form are applicable based on unique income situations.

- Complete Required Sections: Accurately fill out applicable areas, ensuring calculations for Social Security and Medicare taxes are correct.

- Review and Attach to Form 1040: Ensure the form is filled out correctly before attaching it to the Form 1040.

Filing Deadlines and Important Dates

The filing deadline for the 2012 Schedule SE Form, in conjunction with the Form 1040, was April 15, 2013. Extensions could be requested, providing delays until October 15, 2013. Missing these deadlines without an extension could result in penalties.

IRS Guidelines for the 2012 Schedule SE Form

The IRS guidelines specify that all self-employed individuals must accurately report their earnings and calculate their self-employment tax using the Schedule SE form. Failure to comply could result in interest and penalties for underpayment.

Important Terms Related to the Schedule SE Form

- Self-Employment Tax: Comprises Social Security and Medicare taxes owed by self-employed individuals.

- Net Earnings: The remainder of gross income after deducting allowable business expenses.

- Optional Methods: Alternative methods for calculating self-employment income, often used to increase eligibility for Social Security benefits.

Penalties for Non-Compliance

Failure to file the Schedule SE form, or underreporting income, can lead to significant penalties from the IRS. The penalties range from interest on unpaid taxes to more severe consequences, such as fines or legal actions, in cases of deliberate evasion.