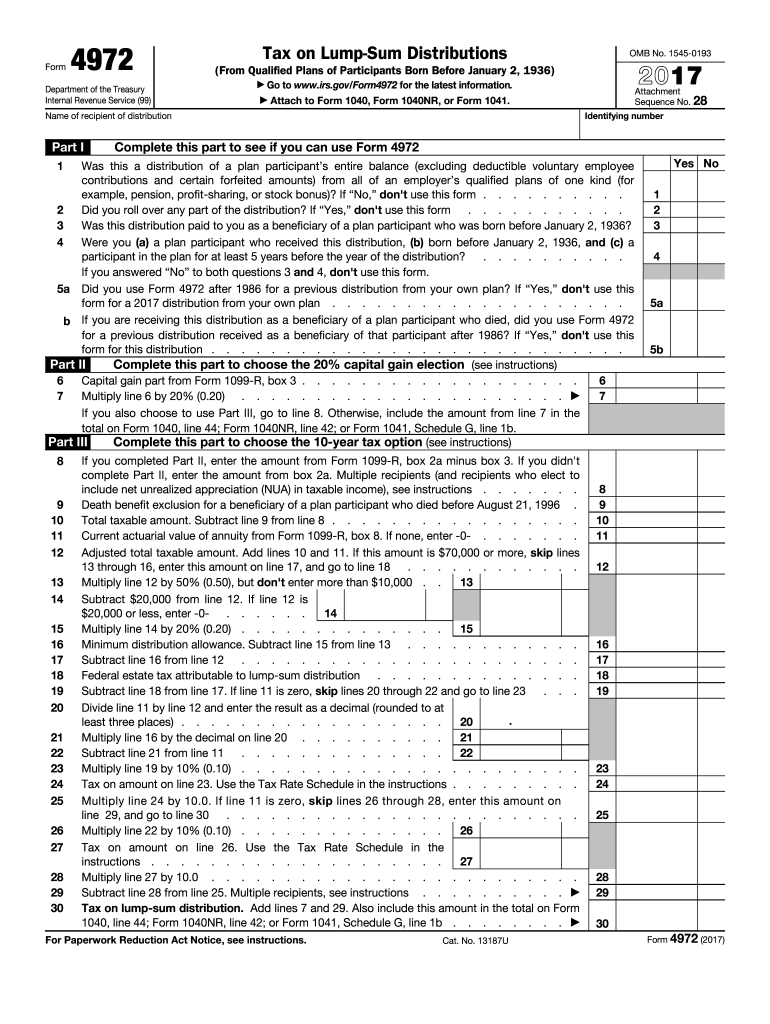

Definition & Purpose of Form 4972

Form 4972, for the year 2017, is designed to help taxpayers calculate the tax on lump-sum distributions from qualified plans. These distributions typically come from retirement or pension plans, and this form is essential for taxpayers born before January 2, 1936. By using Form 4972, eligible individuals can opt for special tax treatments like the 20% capital gain election and the 10-year tax option. Such choices often result in lower tax liabilities than reporting the distribution as ordinary income. This section provides clarity on who can use it and explains its importance alongside enhancing retirement financial planning.

How to Access Form 4972 for 2017

Accessing the correct version of Form 4972 is crucial, especially for accuracy in tax filing. For the 2017 version, it can be downloaded directly from the IRS website. Additionally, numerous tax preparation software includes this form, making it accessible to those using digital platforms. Physical copies are available through libraries, IRS offices, and should be obtained well in advance of the filing deadline to ensure ample time for completion. Both online and physical access points help ensure that taxpayers meet required deadlines without compliance issues.

Steps to Complete Form 4972

Completing Form 4972 requires careful attention to detail and an understanding of tax terms:

- Collect Necessary Documents: Before starting, gather all relevant documents, including lump-sum distribution statements and previous tax records.

- Eligibility Confirmation: Verify eligibility, ensuring the taxpayer was born before January 2, 1936.

- Calculate Tax Options:

- 20% Capital Gain Option: Determine if part of the distribution qualifies for this lower tax rate.

- 10-Year Tax Option: Compute the tax as if the distribution occurred over a 10-year period.

- Fill in Personal Details: Ensure accuracy in entering personal information like name, address, and Social Security number.

- Review and Submit: Double-check all entries for accuracy, then submit via the chosen method.

By taking these steps, taxpayers can ensure that Form 4972 is completed efficiently and correctly.

IRS Guidelines for Form 4972

The IRS provides specific guidelines for accurate completion and submission of Form 4972. These include understanding the eligibility criteria, complying with filing deadlines, and knowing the available tax options. The IRS also details how to report capital gains and outlines the potential benefits of the 10-year tax option. Understanding IRS guidelines helps taxpayers avoid mistakes that could lead to penalties or higher tax liabilities, making it a critical aspect of the process.

Filing Deadlines & Important Dates

Timely submission of Form 4972 is crucial. For the 2017 tax year, the form is typically due by April 15, 2018, unless extensions apply. Understanding this deadline ensures taxpayers avoid late filing penalties. Additionally, keeping track of any state-specific deadlines is essential, as some states may require additional documentation or have separate filing requirements. Timely filing is not just about avoiding penalties but ensuring the taxpayer takes full advantage of the tax options available.

Required Documents for Form 4972

Filing Form 4972 requires specific documentation to accompany the completed form:

- Lump-sum distribution statement (often from the plan administrator)

- Previous year’s tax return for reference

- Statements detailing any tax withheld from the distribution

These documents verify the distribution details and help calculate the correct tax treatment options. Comprehensive document gathering ensures that all financial elements are accounted for, supporting accurate form completion and submission.

Examples of Using Form 4972

Form 4972 can significantly lower tax obligations under the right circumstances. For example, a retired individual receiving a large distribution from their pension may opt for the capital gain treatment on a portion and apply the 10-year averaging on the remainder. This strategic choice can reduce their overall taxable income more effectively than declaring the entire sum as ordinary income. Real-world usage scenarios help illustrate the form’s benefits and guide similar strategies for different financial situations.

Penalties for Non-Compliance

Failing to file Form 4972 correctly or on time can result in notable penalties. Taxpayers may incur interest charges on unpaid taxes, and late fees can accrue if the form is not submitted by the deadline. Understanding these penalties highlights the importance of compliance and timely filing. Properly following IRS rules also ensures taxpayers avoid additional financial burdens beyond the primary tax obligations.

Eligibility Criteria for Using Form 4972

Eligibility to use Form 4972 primarily depends on the taxpayer’s birthdate and the type of distribution received. Taxpayers must have been born before January 2, 1936, to qualify for the specific tax options related to lump-sum distributions outlined in this form. The form is not suitable for everyone receiving such a distribution, emphasizing the need to verify eligibility before attempting to file. Correct eligibility checks protect against incorrect filings and ensure taxpayers utilize appropriate forms for their situations.

Form Submission Methods

Form 4972 can be submitted in multiple ways:

- Electronic Filing: Through IRS-approved tax software, facilitating quick and error-checked submissions.

- Mail: Sending physical forms and documents directly to the IRS.

- In-Person: At local IRS offices where assistance may be available.

Each method has its advantages and deadlines, and selecting the most convenient option helps taxpayers meet filing requirements efficiently, ensuring compliance and minimizing complications come tax season.