Definition and Meaning of Form 4972

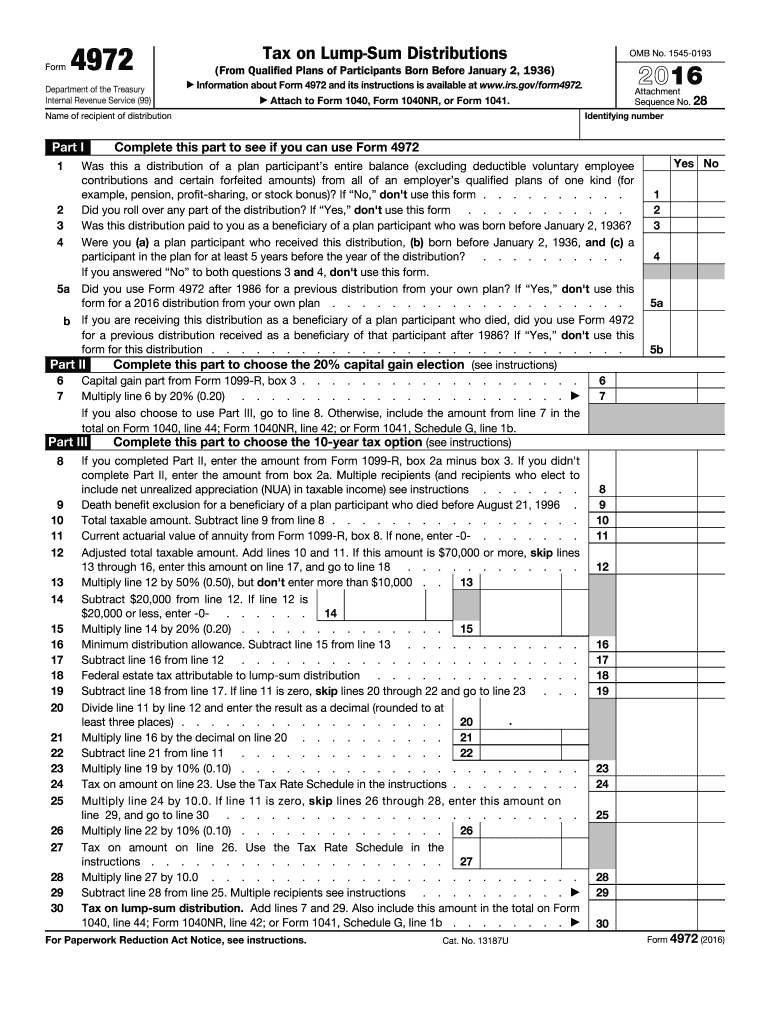

Form 4972 is an IRS form used to calculate the tax on lump-sum distributions from qualified retirement plans. This form is particularly relevant for individuals born before January 2, 1936, as it allows them to take advantage of special tax options. These options include the 20% capital gain election and the 10-year tax option, which can lead to a lower tax liability compared to reporting the distribution as ordinary income.

How to Use the 2016 IRS Form 4972

Using Form 4972 involves calculating your tax liability on lump-sum distributions. First, you need to determine your eligibility based on your date of birth and whether the distribution qualifies. Then, follow the instructions on Form 4972 to apply the 20% capital gain election or the 10-year tax option. Each section of the form guides you through calculations to assess which tax option is beneficial for your financial situation.

Eligibility Criteria

- You must be born before January 2, 1936.

- The distribution must come from a qualified retirement plan.

- The entire balance of the plan must have been distributed within one tax year.

Steps to Complete the 2016 IRS Form 4972

- Collect Necessary Information: Gather details about the lump-sum distribution including amounts and tax withholding.

- Determine Eligibility: Confirm your birthdate and the nature of the distribution.

- Fill Out the Form: Complete sections for capital gain and 10-year tax options. Use the IRS instructions to ensure accuracy.

- Calculate Tax Liability: Use the options on the form to determine the most tax-efficient method.

- Review and File: Double-check all entries for errors and file with your tax return.

Key Elements of the 2016 IRS Form 4972

- 20% Capital Gain Election: Applicable to pre-1974 participation costs, providing tax relief on long-held distributions.

- 10-Year Averaging: Spreads tax liability over ten years to potentially lower overall tax rates.

- Exclusions and Deductions: Specific sections deal with calculating the taxable portion and excluding any non-taxable amounts.

IRS Guidelines for Form 4972

The IRS provides detailed instructions for Form 4972, which are essential for understanding the specific calculations and requirements. Following these guidelines ensures compliance and accuracy, preventing incorrect filings and potential penalties.

Filing Deadlines and Important Dates

- Ensure that the form is filed with your annual tax return by April 15 of the year following the distribution.

Who Typically Uses the 2016 IRS Form 4972

This form is predominantly used by retirees or beneficiaries of retirement plans of individuals born before January 2, 1936. Financial advisors often guide such taxpayers through Form 4972 to help them optimize their tax positions using historical tax provisions.

Important Terms Related to 2016 IRS Form 4972

Understanding the terminology associated with Form 4972 is vital:

- Lump-Sum Distribution: A one-time payment for the entire balance from a retirement plan.

- Qualified Plan: Retirement plans that adhere to IRS legal guidelines like pensions or specific IRAs.

- Capital Gain Election: A method of taxing long-term gains at a reduced rate.

Penalties for Non-Compliance

Failing to file Form 4972 correctly or neglecting to include it when required can result in penalties. Incorrect reporting can lead to additional taxes and possibly interest on unpaid taxes. Thus, ensuring accuracy is critical.

Form Submission Methods

Form 4972 can be submitted either electronically with your tax return through accredited software like TurboTax, or mailed alongside paper tax filings. Electronic submissions often offer faster processing and fewer errors.

Examples of Using the 2016 IRS Form 4972

Consider a retiree who receives a lump-sum distribution from their pension plan. By reviewing Form 4972 options, they calculate potential tax savings from the capital gain election versus standard income taxation, leading to a strategic choice that reduces their immediate tax liability.

Completing this form requires careful calculation and understanding of tax implications for older taxpayers benefiting from past legislative considerations.