Definition and Meaning of the 2014 Form F

The 2014 Form F is a part of the U.S. tax documentation used primarily by farmers to report financial data from their agricultural business. This form is officially known as "Schedule F," which accompanies Form 1040, and it captures the income and expenses related to farming activities. Its primary purpose is to offer a detailed account of profits or losses from these operations. By maintaining an organized summary of agricultural finances, farmers can effectively report their annual income to the Internal Revenue Service (IRS).

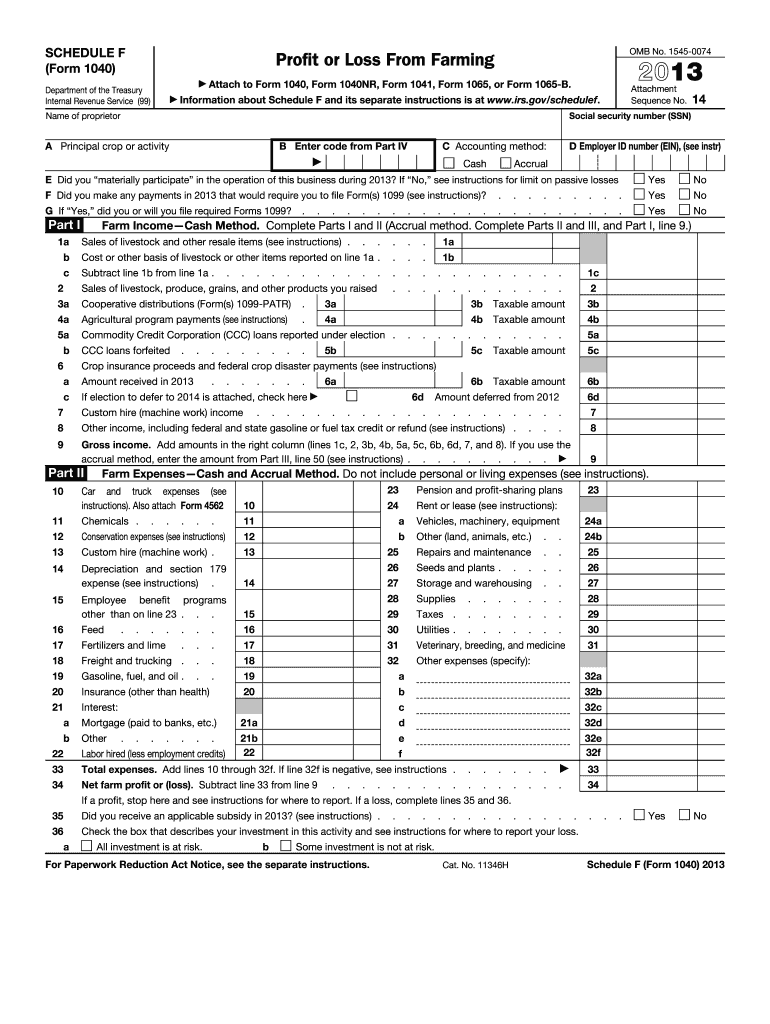

Steps to Complete the 2014 Form F

-

Gather Financial Records: Start by collecting all relevant financial documents, such as receipts, sales invoices, expense records, and previous tax returns. Keeping accurate records is essential for completing the form without discrepancies.

-

Calculate Income: Document all income sources from farming activities, including sales of livestock, produce, grains, and other products. Pay careful attention to any barter exchanges or cooperative distributions that may contribute to taxable income.

-

List Expenses: Accurately itemize deductible expenses, including costs related to feed, fertilizer, seed, repairs, and interest on loans. Ensure that documentation supports each deduction claim to avoid potential audits.

-

Complete Sections: Follow each section of the form, filling in income and expense details as instructed. Ensure accuracy by double-checking figures and ensuring that all totals balance correctly.

-

Attach the Form to 1040: Once completed, attach Schedule F to your Form 1040. This combined documentation should then be submitted to the IRS according to filing instructions.

How to Obtain the 2014 Form F

Farmers can obtain Schedule F for 2014 from several sources:

-

IRS Website: Download the form directly from the IRS official site, where various tax forms are available for direct access.

-

Tax Preparation Software: Software like TurboTax or QuickBooks often includes the ability to fill out and file the Schedule F when preparing taxes.

-

Tax Professional: Engage a certified public accountant (CPA) or tax professional who can provide and help complete the form.

Who Typically Uses the 2014 Form F

Schedule F is specifically designed for individuals engaged in farming activities. Users typically include:

-

Individual Farmers: Those who personally manage and operate their own farming businesses, regardless of the size or scale of activities.

-

Partnerships and LLCs: Entities structured as partnerships or limited liability companies where profits and losses are passed through to individual partners/members must also file using this form.

-

Corporations: C-Corporation and S-Corporation tax filers might use Form 1120 or 1120S, but they must file Schedule F for any farming activities as a supplementary document.

Key Elements of the 2014 Form F

-

Section A - Principal Crop or Activity: Identify the main agricultural products or activities your farm engaged in throughout the year.

-

Section B - Income: List gross income received from sales, cooperative dividends, insurance proceeds, and other farm-related income sources.

-

Expenses: Break down deductible costs into subcategories, such as chemicals, conservation expenses, labor hired, and repairs. This section is pivotal in reducing taxable income effectively.

Legal Use of the 2014 Form F

Ensuring compliance with tax laws through accurate reporting on Schedule F is critical. Farmers must:

-

Accurately Report Income: Misreporting income can lead to penalties and audits, which could hamper financial operations and lead to additional scrutiny by the IRS.

-

Maintain Documentation: Proper documentation, including receipts and invoices, should be retained for at least three years in case verification by tax authorities is needed.

IRS Guidelines for the 2014 Form F

The IRS provides explicit instructions for completing Schedule F:

-

Record-Keeping: Maintain detailed records of all farm-related financial transactions to substantiate entries on the form.

-

Depreciation and Capital Expenses: Capitalize and depreciate the cost of certain farm properties over time, following IRS depreciation rules.

Filing Deadlines and Important Dates

-

Federal Deadline: Typically, personal tax returns, including Schedule F, are due on April 15, unless extensions apply.

-

Estimated Taxes: Farmers may need to pay estimated taxes quarterly if they expect to owe more than a certain amount when filing, as specified by IRS guidelines.

Required Documents for Form Submission

To complete Schedule F accurately, gather:

-

Sales Receipts: For products sold, including any supporting documents relating to income.

-

Expense Statements: Detailing outlays for supplies, equipment, labor, and other operational costs.

-

Loan Agreements: Particularly those related to equipment purchases or operational financing that impact deductible expenses.