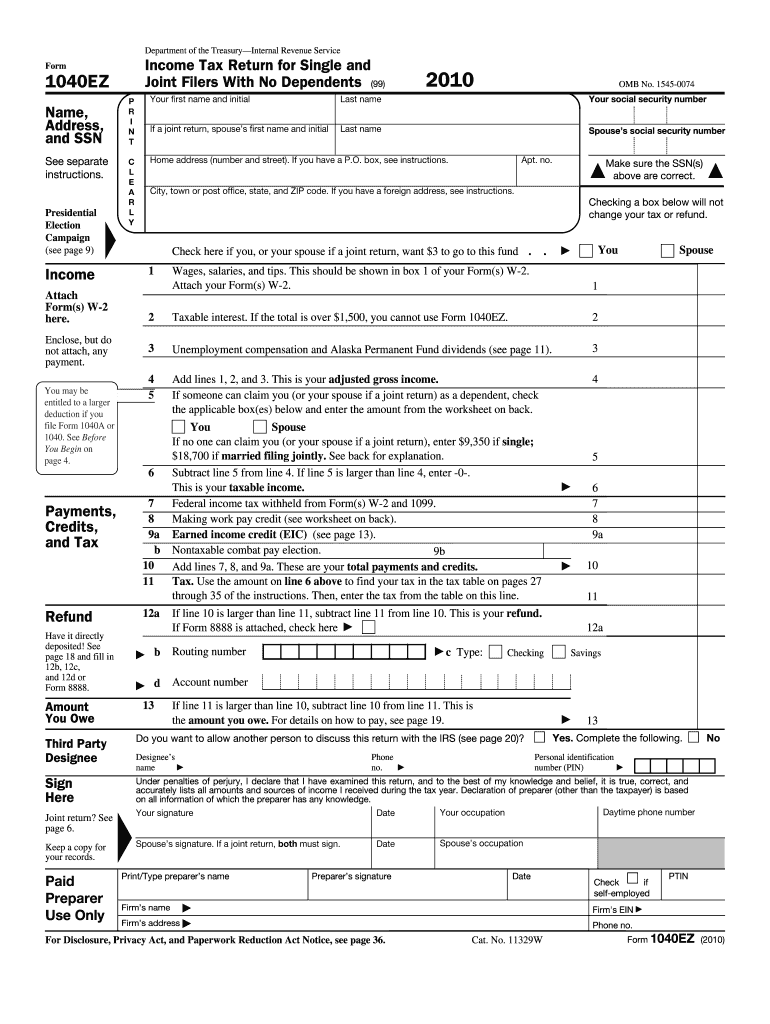

Definition & Purpose of the 2010 Form 1040EZ

The 2010 Form 1040EZ was a simplified income tax form designed for single and joint filers with no dependents. Issued by the Internal Revenue Service (IRS), it was intended for taxpayers with uncomplicated financial situations, usually involving straightforward income sources like wages, salaries, tips, and unemployment compensation. The form aimed to streamline the tax filing process for eligible taxpayers, allowing them to bypass the more complex Form 1040 or 1040A. Key features of the 1040EZ included sections where filers reported personal information, income, and deductions, ultimately aiding in calculating any refunds or owed taxes for the year.

Key Elements of the Form

- Personal Information: The initial section required basic identification details, including the taxpayer's full name, Social Security number, and home address.

- Income Reporting: Applicants reported their income from only the simplest sources, such as earnings from jobs and interest from bank accounts, not exceeding $1,500.

- Taxable Income Calculation: The form included spaces for filers to specify any adjustments to income and calculate adjusted gross income.

- Tax Credit and Payment Details: It prompted users to apply any tax credits and payments already made throughout the year to determine final tax responsibilities or refunds.

Steps to Complete the 2010 Form 1040EZ

Filling out the 2010 Form 1040EZ involved a systematic approach. Follow these steps for a clear process:

- Gather Necessary Documents: Collect your W-2 forms, 1099s, and any pertinent receipts or documentation for income and tax payments made.

