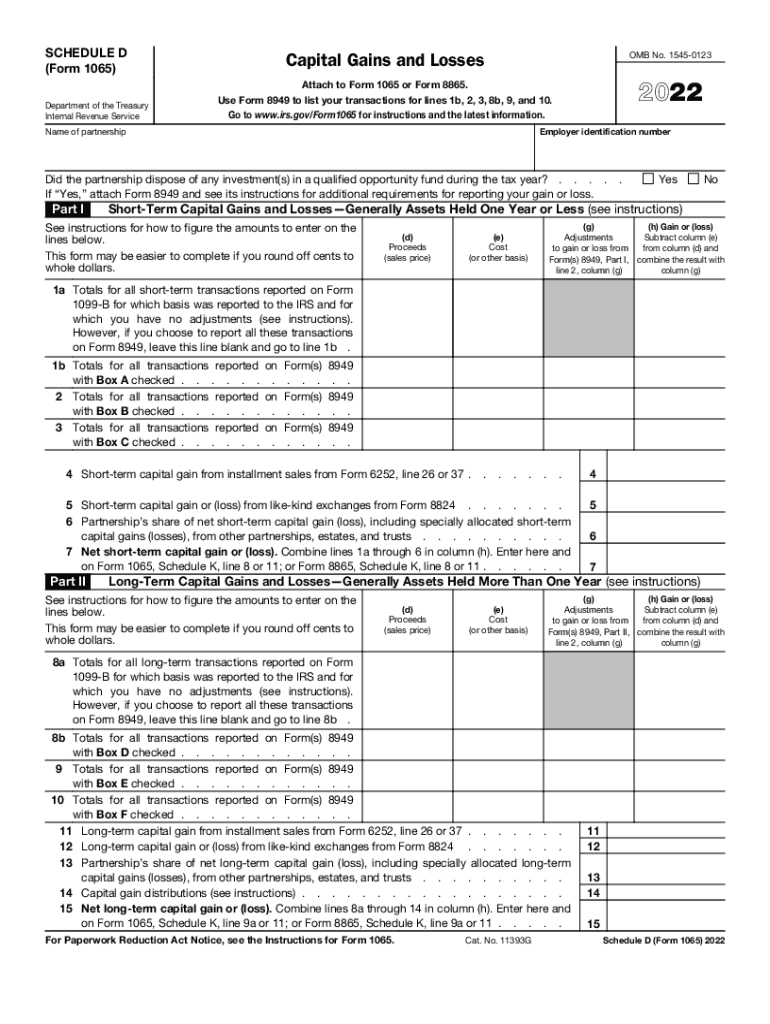

Definition and Purpose of Schedule D (Form 1065)

Schedule D (Form 1065) is a crucial tax document that partnerships in the United States use to report their capital gains and losses for a specific tax year. This form is designed to capture both short-term and long-term capital transactions, requiring detailed reporting of proceeds, costs, and specific adjustments related to assets held by the partnership. The form ensures that partnerships accurately disclose capital transaction outcomes, which in turn affects the overall tax liability of the entity.

Detailed Breakdown of Capital Gains and Losses

-

Short-term vs. Long-term Gains: Short-term capital gains are those realized from the sale of assets held for one year or less, whereas long-term gains apply to assets held for more than a year. The tax implications differ for each, with long-term gains typically enjoying lower tax rates.

-

Qualified Opportunity Funds: Partnerships must report any dispositions involving qualified opportunity funds, a mechanism providing tax incentives for investments in designated economically distressed regions.

-

Form 8949 Attachment Requirement: Complex or extensive capital transactions might necessitate the attachment of Form 8949 for comprehensive transaction reporting.

Steps to Complete Schedule D (Form 1065)

Completing Schedule D requires a systematic approach to ensure accurate and complete reporting. Below is a step-by-step guide to help partnerships navigate this process:

-

Collect Transaction Data: Gather details of all capital transactions, including the sale and purchase dates, proceeds, and cost basis.

