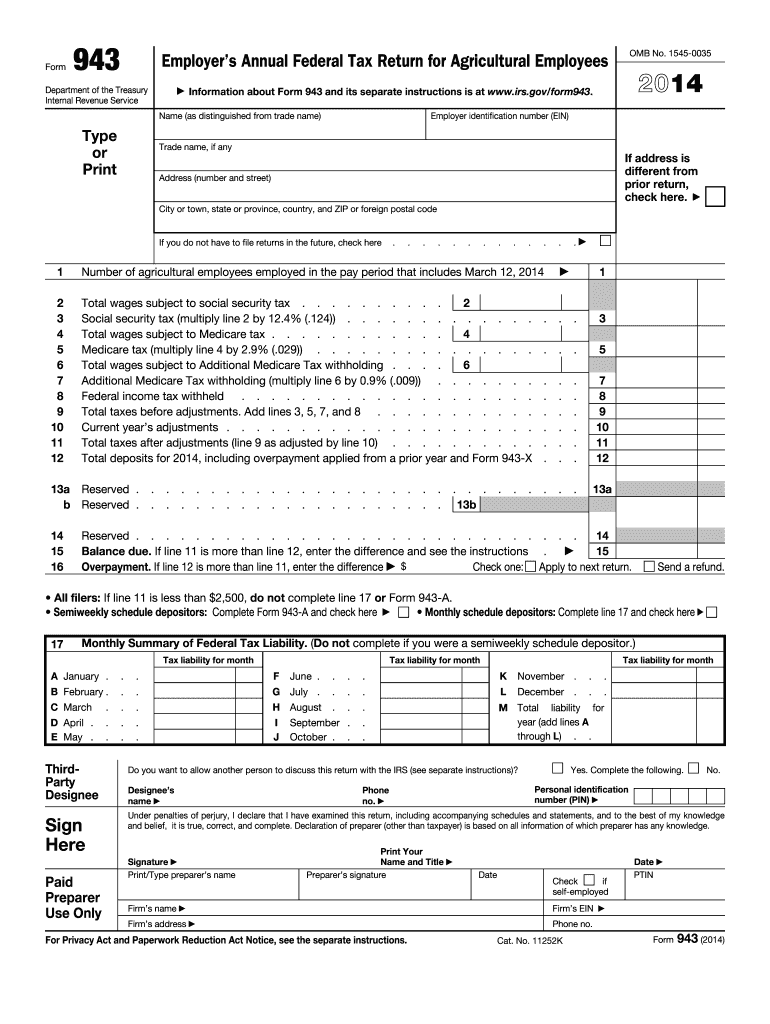

Definition and Purpose of Form 943

Form 943, officially known as the Employer's Annual Federal Tax Return for Agricultural Employees, is a mandatory document that agricultural employers in the United States use to report the taxes withheld from farm workers' wages. This form addresses key taxation components such as Social Security and Medicare taxes. It's a critical tool for ensuring compliance with federal tax obligations specific to the agricultural sector. Unlike other employer-based forms, Form 943 is tailored to capture data pertinent to seasonal and year-round agricultural labor, adding a layer of accuracy to the industry's tax reporting processes.

Important Features of Form 943:

- Employer Identification: Requires detailed information about the employer to ensure proper tracking and assessment.

- Tax Calculations: Specific sections are designed for calculating Social Security and Medicare taxes on agricultural wages.

- Integrated Payment System: Accompanied by Form 943-V, a payment voucher that allows employers to include tax payments directly to the IRS.

Obtaining the 2014 Form 943

Agricultural employers looking to file Form 943 for the year 2014 can acquire this document directly from the IRS’s official website or request a paper version through mail. Accessing the form through digital platforms simplifies the process, allowing employers to download, complete, and submit it efficiently. Additionally, specialized tax preparation software like TurboTax or QuickBooks may provide integrated support for this form, ensuring accurate and streamlined processing.

