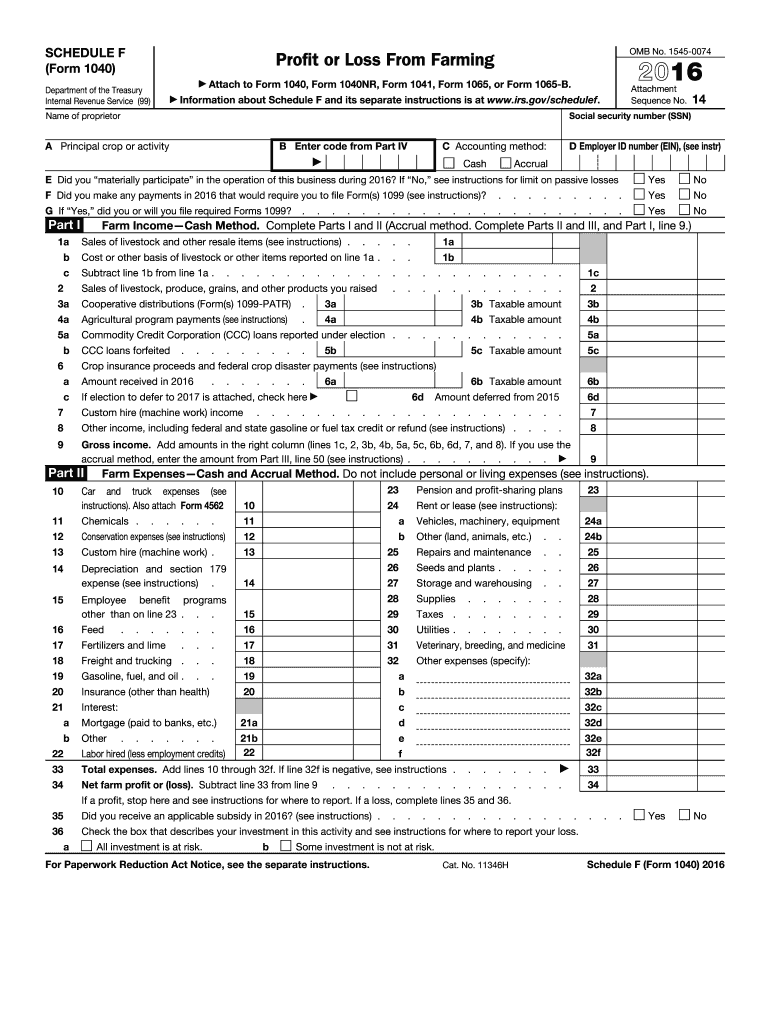

Definition & Purpose of Schedule F (Form 1040)

Schedule F (Form 1040) is a tax document used by farmers to report their income or losses from agricultural activities for the tax year 2016. It plays a critical role in calculating taxable income by detailing profits from sales of livestock, crops, and other farm products. The form also allows farmers to claim deductions for related expenses, such as feed, fertilizer, seed, and equipment depreciation. Understanding the exact purpose of Schedule F can help ensure precise tax reporting and maximize potential tax benefits for those engaged in farming activities.

Steps to Complete the IRS 2011 Schedule F 2016 Form

-

Gather Necessary Financial Records: Before starting, ensure you have records of all farming income and expenses, such as sales receipts, invoices, and bank statements.

-

Provide Income Details: Enter gross income from the sale of livestock, produce, grains, and other products. Include any cooperative distributions, agricultural payments, and crop insurance proceeds.

-

List Farming Expenses: Deductible expenses must be itemized in the form, including seeds, fertilizer, feed purchased for livestock, salaries paid to employees, vehicle expenses, and depreciation of farming equipment.

-

Accounting Method Disclosure: Specify the accounting method used—either cash or accrual accounting—as it affects revenue recognition and expense reporting.

-

Report Net Farm Profit or Loss: Calculate the net profit or loss by subtracting total expenses from total income. This figure will be transferred to Form 1040 on the appropriate line.

-

Complete Additional Sections: Fill out any additional information required, such as details of any supporting forms or schedules.

Key Elements of the IRS 2011 Schedule F 2016 Form

-

Income Section: Records all sources of income related to farming activities, critical for determining gross revenue.

-

Expense Section: Details deductible expenses that reduce taxable income, including both direct and indirect costs incurred during farming.

-

Net Profit Calculation: The culmination of the income and expense sections, it determines the financial outcome of farming operations for the year.

-

Accounting Method: Indicates whether cash or accrual methods are used, impacting income and expense recognition.

How to Obtain the IRS 2011 Schedule F 2016 Form

-

Online Download: The form is available for download on the official IRS website. Ensure you have the latest version to avoid any discrepancies.

-

Local IRS Office: Physical copies can be procured from an IRS office. Assistance is available if you have questions about filling out the form.

-

Tax Software: Many commercial tax software packages, like TurboTax and QuickBooks, include Schedule F and guide users through the completion process.

Who Typically Uses the IRS 2011 Schedule F 2016 Form

Schedule F is predominantly used by individuals or entities engaged in farming as a business operation. This includes sole proprietors, partnerships, estates, and trusts involved in producing crops, dairy, poultry, beef, or similar goods. Farmers operating as self-employed entities, LLCs, or corporations may also use this form to report and manage their agricultural income and expenses.

Important Terms Related to the IRS 2011 Schedule F 2016 Form

-

Gross Income: Total revenue received from all farming activities before any expenses are deducted.

-

Depreciation: A method to allocate the cost of a tangible asset over its useful life, which can be deducted to reduce taxable income.

-

Cooperative Distribution: Payments received from agricultural cooperatives, which must be reported as part of farming income.

-

Principal Agricultural Activity Code: A specific code on the form used to identify the primary farming activity, facilitating proper record classification.

IRS Guidelines for Completing Schedule F

The IRS provides detailed guidelines for completing Schedule F, which ensure compliance with tax laws. These guidelines cover the appropriate classification of deductions, eligibility for specific credits, proper revenue reporting, and the use of supporting documents. Adhering to these guidelines helps prevent errors and avoids potential audits or penalties.

Filing Deadlines & Important Dates

-

Tax Filing Deadline: Typically due by April 15 of the year following the taxable year, unless an extension is filed.

-

Extension Deadline: If a six-month extension is filed, the deadline for submission extends to October 15. Additional forms and instructions are needed to apply for this extension.

Understanding and following these timelines is crucial to avoid late fees and interest charges on unpaid taxes.