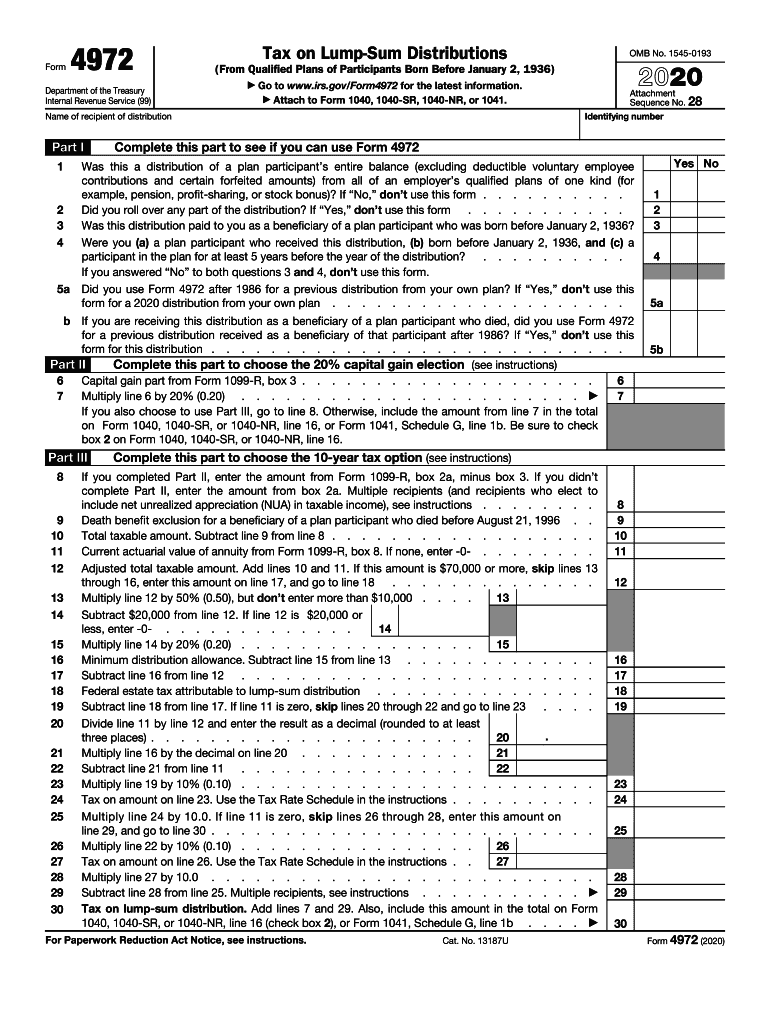

Definition and Purpose of Form 4972

Form 4972 is specifically designed for participants born before January 2, 1936, to calculate the tax on lump-sum distributions from qualified retirement plans. This form applies special tax options, like the 20% capital gain election and the 10-year tax option, which may provide a lower tax liability compared to reporting the entire distribution as ordinary income. Its primary purpose is to offer taxpayers a clearer taxation method of lump-sum withdrawals that reflect potential capital gains and structured payouts over time.

Eligibility Criteria for Using Form 4972

Eligibility to use Form 4972 is contingent on specific criteria. Taxpayers must have received a lump-sum distribution from a qualified retirement plan. The participant receiving the distribution must have been born before January 2, 1936. The distribution should not be a required minimum distribution, nor should it be attributable to an after-tax contribution, such as a Roth account. Understanding these eligibility requirements is crucial for taxpayers to ensure they properly apply the available tax benefits.

Special Tax Options

- 20% Capital Gain Election: Applicable to the portion of the distribution attributable to pre-1974 participation.

- 10-Year Tax Option: Allows the distribution to be taxed by averaging it over ten years as opposed to a single tax year.

Steps to Complete Form 4972

Filling out Form 4972 requires attention to several details to correctly process the tax reduction options. Here’s a general step-by-step guide:

- Identify Eligibility: Verify that the distribution qualifies under Form 4972's guidelines.

- Gather Required Information: Collect all necessary documentation about the retirement plan and distribution specifics.

- Calculate the Capital Gain: Use the 20% capital gain election where applicable, taking into account the date of plan participation.

- Determine the 10-Year Tax Option: Assess if the 10-year averaging method applies to the distribution.

- Complete Form Fields: Enter the calculated figures and personal information accurately in the corresponding boxes.

- Review and Submit: Ensure all entries are correct before submission; include with your tax return.

Required Documents for Form 4972

When preparing to complete Form 4972, collect the following documents to ensure accurate reporting:

- Plan Distribution Statement: Provides details of the lump-sum distribution.

- Previous Tax Returns: Useful for verifying historical participation details and ensuring consistent reporting.

- Documentation of Tax Withheld: Such as Form W-2 or Form 1099-R.

- Proof of Age for Eligibility Verification: A birth certificate or other official documentation showing the date of birth before January 2, 1936.

IRS Guidelines on Form 4972

The IRS provides several guidelines to facilitate the correct use of Form 4972. Taxpayers must adhere to specified calculations for both the capital gains election and the 10-year averaging. These guidelines help individuals precisely determine the taxable portion of their distribution. Official IRS instructions can offer additional clarity, detailing conditions under which certain tax options may or may not apply and elaborating on precise calculation procedures.

Examples of Using Form 4972 Effectively

Imagine a retiree named John, born in 1935, who received a $100,000 lump-sum distribution from his employer's pension plan. John uses Form 4972 to apply the 20% capital gain to $30,000 of his distribution due to his participation dating before 1974, while opting for the 10-year tax averaging on the remaining $70,000. This strategic application results in significantly reduced taxes owed compared to regular ordinary income reporting.

Who Typically Uses Form 4972

Form 4972 is typically employed by retirees over the age of 55 who are receiving lump-sum payments from qualified retirement plans. Generally, these are individuals nearing or past retirement age, and often those who have extensive work history allowing for a background in pension plan participation. It is also utilized by beneficiaries of such retirees in cases where the distribution occurs as part of a death benefit.

Penalties for Non-Compliance

There are significant penalties for failing to properly file Form 4972, or for inaccurately reporting the lump-sum distribution. Taxpayers might face an audit from the IRS, leading to back taxes, fines, and additional penalties based on the discrepancy between owed taxes and reported amounts. It is crucial to maintain accurate and comprehensive records to substantiate claims made on Form 4972 and prevent any potential legal or financial consequences.