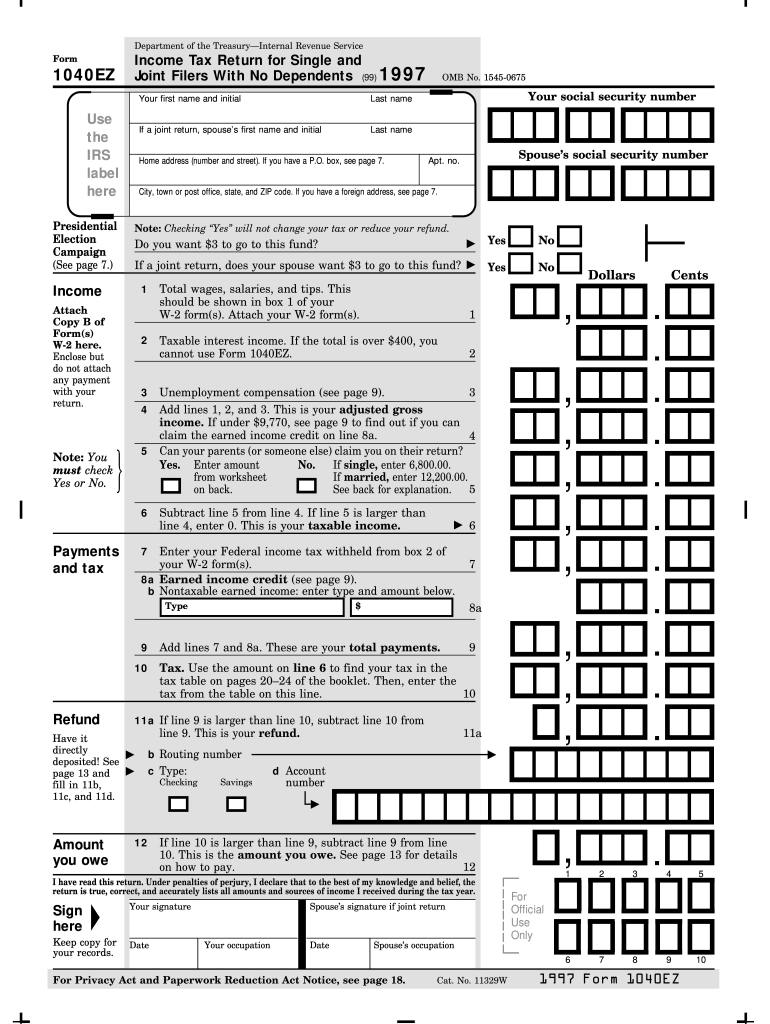

Definition and Purpose of the 1997 Form 1040EZ

The 1997 Form 1040EZ is a simplified income tax return form specifically designed for single and joint filers without dependents. It is intended to streamline the process of reporting income, calculating taxable income, and determining the amount of tax owed or refunded. Those using this form typically have uncomplicated tax situations, which include having no dependents, various types of income, such as wages, salaries, and tips, and a taxable income below a certain threshold. By focusing on straightforward financial circumstances, the Form 1040EZ allows for a less complex filing experience compared to more detailed forms like the 1040A or the standard 1040.

Steps to Complete the 1997 Form 1040EZ

To accurately fill out the 1997 Form 1040EZ, follow these detailed steps:

-

Gather Personal Information: Begin by providing your basic details such as name, address, and Social Security Number. If filing jointly, include your spouse's information as well.

-

Report Income: Enter your total income, including wages, salaries, and tips, from Form W-2. Ensure all figures are copied accurately to avoid discrepancies.

-

Calculate Adjusted Gross Income (AGI): The Form 1040EZ does not offer many deductions, so your AGI will be your total income unless you have qualifying adjustments.

-

Determine Tax Liability: Use the tax table provided in the IRS instructions for the Form 1040EZ to calculate your tax based on your taxable income.

-

Check Withholding and Payments: Complete this section with information from your W-2 to determine if you have overpaid or underpaid your taxes throughout the year.

-

Determine Refund or Amount Owed: Subtract the total tax withheld from your tax liability to see if you are entitled to a refund or if you owe additional tax.

-

Sign and Submit: Conclude by signing the form. If filing jointly, both spouses must sign. Submit it by mail to the IRS, using the address provided in the form’s instructions.

Eligibility Criteria for Using Form 1040EZ

The 1997 Form 1040EZ has specific eligibility criteria designed to limit its use to simpler tax situations. Filers must:

- Be single or married filing jointly.

- Have no dependents.

- Earn income only from wages, salaries, tips, taxable scholarships, or unemployment compensation.

- Have a taxable income below set limits.

- Not claim any deductions or credits aside from the earned income credit.

- Not have interest income over $400. These requirements ensure that only those with straightforward financial situations use the form, as this form doesn't accommodate more complex filings.

Required Documents for Filing

To complete the 1997 Form 1040EZ, gather the following essential documents:

- W-2 Forms: These should detail all income from wages and provide information on tax withholding.

- Form 1099s: Required if any taxable scholarships or unemployment compensation apply.

- Interest Income Statements: Such as those from a bank, provided your interest income is under $400.

- Previous Year’s Tax Return: Useful for reference and to ensure consistency. Having these documents on hand facilitates accurate and timely completion of the form.

Key Elements of the 1997 Form 1040EZ

Key elements of the form include:

- Personal Information Section: Where you fill out identifying details.

- Income Section: For reporting total income, including wages, salaries, and tips.

- Adjustments to Income: Limited on this form to maintaining simplicity.

- Taxable Income Calculation: Using simple arithmetic for easier understanding.

- Refund Information: Must provide bank information if you opt for direct deposit. These elements help ensure the taxpayer provides comprehensive information necessary for the IRS to assess their tax situation accurately.

IRS Guidelines for Form 1040EZ

The IRS provides specific guidelines to assist with Form 1040EZ filing:

- Follow the income and filing status criteria to confirm eligibility.

- Use the IRS-provided tax tables to accurately calculate tax liability and refunds.

- Ensure submissions are postmarked by the federal tax filing deadline, which is typically April 15, unless extended due to weekends or holidays. Adhering to these guidelines helps avoid common errors and ensures compliance with federal tax requirements.

Penalties for Non-Compliance

Non-compliance with requirements associated with the 1997 Form 1040EZ can result in several potential penalties:

- Failure to File: If you miss the filing deadline without an IRS-approved extension, you may incur a penalty.

- Failure to Pay: Not paying taxes by the due date can lead to interest charges and additional penalties on the unpaid tax amount.

- Accuracy-Related Penalty: Errors resulting from negligence or unsupported claims can yield monetary penalties. Maintaining accuracy and timeliness is crucial to avoiding these penalties.

Filing Deadlines and Important Dates

Filing deadlines for the 1997 Form 1040EZ include the following:

- Federal Tax Filing Deadline: Typically April 15, with exceptions for weekends or holidays.

- Extension Requests: Must be submitted by the filing deadline to avoid penalties for late filing.

- State Filing Deadlines: These can vary, so verify with your state's tax agency for precise dates. It's critical to comply with these deadlines to avoid penalties, interest charges, or missing out on a timely refund.