Definition & Meaning

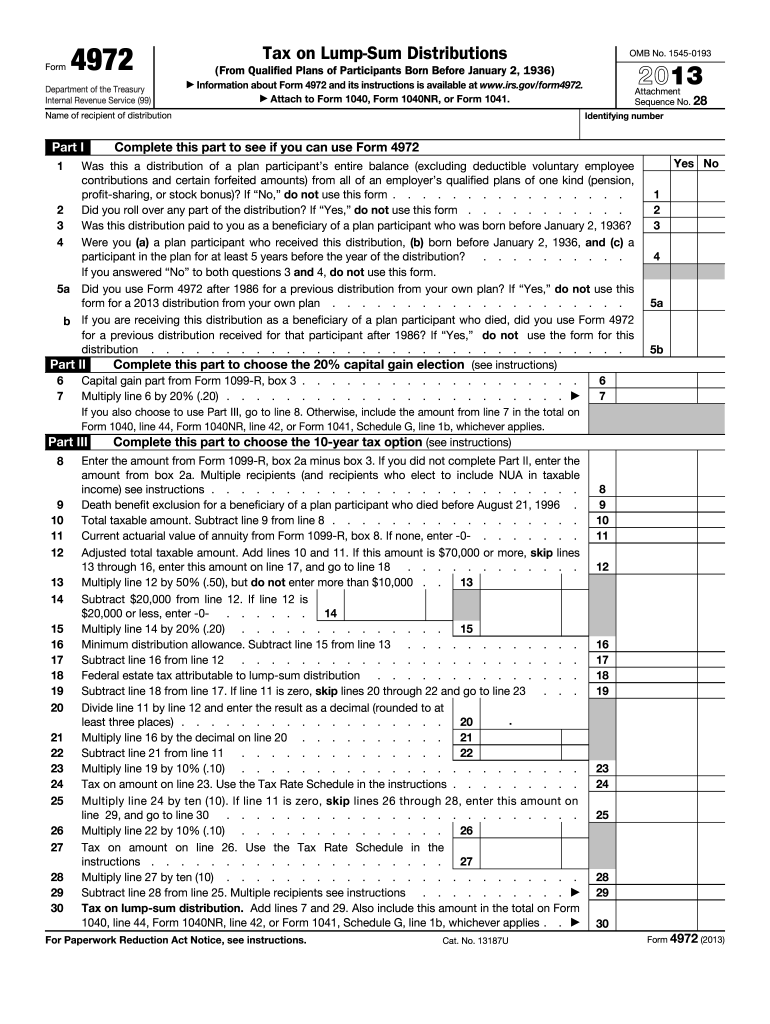

Form 4972 is a tax form used by individuals born before January 2, 1936, to calculate tax on lump-sum distributions from qualified retirement plans. This form provides eligible taxpayers with alternative tax treatment options such as the 20% capital gain election and the 10-year tax option. Completing this form accurately is critical to potentially lowering tax liabilities compared to reporting the distribution as ordinary income.

IRS Guidelines

According to IRS guidelines, Form 4972 allows qualifying taxpayers to split their lump-sum distribution into portions subject to different tax treatments. Detailed instructions focus on how to accurately report eligible portions of the distribution, compute the 20% capital gain portion, and utilize the 10-year averaging method.

Eligibility Criteria

Taxpayers must meet specific IRS eligibility criteria to use Form 4972, such as being born before January 2, 1936, and receiving a lump-sum distribution following the death, disability, or separation from service. Additionally, the form is applicable only once per taxpayer's lifetime for a particular retirement plan.

Steps to Complete the 2011 Form 4972

-

Gather Necessary Documents: Ensure you have all relevant 1099-R forms and details about the retirement plan distribution.

-

Complete Basic Information: Enter your name, social security number, and other identifying details as required.

-

Calculate Capital Gains: Determine the portion of the distribution eligible for capital gains tax by referencing instructions provided in the form's guidelines.

-

Compute Tax Using the 10-Year Option: Follow the instructions to calculate the tax using the 10-year averaging method for remaining distributions.

-

Fill Out Necessary Worksheets: Depending on the chosen tax options, complete any mandatory worksheets included in the form instructions.

-

Verify and Sign: Double-check all calculations and necessary information before signing the form to affirm its accuracy.

How to Obtain the 2011 Form 4972

Form 4972 can be obtained from the IRS website, local IRS office, or by requesting a mailed copy from the IRS directly. Additionally, many tax preparation software programs include Form 4972, and professional tax advisors can provide guidance on obtaining and completing the form.

Important Terms Related to 2011 Form 4972

- Lump-Sum Distribution: A one-time payment from a retirement plan, often triggering tax implications.

- 20% Capital Gain Election: A special tax treatment option allowing a portion of the distribution to be taxed as a long-term capital gain.

- 10-Year Averaging: A tax method that averages the lump-sum distribution over ten years, potentially lowering tax liability.

Examples of Using the 2011 Form 4972

Consider a retired individual who receives a lump-sum distribution from their former employer's pension plan. By leveraging Form 4972, they could apply the 20% capital gain election for part of the distribution benefiting from potentially lower tax rates. Another portion may qualify for the 10-year averaging method, spreading tax burden over a decade.

Penalties for Non-Compliance

Failing to properly complete and submit Form 4972 can result in penalties and interest from the IRS, including underpayment penalties if the taxable amount of a distribution was misreported. Ensuring accurate completion and timely filing is crucial to avoiding such consequences.

Form Submission Methods (Online / Mail / In-Person)

Form 4972 can be filed alongside your tax return electronically through IRS-approved e-file providers or on paper through traditional mail. It can also be included when using tax preparation services in person, providing flexibility depending on taxpayer preference.

Software Compatibility

Many tax preparation software suites, including TurboTax and QuickBooks, support the completion of Form 4972. These programs can guide users through the process, ensuring compliance with IRS regulations while helping calculate potential tax savings.

Required Documents

Taxpayers should have all necessary documents on hand, including Form 1099-R, which details the distribution amount and type from the retirement plan. Having previous tax returns on hand is also advisable to ensure consistency and accuracy with income history.