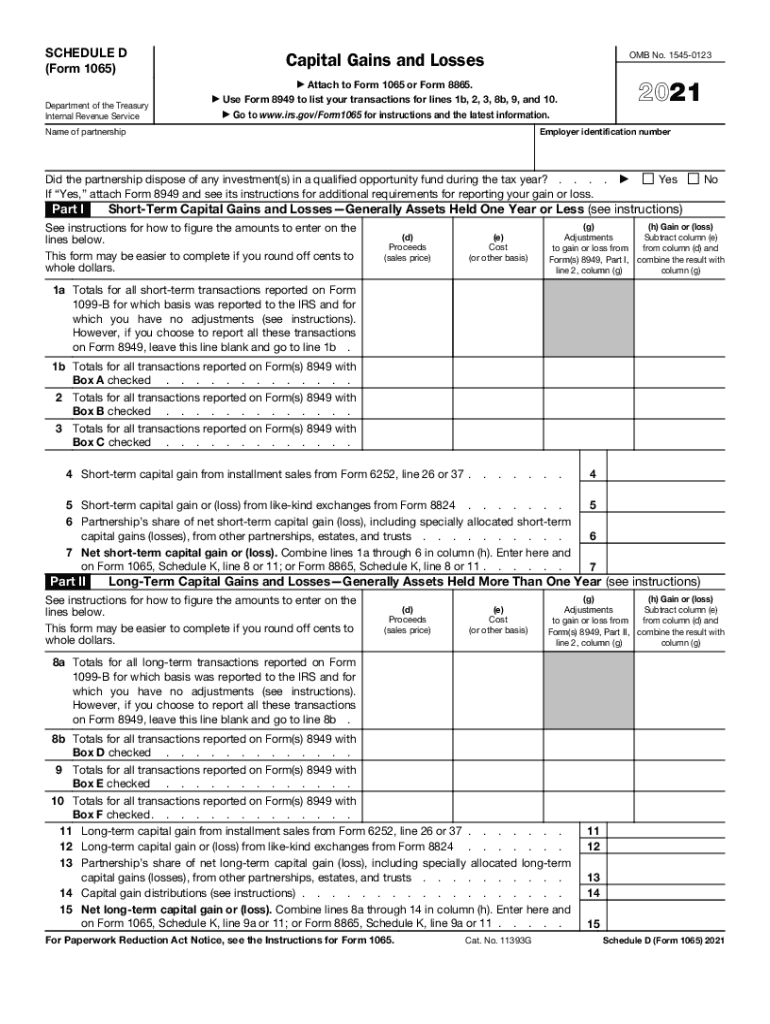

Definition and Meaning of IRS Schedule D

IRS Schedule D is a crucial component of the United States tax system, specifically used to report capital gains and losses from the sale or exchange of capital assets. This form is an integral part of federal tax filings, especially for individuals, partnerships, and corporations holding investments in stocks, bonds, real estate, and other assets. By detailing the gains and losses, taxpayers can accurately determine their tax liability for a given year, ensuring compliance with federal tax regulations. It is closely associated with Form 1040 or 1065, depending on the taxpayer's filing status. Utilizing Schedule D requires an understanding of various terminologies such as short-term versus long-term gains, cost basis, and adjustments.

Steps to Complete IRS Schedule D

Completing Schedule D involves multiple steps that require precision and attention to detail. Here's a general guide to help you through the process:

-

Gather Documentation: Collect all necessary documents including brokerage statements, purchase and sale records, and any related correspondence that confirms details of your transactions.

-

Classify Transactions: Identify if each transaction is short-term or long-term. This classification impacts how gains or losses are reported and taxed.

-

Calculate Gains or Losses: For each transaction, subtract the cost basis from the sales price to determine the gain or loss. Adjustments may be necessary for reinvested dividends or stock splits.

-

Fill Out Form 8949: List specific transactions on Form 8949 before transferring totals to Schedule D. Include details like proceeds, costs, and any adjustments.

-

Transfer Totals to Schedule D: Sum up the net gain or loss calculations and enter these amounts in the respective sections on Schedule D.

-

Attach to Main Tax Return: Connect Schedule D to Form 1040, 1041, or 1065, depending on your filing circumstances, and submit it along with your complete tax return by the filing deadline.

Important Terms Related to IRS Schedule D

Understanding certain key terms is vital when dealing with IRS Schedule D. Here are some essential ones:

-

Capital Asset: Any significant piece of property owned for investment or personal use, such as stocks, land, or cars.

-

Short-Term vs. Long-Term: Capital gains or losses categorized by the duration the asset was held. If held for less than one year, it is a short-term transaction; if over one year, it is classified as long-term.

-

Cost Basis: The original value of an asset, adjusted for changes such as stock splits or dividends.

-

Proceeds: The amount received from the sale of a capital asset.

-

Adjustment Codes: Codes listed on Form 8949 that explain modifications made to the cost basis or sales price of an asset.

Filing Deadlines and Important Dates

Meeting filing deadlines is critical to avoid penalties. Typically, Schedule D should be filed with your federal tax return, which is due April 15 of the tax year following the reporting period. In case of a weekend or holiday, the deadline shifts to the next business day. Extensions can be requested using Form 4868, but any taxes owed must still be paid by April 15 to avoid interest and penalties. It is advisable to keep abreast of IRS announcements for any changes to filing deadlines.

Who Typically Uses the IRS Schedule D

Schedule D is primarily used by individuals, partnerships, and corporations that have engaged in transactions involving capital assets. This includes retail investors dealing in the stock market, real estate transactions yielding capital gains or losses, and partnerships owning distributive share capital assets. Taxpayers reporting gains or losses from cryptocurrencies also utilize Schedule D. Those using passive investments, retirees managing investment portfolios, and small business owners with investment activities engage with this form.

IRS Guidelines for Using Schedule D

The IRS provides comprehensive guidelines to ensure correct completion of Schedule D, which involve:

- Consulting Publication 550 for investment income and expense information.

- Following specific instructions provided on Form 1040 or 8949 for listing transactions.

- Adhering to instructions specific to your filing status, whether it's a 1040, 1041, or 1065 filer.

- Checking the IRS website or seeking professional advice for the latest updates and clarifications concerning capital asset reporting rules.

Penalties for Non-Compliance

Failing to file Schedule D accurately or on time can incur significant penalties. The IRS may impose fines corresponding to the severity of the oversight, intentional omission, or misreporting. Penalty amounts vary, but they may include interest on unpaid taxes, accuracy-related penalties, or even fraud charges. To minimize risks, maintain meticulous records, ensure timely submissions, and consider consulting tax professionals for complex transactions.

Software Compatibility for Filing IRS Schedule D

Several tax preparation software solutions are compatible with IRS Schedule D, aiding in electronic filing and ensuring accurate computation of capital gains and losses. Commonly used software includes TurboTax, H&R Block, and TaxSlayer. These platforms offer step-by-step guidance for inputting transaction details, transferring data from Form 8949, and e-filing your return. For those using accounting software like QuickBooks, integration with tax software can further streamline the process, providing an efficient way to manage and report financial transactions related to capital gains.