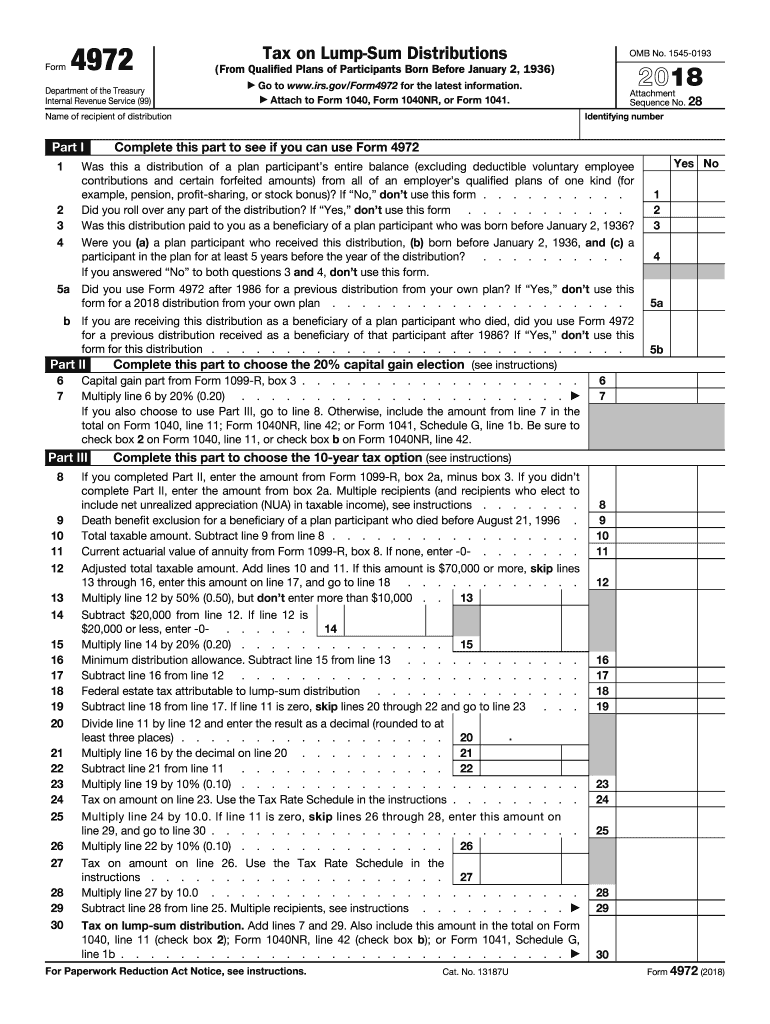

Definition and Purpose of Federal Tax Form 4972 for 2018

Federal Tax Form 4972, for the tax year 2018, serves a specific function in simplifying the tax calculation for certain retirees. The form is utilized to determine the tax on qualified lump-sum distributions from retirement plans for individuals born before January 2, 1936. It offers taxpayers the opportunity to opt for special tax calculations like the 20% capital gain election and the 10-year tax option. Understanding these options can often result in reduced tax liabilities, as it allows the distribution to potentially avoid being taxed as ordinary income.

How to Obtain the 2018 Federal Tax Form 4972

Taxpayers can acquire the 2018 version of Form 4972 through several methods. It is available for download from the IRS official website, which provides both the form and its instructions. Additionally, tax preparation software often includes digital versions of historical tax forms. Those preferring physical copies can visit a local IRS office or request a copy by mail by contacting the IRS directly.

Steps to Access the Form

- Visit the IRS website and navigate to the forms and publications section.

- Use the search feature to find "Form 4972" and select the 2018 version.

- Download the form along with the accompanying instructions as PDF files.

- Alternatively, open tax preparation software that includes a library of tax forms.

Steps to Complete the 2018 Federal Tax Form 4972

Completing Form 4972 involves several key steps, including the calculation of eligible lump-sum distributions and applying applicable tax treatments.

Step-by-Step Process

- Personal Information: Fill in your name, Social Security Number, and other relevant personal details at the top of the form.

- Lump-Sum Distribution: Use Part I to report the total amount of the distribution.

- 10-Year Tax Option: In Part II, complete lines pertaining to the 10-year tax option, which spreads income tax over ten years.

- Capital Gain Election: Part III involves calculating tax based on the capital gain option of 20% on eligible amounts.

- Death Benefits Exclusion: If applicable, Part IV addresses special treatments for death benefits.

- Final Calculation: Add the results from each section to determine the total tax liability on your lump-sum distribution.

Who Typically Uses the 2018 Federal Tax Form 4972

The form is primarily used by individuals over the age of 59 1/2, who have recently retired and are receiving a lump-sum distribution from a qualified retirement plan. This demographic includes former employees, union members, and military personnel who qualify under the criteria for special tax treatment. Eligibility often requires that the distribution comes from a pension, profit-sharing, or stock bonus plan.

Important Terms Related to the Form

- Lump-Sum Distribution: A one-time payment for a complete withdrawal of funds from a retirement plan.

- Capital Gain Election: A taxation option that allows part of the distribution to be taxed as a long-term capital gain.

- 10-Year Averaging: A method of spreading out tax liability over ten years, mitigating the impact of the distribution on a single year's tax return.

- Death Benefits: Specific provisions for distributions received by a beneficiary upon the account holder’s death.

Legal Use of the 2018 Federal Tax Form 4972

Using Form 4972 legally requires adhering to IRS rules regarding eligible distributions and taxpayer qualifications. Applying the form improperly can result in tax penalties and interest on underreported income. The user must provide accurate personal and financial information and apply the correct tax treatment as outlined in the IRS instructions.

Key Elements of the Form

Several sections make up Form 4972, each focusing on distinct elements of tax calculations:

- Part I: Details regarding the lump-sum distribution amount.

- Part II: The 10-year tax option calculation.

- Part III: Capital gain election specifics.

- Part IV: Calculations for qualifying death benefits.

Filing Deadlines and Important Dates

Although the form pertains to 2018 distributions, taxpayers often file it during the subsequent year's tax filing season, generally before mid-April. Understanding these timelines is crucial, as missing the April deadline could result in penalties. However, if an extension is filed, the deadlines may be adjusted accordingly.

Filing Timeline

- Regular Deadline: April 15th of the following tax year.

- Extended Deadline: October 15th if an official extension is properly filed.

IRS Guidelines for Form 4972

The IRS provides comprehensive instructions to aid taxpayers in accurately completing and filing Form 4972. This guidance is available alongside the form itself on the IRS website, offering detailed explanations of calculations, eligibility criteria, and submission requirements. Taxpayers are encouraged to carefully review these guidelines to ensure compliance.