Steps to Access the Form:

- Visit IRS Website: Navigate to the forms section and search for Form 943 for 2014.

- Download or Request a Copy: Choose between downloading a PDF version or requesting a mailed copy.

- Review Software Compatibility: Check if your tax preparation software directly supports Form 943 for seamless integration.

Completing the 2014 Form 943

Accurate completion of Form 943 requires careful navigation through various sections. Employers must diligently report all pertinent wage information and tax withholdings. Adequate attention to detail during the filling process minimizes errors and potential non-compliance implications.

Key Steps for Completing the Form:

- Employer Information: Enter employer identification details accurately.

- Wages and Tax Calculations: Detail the total wages paid and the corresponding Social Security and Medicare taxes.

- Payment and Adjustments: Integrate any necessary adjustments or corrections from previous forms or payments.

- Filing and Submission: Ensure all calculations are checked before filing; late or incorrect submissions might incur penalties.

Legal Considerations and Compliance

Employers filing Form 943 must adhere to legal guidelines set by the IRS. Ensuring compliance involves understanding the penalties associated with non-submission or misrepresentation. All provided information should be truthful and reflective of actual business operations to avoid legal repercussions.

Compliance Points:

- Accurate Reporting: Confirm that all reported wages and taxes are accurate and verified.

- Amendments: In case of errors, filings must be amended promptly to reflect accurate information.

- Record Keeping: Maintain comprehensive records of filed forms and supporting documentation for at least four years.

Where and How to Submit Form 943

Form 943 can be submitted either electronically or via mail. Each submission method has its nuances and offers agricultural employers flexibility in how they report their tax obligations. Electronic filing is often encouraged due to its efficiency and reduced error rates.

Submission Options:

- Electronic Filing: Use IRS-approved e-file systems for a quicker and more secure submission.

- Mail Submission: Send completed forms to the appropriate IRS address as indicated in the form’s instructions.

- Consideration of Deadlines: Always adhere to the IRS’s designated deadlines for form submission to avoid penalties.

IRS Guidelines and Filing Deadlines

The IRS provides extensive guidelines to assist employers in correctly filing Form 943. These guidelines help clarify eligibility criteria, necessary documentation, and specific deadlines. Understanding these deadlines is crucial for operating within federal compliance parameters.

Filing Deadline:

- Form 943 is generally due by January 31 following the tax year.

Additional Support:

- The IRS offers resources and customer support lines for questions specific to Form 943 and other agricultural employment taxes.

Penalties for Non-Compliance

Failing to correctly file Form 943 within the prescribed timelines can lead to significant penalties. Understanding the potential financial and operational impacts of non-compliance encourages diligence in tax preparation and filing processes.

Types of Penalties:

- Late Filing Fees: Charges for failing to submit the form by the deadline.

- Underpayment Penalties: Consequences for inaccurately reporting or underpaying taxes owed.

Variants and Related Forms

Form 943 has evolved over time, with adjustments reflecting changes in tax laws and agricultural employment practices. Alternative forms may apply depending on the specific nature or scale of agricultural operations, particularly when dealing with multiple forms of employment within a single business entity.

Related Forms:

- Form 943-V: Payment voucher used to accompany the tax return when submitting payments.

- Other Employer Tax Forms: Forms such as Form 941 for non-agricultural employees, which may be required for businesses with diverse employment settings.

Implications for Different Business Entities

Various business structures, including LLCs, corporations, and partnerships, may have unique requirements when it comes to filing Form 943. Each entity must navigate its specific obligations, considering the multiplicity of state-specific regulations affecting agricultural taxation.

Business Entity Considerations:

- LLCs and Corporations: Would need to assess the influence of combined agricultural and non-agricultural employment on tax obligations.

- Partnerships: Entities must evaluate how shared ownership influences tax reporting and liability.

By fully understanding the complexities of Form 943, employers can better ensure compliance, maximize efficiency, and optimize their approach to federal agricultural tax obligations.