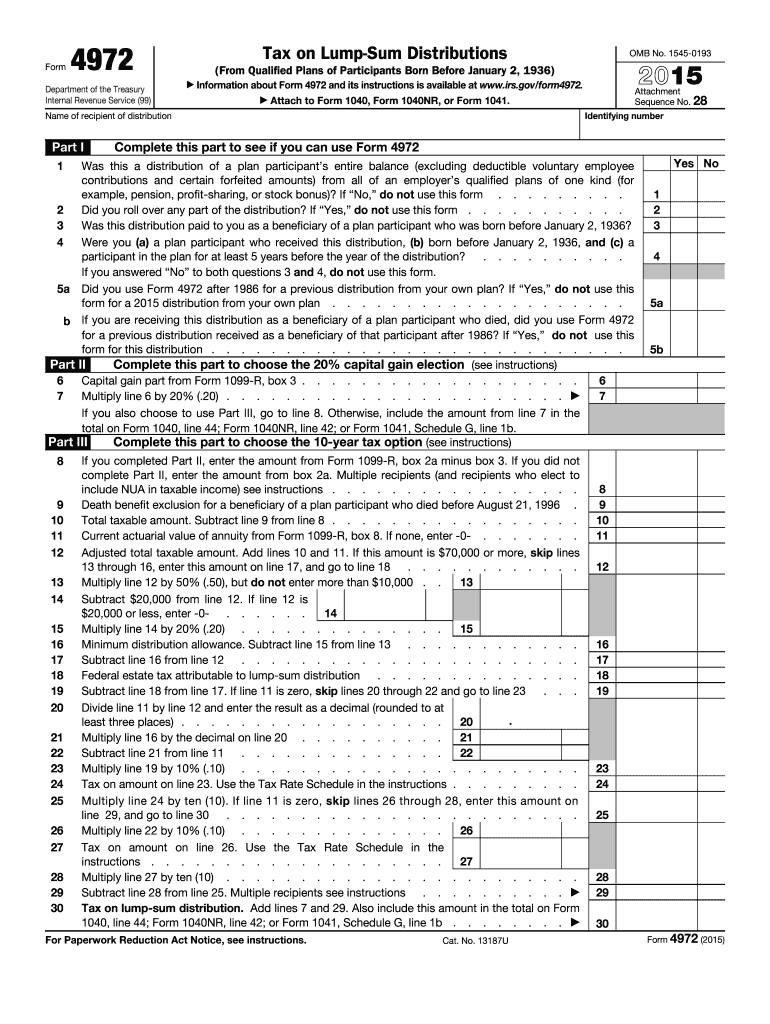

Understanding the 2015 Form 4972

Form 4972 is a significant document used to compute the tax on lump-sum distributions from qualified retirement plans. It is particularly relevant for individuals born before January 2, 1936. The form enables taxpayers to leverage specific tax options, potentially lowering their overall tax obligation compared to standard income reporting. Different sections of the form allow taxpayers to navigate eligibility, reporting, and calculation procedures. Understanding these elements is pivotal to correctly filing the 2015 version of Form 4972.

How to Use the 2015 Form 4972

Taxpayers can utilize Form 4972 to choose advantageous tax treatments for their lump-sum distributions. Available options, such as the 20% capital gain election and the 10-year tax option, can significantly affect the final tax liability. Taxpayers need to assess these options based on their financial circumstances to identify the most beneficial path. This form requires precise calculations to report the taxable amount, given the unique treatment these distributions may warrant.

Steps to Complete the 2015 Form 4972

- Assess Eligibility: Confirm that you meet the birth date and distribution criteria.

- Gather Required Documents: Collect your distribution statement and relevant tax records.

- Select Tax Options: Decide between the 20% capital gain election and the 10-year tax option.

- Calculate Taxable Amounts: Use the instructions to accurately compute your taxable distribution.

- Fill Out the Form: Carefully complete each part of the form, ensuring accuracy.

- Review and Submit: Double-check your entries for errors before submission.

Specific Examples

- 20% Capital Gain Option: Select this if a portion of the distribution qualifies as long-term capital gains.

- 10-Year Tax Option: Spread the tax burden over a decade for potential ease on the annual tax load.

Important Terms Related to 2015 Form 4972

Several terminologies are vital for understanding Form 4972. For instance, "lump-sum distribution" refers to a participant's complete withdrawal from a retirement plan upon leaving an employer or plan closure. Other terms like "ordinary income," "capital gains," and "special tax treatment" are crucial in navigating the form's instructions. Familiarity with these terms enhances comprehension and execution efficacy when filing.

Eligibility Criteria for Using the 2015 Form 4972

Eligibility to use Form 4972 involves specific criteria. You must be a plan participant or beneficiary born before January 2, 1936. The distribution should represent the entirety of the benefits payable under the plan. These requirements ensure that special tax treatments are appropriately applied to qualifying individuals. The IRS offers guidelines to aid taxpayers in determining their eligibility.

Key Elements of the 2015 Form 4972

Form 4972 features several critical components, including:

- Participant Information: Personal data confirmation to affirm eligibility.

- Distribution Details: Comprehensive insights into the total plan distribution.

- Tax Treatment Options: Sections to elect between alternative tax computations.

- Calculation and Totals: Final figures that integrate into broader tax filings.

Detailed Breakdown

- Taxpayer Identification: Essential for taxpayer validation.

- Lump-Sum Election Statement: Confirms the choice of special tax treatment, crucial for compliance.

IRS Guidelines on Form 4972

The IRS offers specific guidelines to optimize the correct use of Form 4972. These instructions provide clarity on eligibility, calculation methods, and submission timelines. Comprehensive reading of these guidelines is recommended to ensure accurate completion and adherence to IRS standards. The guidelines also cover potential penalties for non-compliance or incorrect filings.

Filing Deadlines for the 2015 Form 4972

Timeliness is critical when filing Form 4972. Adherence to specific deadlines must be preserved to avoid penalties. Generally, these timelines align with the regular tax filing period, typically April 15. However, extensions or special circumstances may affect this date. It is imperative to verify current year deadlines to avoid missteps in filing procedures.

Penalties for Non-Compliance

Failure to comply with filing requirements or misreporting figures can result in significant penalties. Given the complexity of lump-sum taxation options, precise adherence to regulations is essential to avoid fines or legal challenges. Understanding these consequences fosters a diligent approach to completing and submitting Form 4972 accurately.