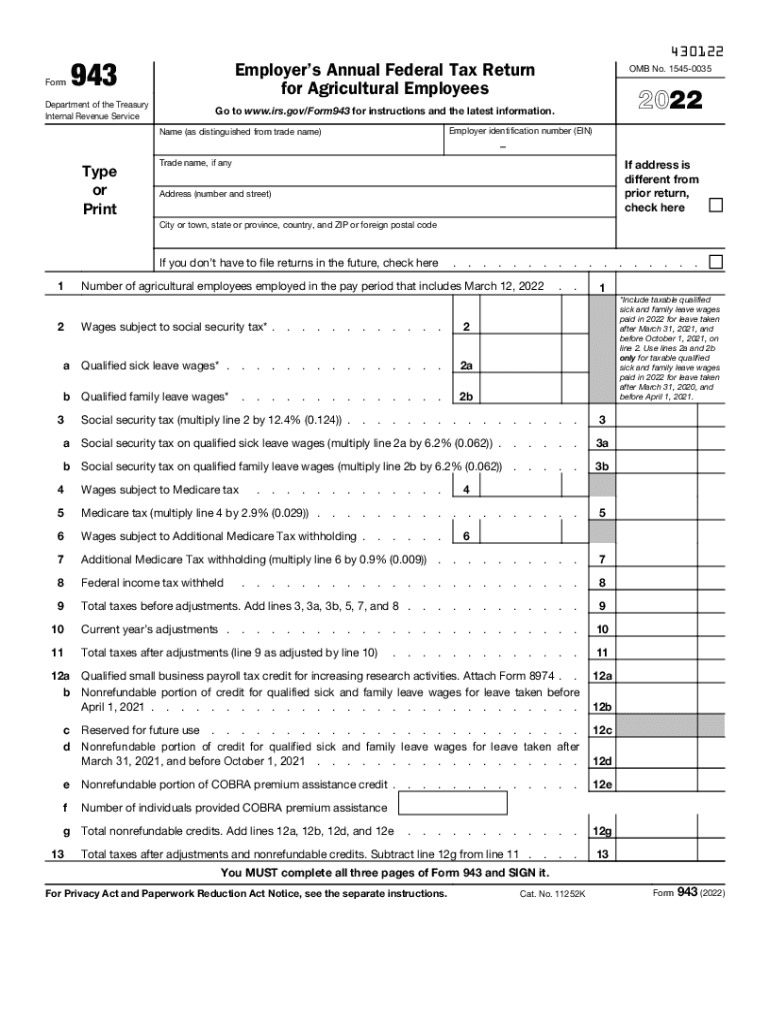

Overview of Form 943

Form 943, officially titled "Employer’s Annual Federal Tax Return for Agricultural Employees," is required for agricultural employers to report federal tax obligations. This form details wages paid to farmworkers subject to Social Security and Medicare taxes, as well as federal income tax withholdings. Employers must accurately fill out each section to ensure compliance with IRS requirements.

Using the 943 Form

To properly utilize Form 943, employers must first gather all payroll data for agricultural employees. This includes total wages paid, tips reported by employees, and any federal income tax withheld. Employers should carefully follow the IRS instructions accompanying the form to ensure each section is completed correctly. The form also allows employers to report sick and family leave wages and the associated tax credits.

Step-by-Step Completion Process

- Employer Information: Include your business name, address, and Employer Identification Number (EIN).

- Wage Reporting: Enter total wages paid to agricultural employees.

- Tax Calculations: Compute Social Security and Medicare contributions based on employee wages.

- Leave Wages: Report any sick or family leave wages and claimed tax credits.

- Payment Process: Calculate total tax liabilities and use Form 943-V for voucher payments.

Obtaining Form 943

Form 943 can be obtained directly from the IRS website as a downloadable PDF. Additionally, you can pick up a physical copy from a local IRS office or request one via mail by contacting the IRS. The form is also available through tax software providers, which may offer electronic filing options.

Who Uses Form 943?

Form 943 is primarily used by employers in the agricultural sector. This includes farms, ranches, and agricultural cooperatives that employ workers subject to federal employment taxes. Businesses that fall under NAICS codes related to farming activities should utilize this form to report and remit taxes.

Key Elements of Form 943

- Employer Identification Information: Essential for IRS records.

- Wage Details: Mandatory for accurate tax computation.

- Tax Liability Calculations: To identify amounts owed for Social Security, Medicare, and federal income taxes.

- Qualified Leave Wages: Reported separately for tax credits related to COVID-19 relief measures.

Important Dates and Filing Deadlines

Employers must submit Form 943 by January 31 following the end of the tax year. Employers making timely tax deposits may qualify for an extension until February 10. Ensuring prompt submission is critical to avoid potential penalties.

Penalties for Non-Compliance

Failing to file Form 943 or inaccurately reporting tax liabilities can result in IRS penalties. These can include fines calculated based on taxes owed and the duration of the delay in submitting the form. Therefore, precise and timely filing is crucial for compliance.

Form Submission Methods

You can either file Form 943 online or mail a physical copy to the IRS. Electronic filing through IRS-approved software provides a faster and more efficient option, while mailing requires ensuring that the form is postmarked by the deadline. Each submission method has specific instructions that must be meticulously followed to confirm receipt by the IRS.

IRS Guidelines and Changes

The IRS provides specific guidelines for filling out Form 943, including updates on tax law changes or applicable credits. These guidelines are critical in ensuring that employers report correct information, especially with pandemic-related tax adjustments. It is advisable to review these guidelines annually to stay updated on any modifications to the form or filing requirements.