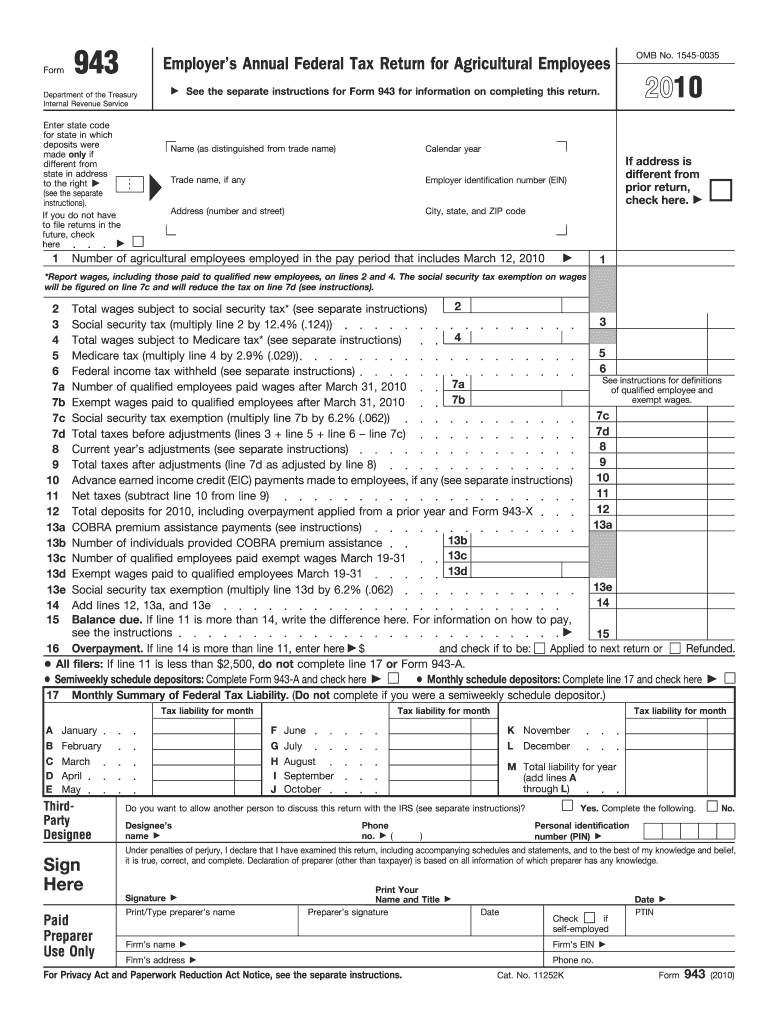

Understanding the 2010 Form 943

The 2010 Form 943 is the Employer's Annual Federal Tax Return for Agricultural Employees, which is specifically designed for employers in the agricultural sector. It requires employers to report wages paid to agricultural workers and taxes withheld, facilitating the appropriate management of tax liabilities associated with agricultural employment.

How to Use the 2010 Form 943

Employers need to use the 2010 Form 943 to accurately report the total wages paid to their agricultural employees and the amount of federal income tax, Social Security, and Medicare taxes withheld. This report is crucial for maintaining compliance with federal tax regulations specific to agricultural employment.

Steps to Complete the 2010 Form 943

- Gather Information: Collect all necessary payroll data for agricultural employees for the entire calendar year.

- Calculate Total Wages: Total all cash wages paid to each employee during the year.

- Determine Tax Withholdings: Calculate the amount of Social Security and Medicare taxes withheld from those wages.

- Complete Required Sections: Fill out each section of the form, including employer identification details, wages, and tax withholdings.

- Review and Verify: Double-check all entries for accuracy to avoid errors and potential penalties.

- Submit the Form: File the completed form with the IRS by the deadline.

Filing Deadlines for the 2010 Form 943

The form must be filed with the IRS by January 31st of the year following the reporting period. Employers who have deposited all taxes on time and in full may file by February 10th. It's critical to adhere to these deadlines to avoid late filing penalties.

Key Elements of the 2010 Form 943

- Employer Identification Number (EIN): Unique number issued by the IRS for tracking tax responsibilities.

- Wages Paid: Total cash wages paid to agricultural employees.

- Federal Tax Withholdings: Social Security and Medicare taxes withheld.

- Adjustments: Any adjustments needed for over- or under-paid taxes.

Required Documentation for Filing

To complete the form, employers need their payroll records, records of tax deposits made throughout the year, and any correspondence from the IRS concerning previous filings or tax obligations.

Legal Use of the 2010 Form 943

This form is a legally required document for agricultural employers who pay wages to farmworkers. Failure to file this form or filing it inaccurately can result in penalties or legal action by the IRS.

Penalties for Non-Compliance

Failure to file the 2010 Form 943 by the deadline, filing an inaccurate form, or failing to pay the required taxes can result in financial penalties. The IRS may impose fines based on the amount of tax due and the duration of the delay in filing.

Electronic vs. Paper Submissions

Employers have the option to file Form 943 electronically or via paper submission. Electronic filing through tax software may simplify the process and reduce errors, while paper filing requires mailing the physical form to the IRS.

IRS Guidelines for the 2010 Form 943

The IRS provides detailed instructions accompanying the form to assist employers in correctly completing the form. These guidelines help ensure compliance and provide clarity on specific provisions related to agricultural tax reporting.

Examples of Using the 2010 Form 943 in Business

Consider a small farm employing seasonal workers. At the end of the year, the farm owner consolidates all payroll data, calculates taxes owed, and submits the Form 943 to report all activities related to employee payments and tax withholdings in compliance with federal regulations, preventing legal issues and maintaining good standing with the IRS.