Definition & Meaning

Form 1120-L, the U.S. Life Insurance Company Income Tax Return, is essential for life insurance companies to report their income, deductions, and tax calculations. This form is applicable for the tax years 2017 through 2019 and caters specifically to the financial reporting needs of U.S.-based life insurance entities. The structure of the form includes various schedules that deal with specific types of income such as dividend and investment income, reserves, and policy acquisition expenses, making it a specialized financial document tailored for the insurance sector.

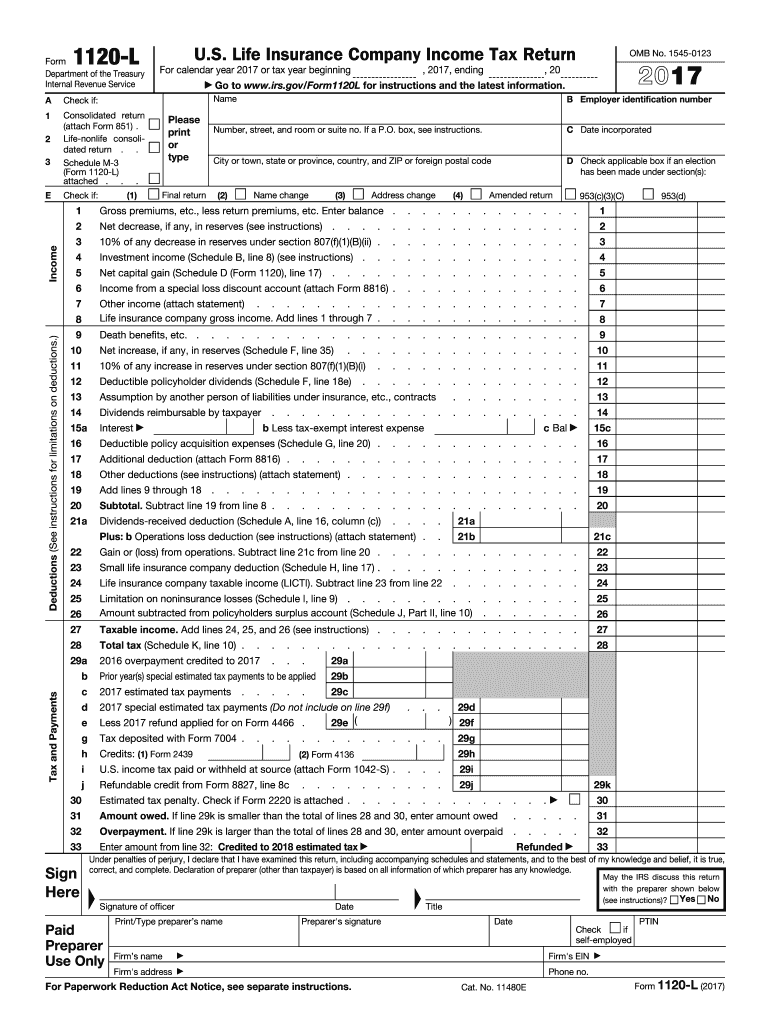

How to Use the 1120-L 2 Form

Using Form 1120-L requires a comprehensive understanding of the financial activities specific to a life insurance company. Companies need to:

- Report all income streams, which include but are not limited to investment income and taxable interest.

- Subtract allowable deductions specific to insurance operations to determine taxable income.

- Calculate company tax liabilities based on the net income and applicable tax regulations during the years 2017 to 2019.

- Ensure compliance with federal regulations by using the correct line items and completing all necessary schedules for comprehensive financial reporting.

Steps to Complete the 1120-L 2 Form

- Gather Financial Documents: Accumulate all necessary financial records including income statements, transaction logs, and expense reports.

- Fill Out Personal and Company Information: Enter accurate identification information for the company, including name, address, and Entity Identification Number (EIN).

- Calculate Income and Deductions: Itemize all sources of income and potential deductions in their respective sections.

- Complete Schedules: Attach and fill out relevant schedules for complex financial descriptions, such as Schedule F for dividend income.

- Review and Validate Entries: Double-check all calculations and ensure all data is correctly input into the form.

- Submit to IRS: Follow IRS submission guidelines for mailing or electronic submission.

Who Typically Uses the 1120-L 2 Form

The primary users of the Form 1120-L are U.S.-based life insurance companies that need to report their annual financial activities to the IRS. This group includes both small and large entities engaged in underwriting, managing life insurance policies, and handling financial reserves related to such insurance products. Typically, financial and tax professionals within these organizations are responsible for completing the form.

Key Elements of the 1120-L 2 Form

- Income Section: Details gross income from different channels, including standard and specific entries for insurance-related revenues.

- Deductions: Lists permissible deductions exclusive to insurance companies, which could include policyholder benefits and claims.

- Tax Calculations: Outlines steps for calculating the taxes owed, reflecting applicable credits, and estimating quarterly payments.

- Schedules: Includes various schedules, like Schedule F, which details the dividend income and specific computations critical for accurate tax filings.

IRS Guidelines

The IRS provides comprehensive instructions for filling out Form 1120-L, ensuring compliance with federal tax laws applicable to life insurance companies. These guidelines include:

- Defining Taxable Items: Clarifies what constitutes taxable income for life insurance companies.

- Deductions and Credits: Specifies allowable deductions and available credits for tax reduction.

- Submission Requirements: Details deadlines and precise documentation needed for successful form submission.

Filing Deadlines / Important Dates

For the years 2017 to 2019, Form 1120-L follows standard corporate filing deadlines outlined by the IRS:

- Regular Deadline: Generally due by the 15th day of the fourth month following the end of the fiscal year.

- Extensions: Companies can file for an extension using Form 7004, extending the deadline by six months.

Penalties for Non-Compliance

Failure to comply with the filing requirements of Form 1120-L can lead to significant penalties:

- Late Filing Penalties: Charged if the form is submitted past the deadline without an approved extension.

- Inaccurate Reporting Penalties: Levied for intentional or recurrent mistakes, including incorrect financial reporting or insufficient documentation.

Understanding these components and following thorough preparation processes ensure accurate and timely filing of the 1120-L form for the specified tax years, thus maintaining compliance and avoiding any potential penalties.