- Fill in Basic Information: Begin with personal details such as name, address, and Social Security number.

- Enter Income Data: Record your income from W-2 forms and eligible interest, ensuring it aligns with your documentation.

- Calculate Adjustments and Taxable Income: Use provided sections to make adjustments and find the gross taxable income.

- Apply Tax Credits and Prepaid Taxes: Include any earned income credits and account for taxes already paid through withholding or estimated payments.

- Determine Refunds or Amounts Owed: Subtract total payments and credits from the calculated tax to discover whether you'll receive a refund or owe additional taxes.

- Review and Sign: Carefully review the form for accuracy before signing and dating it.

Important Reminders

- Double-check math calculations to avoid discrepancies.

- Ensure all information matches supporting documents.

- Keep copies of your completed form and all submissions for personal records.

Who Typically Uses the 2010 Form 1040EZ

The 2010 Form 1040EZ was specifically tailored for taxpayers who met specific criteria. Typical users included:

- Single and Joint Filers: Primarily those without dependents and straightforward financial situations.

- Young Professionals and Students: Often individuals with simple income streams, such as wages or tips, and minimal investments or deductions.

- Retired Individuals: If they had uncomplicated income and did not qualify for more complex tax situations.

Eligibility Criteria

To use the 1040EZ, filers needed to meet the following parameters:

- Total income was below $100,000 for the year.

- No dependents were claimed.

- Filing status must be single or married filing jointly.

- Interest income was $1,500 or less.

- No income from self-employment was reported.

Legal Implications and Use of the 2010 Form 1040EZ

The legal framework surrounding the 1040EZ ensured that it was used solely by qualifying taxpayers to meet federal tax obligations. The form served to report taxable income accurately and prevent fraud through honest declarations of earnings and applicable deductions. Misuse or erroneous filings could trigger audits, fines, or fraud penalties.

Potential Penalties for Non-Compliance

- Incorrect Filings: Errors might lead to audits or correction requests from the IRS, which could delay refunds or necessitate additional payments.

- Misrepresentation: Intentional misstatements held the risk of hefty fines or even legal action for tax evasion.

IRS Guidelines and Filing Deadlines

The IRS provided specific guidelines on when and how to submit the 1040EZ form. Adhering to these guidelines ensured compliance and minimized potential tax-related issues.

Important Dates

- Filing Deadline: Traditionally due by April 15 of the following year, although extensions or adjustments could apply based on IRS rules.

- Refund Issuance: Direct deposits for refunds were typically processed faster than paper checks, often within a few weeks of submission.

Submission Methods

- Electronic Filing: Utilizing e-file services, whether through tax software or an authorized provider, expedited the process and reduced potential for manual errors.

- Mail: Hard copies sent via mail required careful adherence to mailing instructions, including using correct addresses and postage.

Examples and Use Cases for the 2010 Form 1040EZ

Real-world examples highlight how the form can be effectively utilized by the prescribed demographic.

Example Scenarios

- Recent Graduates: A graduate secures their first full-time role, with only W-2 wage income, making the 1040EZ ideal for straightforward tax filings.

- Entry-Level Workers: An individual working several part-time jobs over the year without complex financial affairs uses the form for its simplicity.

Alternatives to the 2010 Form 1040EZ

Over time, the simplicity offered by 1040EZ saw declines as the IRS favored more comprehensive forms to encapsulate ongoing financial nuances.

Form 1040A

The next level of complexity allowed for additional deductions and credits beyond the scope allowable by Form 1040EZ.

Full 1040 Form

Best suited for filers with diverse income streams, such as investments and self-employment, or those with a range of deductions and larger families.

Including step-by-step approaches, detailed scenarios, and historical contexts helps in understanding the utility of the 2010 Form 1040EZ. Such in-depth coverage ensures comprehensive guidance, highlighting relevance and the function of the form in the American tax landscape.