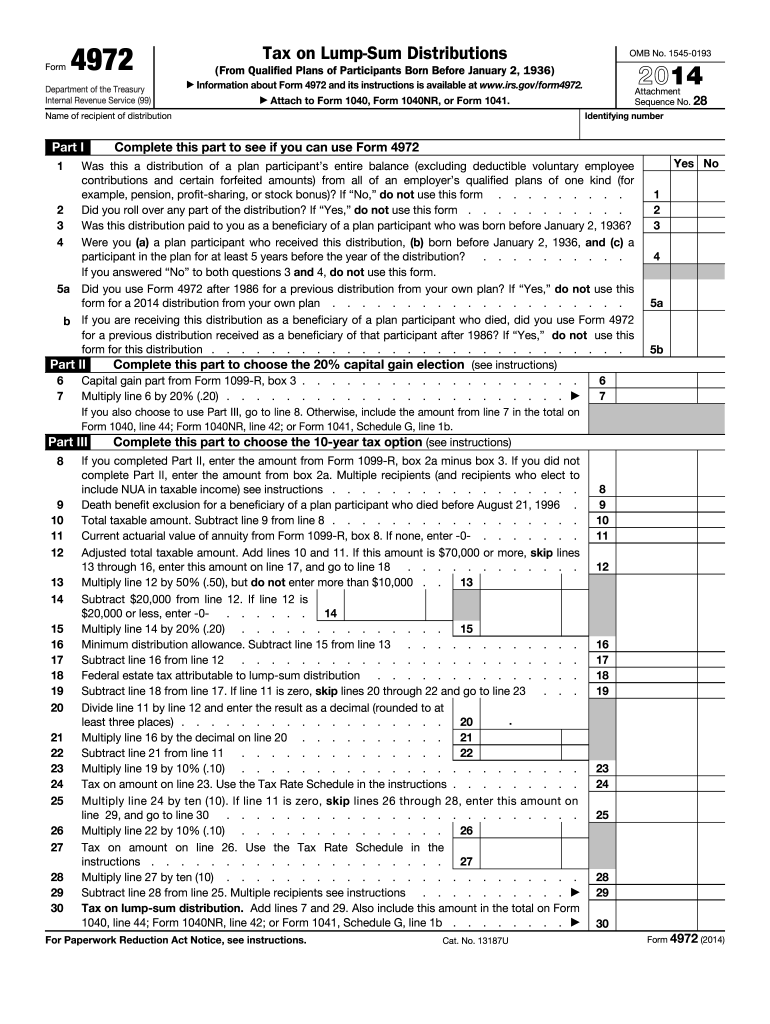

Definition & Function of Form 4972

Form 4972 is used to calculate the tax on lump-sum distributions from qualified retirement plans, specifically tailored for individuals born before January 2, 1936. The form helps taxpayers leverage special tax options, including the 20% capital gain election and the 10-year tax option. These options may provide a lower tax liability compared to treating the distribution as regular income. It’s essential for determining eligibility, calculating specific tax liabilities, and ensuring compliance with IRS requirements.

- Lump-sum distributions: Used mainly for retirees or beneficiaries taking full distribution from a retirement plan in one tax year.

- Special tax options: Offer potential tax savings by applying different tax computations.

- Eligibility criteria: Includes age-related and distribution timing factors.

How to Use the 2014 Form 4972

To utilize Form 4972 effectively, it’s crucial to understand the steps involved in completing the form:

- Gather necessary information: Collect details on your retirement plan distributions, including Form 1099-R provided by your plan administrator.

- Determine eligibility: Confirm that you qualify based on age and distribution type.

- Follow IRS instructions: Use the official IRS instructions to correctly apply the 20% capital gain election and the 10-year tax option.

- Complete calculations: Accurately fill out each section, ensuring calculations align with IRS tax laws and exemptions.

- Review and submit: Check for accuracy and submit the form with your tax return.

- Critical calculations: Ensure precise application of the election rules.

- Aging nuances: Only eligible for individuals or beneficiaries according to IRS age guidelines.

How to Obtain the 2014 Form 4972

Accessing Form 4972 involves straightforward methods to ensure compliance:

-

IRS website: The form is available for download directly from the IRS website.

-

Tax software: Programs like TurboTax or QuickBooks may integrate the form for easy filing.

-

Tax professionals: Certified tax preparers can provide the necessary form and guidance.

-

Electronic vs. printed forms: Choose based on preference, ensuring legibility and completeness.

-

Availability: Forms can be sourced year-round but are most relevant during tax season.

Step-by-Step Completion Guide

Completing Form 4972 involves several defined steps, crucial for ensuring accuracy and compliance:

- Eligibility confirmation: Verify the taxpayer meets age and distribution criteria.

- Calculation of tax: Use Parts II and III for calculating the 20% capital gain and 10-year option.

- Complete taxpayer details: Including personal information and plan specifics.

- Double-check entries: Validate totals, ensuring no discrepancies in figures.

- Copies for records: Retain copies of all documents and calculations for future reference.

- Verification processes: Avoid errors by double-checking entries against original documents.

Importance of the 2014 Form 4972

Understanding why Form 4972 is necessary highlights its significance for eligible taxpayers:

-

Tax savings potential: By applying special tax rules, taxpayers lower their liabilities, maximizing financial benefits.

-

Compliance necessity: Ensures adherence to IRS tax laws, avoiding potential penalties or audits.

-

Specialized scenarios: Primarily beneficial for those with singular, substantial retirement distributions.

-

Financial advantages: Opting for defined calculations can lead to notable savings.

-

IRS alignment: Compliance with federal tax rules prevents future legal issues.

Legal Compliance and Usage

Using Form 4972 within legal boundaries ensures lawful processing:

-

Compliance with the ESIGN Act: Known legal standards this form might fit into for executions, similar to electronic signature laws.

-

IRS guidelines adherence: Aligning with IRS policies for accurate tax reporting and submission.

-

Legally required documentation: Ensure all supplemental forms and evidence adhere to IRS conditions.

Key Elements of the 2014 Form 4972

Understanding the critical sections of Form 4972 guides accurate completion:

-

Personal identification details: The top section requires the filer’s personal information.

-

Distribution calculation sections: Specific parts handle special tax calculations.

-

Eligibility verification: Sections ensuring taxpayer qualification.

-

Information hierarchy: Presenting details in the order required by the IRS.

Required Documents

To properly complete Form 4972, you need:

-

Form 1099-R: From your plan administrator detailing distribution.

-

Proof of age: Documentation confirming eligibility age criteria.

-

Retirement plan documentation: Additional details proving source and nature of distributions.

-

Document organization: Maintaining a clear file of all forms and proofs aids in seamless filing.