-

Calculate Gains and Losses: Input all short-term and long-term capital gains and losses separately, ensuring each transaction is categorized appropriately.

-

Adjust for Depreciation: Apply any necessary adjustments for depreciation recapture, particularly relevant for asset sales involving depreciable property.

-

Total the Results: Sum the calculated gains and losses to ascertain the net gain or loss for the tax period.

-

Complete Form 8949 if Needed: For detailed transaction reporting, fill out Form 8949 with specifics, including adjustments.

-

File with Form 1065: Attach Schedule D to Form 1065, the primary partnership tax return form, when submitting to the IRS.

Key Elements of Schedule D (Form 1065)

Several critical elements within Schedule D (Form 1065) enable accurate reporting of capital gains and losses:

-

Transaction Specifics: Includes fields for transaction identification, dates of acquisition and sale, and proceeds.

-

Cost Basis Information: Provides lines for reporting the cost or purchase price of sold assets, adjusted for any improvements or changes.

-

Net Capital Gains/Losses Calculation: Designed to net all gains against losses from all transactions, reflecting the partnership's overall capital position.

Who Typically Uses Schedule D (Form 1065)

Partnerships of various forms and sizes across the United States utilize Schedule D (Form 1065) when they experience capital transactions:

-

General Partnerships: Report gains and losses realized from investments or asset sales specific to business operations.

-

Limited Partnerships (LPs): Often engage in diverse investment strategies, necessitating detailed tracking of capital gains and losses.

-

Limited Liability Partnerships (LLPs): Execute capital-intensive projects, requiring precise documentation of investment outcomes.

IRS Guidelines on Schedule D (Form 1065)

The IRS provides specific guidelines to ensure partnerships accurately complete and file Schedule D (Form 1065):

-

Record-Keeping Requirements: Partnerships must maintain detailed records of all capital transactions, including documentation supporting cost basis calculations.

-

Timely Filing: Aligns with Form 1065 deadlines, typically March 15, with potential extensions available.

-

Accuracy Verification: IRS mandates partnerships to cross-check calculations, especially concerning gains and losses, to prevent errors leading to audits or penalties.

Penalties for Non-Compliance with Schedule D (Form 1065) Requirements

Failure to file or inaccurately filing Schedule D may result in significant penalties:

-

Late Filing Fees: The IRS imposes penalties for late filing, calculated per partner per month, emphasizing timely compliance.

-

Underreporting Penalties: Incorrect or incomplete filing can lead to substantial fines based on the underreported tax amount.

-

Audit Risk: Non-compliance raises the likelihood of IRS audits, potentially subjecting partnerships to further scrutiny and financial rectification.

Examples of Using Schedule D (Form 1065)

Examples illustrate various scenarios where partnerships might engage Schedule D for accurate capital gain and loss reporting:

-

Real Estate Partnerships: Sell property investments within their portfolio, requiring delineation of gains for assets held under different timeframes.

-

Investment Partnerships: Engage in securities trading, necessitating precise tracking of transaction outcomes and tax impacts.

-

Venture Capital Firms: Exit or divest from startup investments, leading to capital gain or loss assessments reflected on Schedule D.

Filing Deadlines and Important Dates for Schedule D (Form 1065)

Understanding and adhering to key filing deadlines ensures compliance with IRS procedures:

-

March 15 Deadline: Schedule D must accompany Form 1065, which is due by March 15 for most partnerships.

-

Extension Options: Partnerships may file for an extension, usually extending the deadline to September 15, providing additional time for data collation and verification.

-

Estimated Payments Consideration: Partnerships owing taxes from realized gains should consider making estimated payments to avoid penalties for underpayment.

These comprehensive insights equip partnerships with the necessary knowledge to successfully manage the reporting of capital gains and losses via Schedule D (Form 1065).